")

Investment Thesis

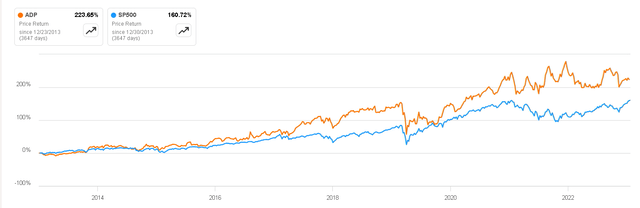

Automatic Data Processing (NASDAQ:ADP) has demonstrated outstanding performance in the stock market over the past decade, accompanied by a current trajectory of sustainable dividend growth. The company is characterized by resilience and solidity, attributes that contribute to its enduring success.

In this article, we will delve into the intricacies of ADP’s business model, highlighting key ratios that underscore its quality and stability. Additionally, I will conduct a valuation analysis to elucidate why, despite the company’s commendable characteristics, I believe it would be prudent to await somewhat lower prices before considering a buy.

Price Return in Last Decade (Seeking Alpha)

Business Overview

Automatic Data Processing is a provider of human resources management software and services. The company offers a range of solutions related to payroll processing, time and attendance management, benefits administration, and other HR-related functions.

Human resources management is essential for businesses, and I consider it to be just as important as cybersecurity and accounting. This is because ADP’s payroll solutions help clients ensure that their employees are paid correctly and on time, which is essential for employee satisfaction and compliance with ever-changing legal and tax regulations.

All of this leads formal companies to be willing to hire ADP services, as the cost becomes the least important factor when considering the benefits of reducing the risk of errors in payroll payments and preventing penalties and legal issues. In fact, there are economic plans that start at $29 per month, plus $5 for each new employee who wishes to be added. This is why the company has recurring income and a significant capacity to rise at the rate of inflation or more without losing customers.

ADP Investor Presentation

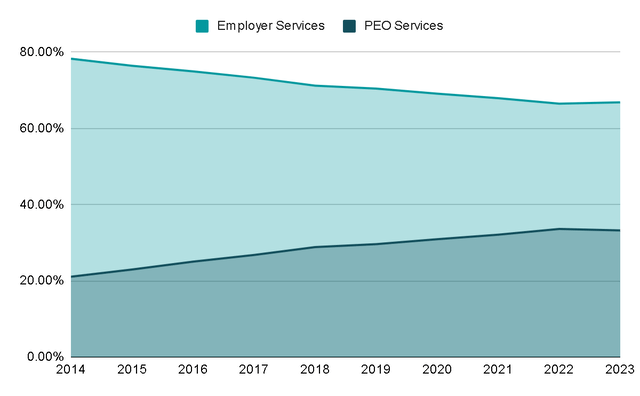

Currently, 67% of revenue comes from the ‘Employer Services (ES)’ segment, which has grown at a rate of 4% annually over the last decade and maintains EBITDA margins of 37%. This segment offers software with a range of services, including payroll management, employee benefits administration, workforce management, retirement services, and compliance services.

On the other hand, the ‘PEO (Professional Employer Organization) Services‘ segment represents 33% of revenue and has experienced an annual growth rate of 11% over the last ten years, with current EBITDA margins of 16.5%. In this segment, the company is responsible for outsourcing human resources, providing services such as benefits packages, protection and compliance, talent hiring, and outsourcing of recruitment processes, among others. This is significant for ADP clients as it allows them to reduce costs associated with hiring and maintaining an in-house HR team while delegating activities to professionals with expertise and tools, enabling them to focus on their core competencies.

PEOs often provide essential services that can be valuable to businesses regardless of economic conditions, so during challenging economic times, businesses may turn to PEOs as a cost-effective solution to manage HR functions more efficiently.

Author’s Representation

In fact, during the great recession of 2008 the company remained flat in terms of revenue growth and the EBITDA margin did not fall. This shows us how resilient this business is and its extraordinary quality.

Author’s Representation

Key Ratios

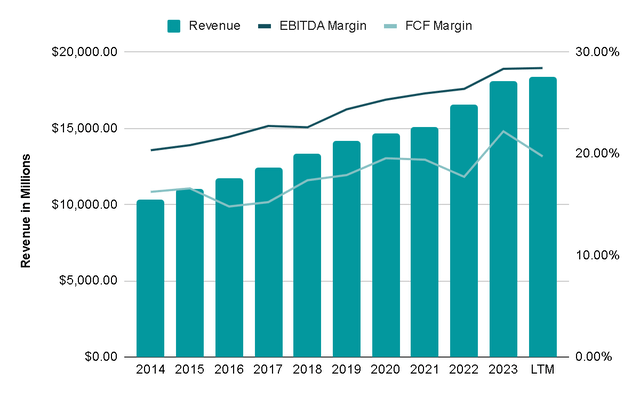

Considering the two segments, revenue has experienced a consistent annual growth of 6% over the last decade. During this period, EBITDA margins have increased from 20% to the current 28%. A similar trend is observed in the Free Cash Flow margin, which has risen from 16% to nearly 20%. These developments indicate that the company has leveraged economies of scale effectively, spreading its fixed costs over a larger client base. Additionally, rigorous cost control and effective expense management have played a crucial role in these positive financial outcomes

Author’s Representation

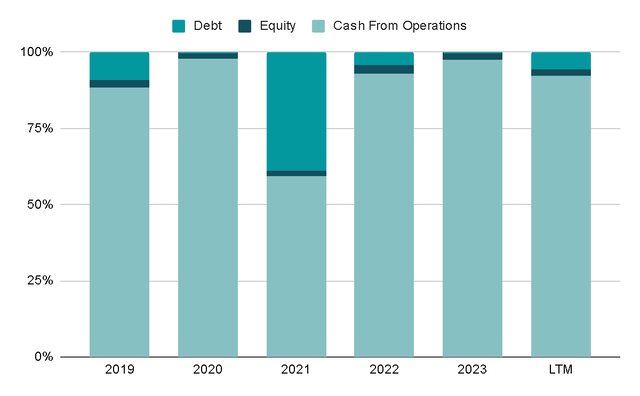

Furthermore, it’s noteworthy that over the last five years, the company has been funded by an impressive 85% of the cash from operations it generated. This aligns with ADP’s reputation as a robust cash generator. The absence of debt is particularly significant, as it ensures that the capital can be directed toward shareholder-friendly initiatives such as share buybacks and dividends. Without the burden of debt risk, these profits can be utilized more effectively.

Author’s Representation

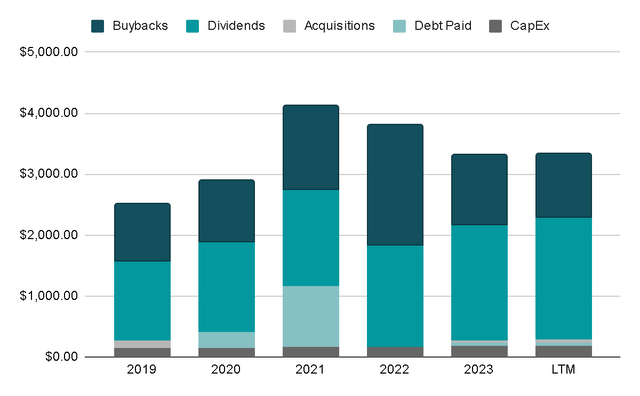

To be specific, 30% of the capital has been reinvested in the business, a strategic move given the excellent returns we will explore later. Another substantial portion, 64%, equivalent to more than $14 billion, has been allocated to buybacks and dividends.

Author’s Representation

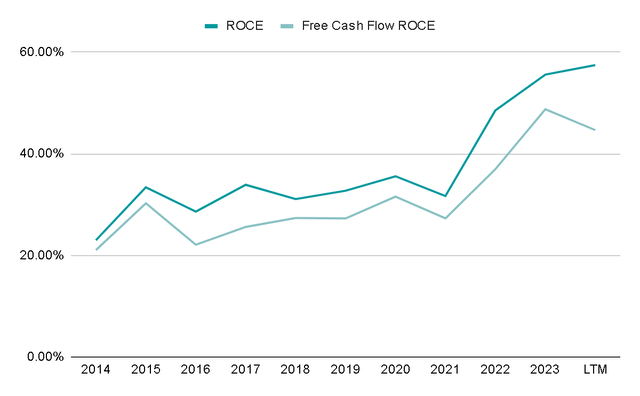

The accompanying image reveals the extraordinary return on capital employed by the company, currently standing at 57%, with Free Cash Flow return on capital employed at 45%. These figures underscore the highly profitable nature of the business, indicating its ability to generate long-term value.

Author’s Representation

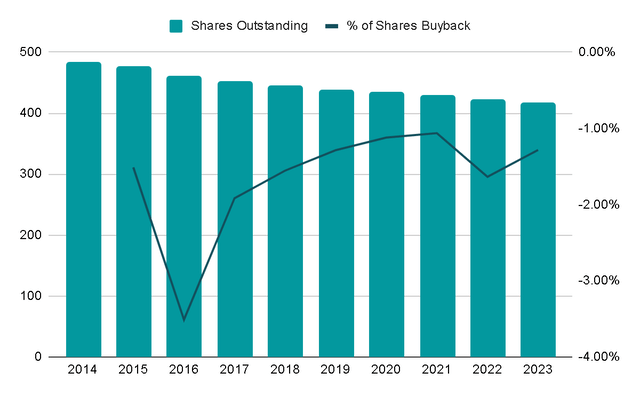

Turning to buybacks, the company has consistently repurchased its shares over the last decade, averaging a rate of 1.5% per year, with no sign of slowing down.

Author’s Representation

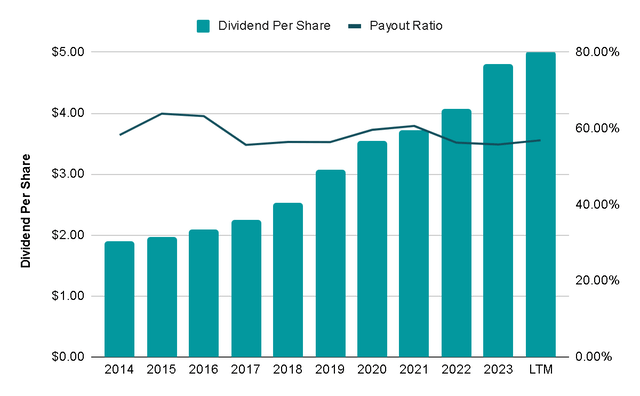

On the dividend front, the per-share distribution has seen an annual increase of 10% over the past decade, currently boasting a dividend yield of 2%. The dividend appears robust and sustainable, representing 57% of the Free Cash Flow in the last twelve months. On average, it has distributed 54% of Free Cash Flow, leaving room for potential increases. This underscores the importance of maintaining a debt-free stance.

Author’s Representation

Valuation

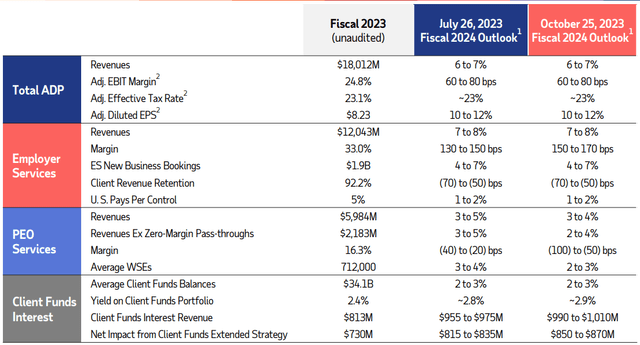

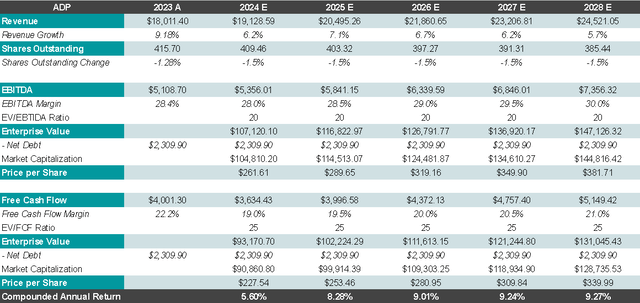

To estimate the potential return on the stock at its current price, I’ll project the performance of the two segments of the company. For FY2024, I’ll consider the most recent guidance provided during Q1 2024, indicating growth between 7 and 8% for the Employer Services segment and between 3 and 4% for the PEO Services segment.

Q1 2024 Presentation

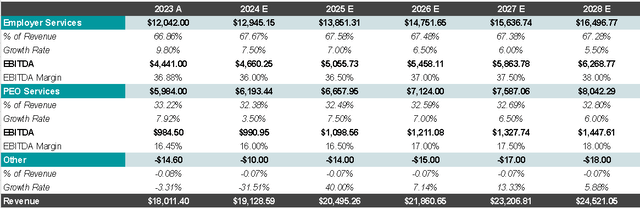

In the following years, I anticipate an annual growth rate of 6.5% for the Employer Services segment and 6% for the PEO Services segment. Additionally, I find it plausible that EBITDA margins will continue to expand.

Author’s Representation

This projection results in a total annual revenue growth of 6.4%, slightly below the management’s expectation of an increase between 7 and 8%, as outlined on page 13 of the Investor Presentation. If we factor in the mentioned margin expansion and apply multiples of 20x EBITDA and 25x Free Cash Flow, we could anticipate a return of 9% per year, along with the dividend yield of 2%. Considering the high multiples assumed in the valuation, it appears there might not be much margin of safety.

Author’s Representation

Risks

While the business model boasts excellent characteristics that contribute to its quality, it’s essential to acknowledge certain risks, even if they aren’t imminent or insurmountable. One key concern is competition, as the HR software and services industry is highly competitive, with numerous companies trying to expand their market share. Intense competition could exert pressure on prices, diminish profit margins, and necessitate continuous innovation to maintain a competitive edge. Notable competitors in this landscape include Paychex, Workday, Oracle, and SAP, underscoring the significance of this competitive challenge.

Linked to this is the exposure to rapid technological advancements, which could potentially impact ADP’s business model. Failing to adapt to emerging technologies or facing disruptions in technology infrastructure could jeopardize competitiveness and service delivery. This becomes especially pertinent considering that any technological delays would put ADP at risk of trailing behind competitors consistently investing in software improvements.

In this context, ADP’s ability to foster strong, enduring relationships with clients and leverage the replacement costs of its products becomes crucial. For clients, maintaining existing software often proves a preferable option compared to undergoing the substantial task of training an entire staff on new software. The learning curve and the potential for new software to introduce unforeseen errors further enhance the appeal of sticking with familiar technology.

Final Thoughts

There is no doubt that the company possesses qualities that render it highly resilient across various macroeconomic environments, and its businesses benefit from enduring tailwinds that suggest continued growth for years to come. Moreover, the company’s capital allocation and financial position present a compelling case for any investor. Currently, in a phase of moderate/low growth, the company is prioritizing capital allocation to reward shareholders.

Despite these positive aspects, the current valuation does not strike me as entirely attractive. While I don’t anticipate a company of this quality to deliver projected returns exceeding 15% annually (unless there were strong temporary problems or a reduction in the guidance provided, for example), I would find the valuation more appealing around $200 USD. This would translate to a P/FCF of 20x, resulting in an expected return of approximately 12 or 13%. Given these considerations, I believe a ‘hold‘ rating is the most prudent stance at the moment.

EV/EBITDA Ratio (Seeking Alpha)

Read the full article here