")

Investment Outlook

AvePoint, Inc. (NASDAQ:AVPT) provides clients with cloud-based data management software and related services.

Investors have been rewarded in the past year as the firm has reached operating breakeven on reasonably strong growth and the potential of AI in its products.

However, the stock has plateaued recently, and AI functions are still in the proof-of-concept stage, while top line revenue growth is expected to slow in 2024.

Until management can increase growth while improving operating results, I’m Neutral [Hold] on AVPT.

AvePoint’s Market And Approach

According to a 2023 market research report by Grand View Research, the cloud data management market size was an estimated $89 billion in 2022 and is forecasted to reach $222 billion by 2030.

If achieved, this would represent an impressive compound annual growth rate of 12.1% from 2023 to 2030.

The market is expected to see increased demand from clients seeking improved risk management, parallel processing architectures, automation and increased security amid a proliferation of numerous cyber threat vectors.

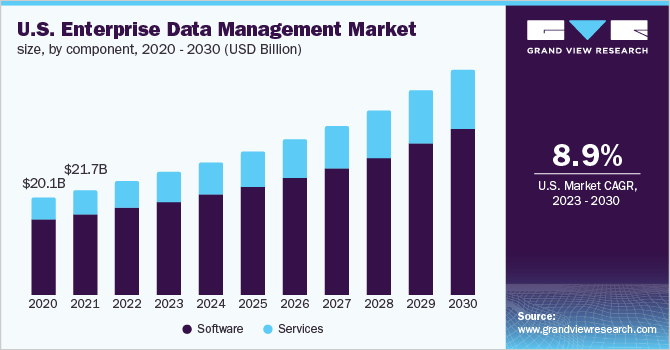

The chart below shows the historical and projected future growth trajectory of the U.S. Enterprise Data Management Market from 2020 to 2030:

Grand View Research

Major competitors in the space include these companies:

-

IBM

-

Oracle

-

SAP SE

-

Cloudera

-

Amazon Web Services

-

Teradata

-

MindTree

-

Broadcom (Symantec)

-

Informatica

-

Micro Focus

AvePoint sells both through its direct sales force and through channel partners. It pursues companies of all sizes in all major industry verticals and focuses on its channel partners for smaller and mid-market prospects while aiming at enterprises with its in-house sales and marketing teams.

AVPT’s software solutions are primarily headcount-based, and the sales team likely pursues a ‘land and expand’ strategy within its larger mid-market and enterprise accounts.

Recent Financial Trends And Valuation

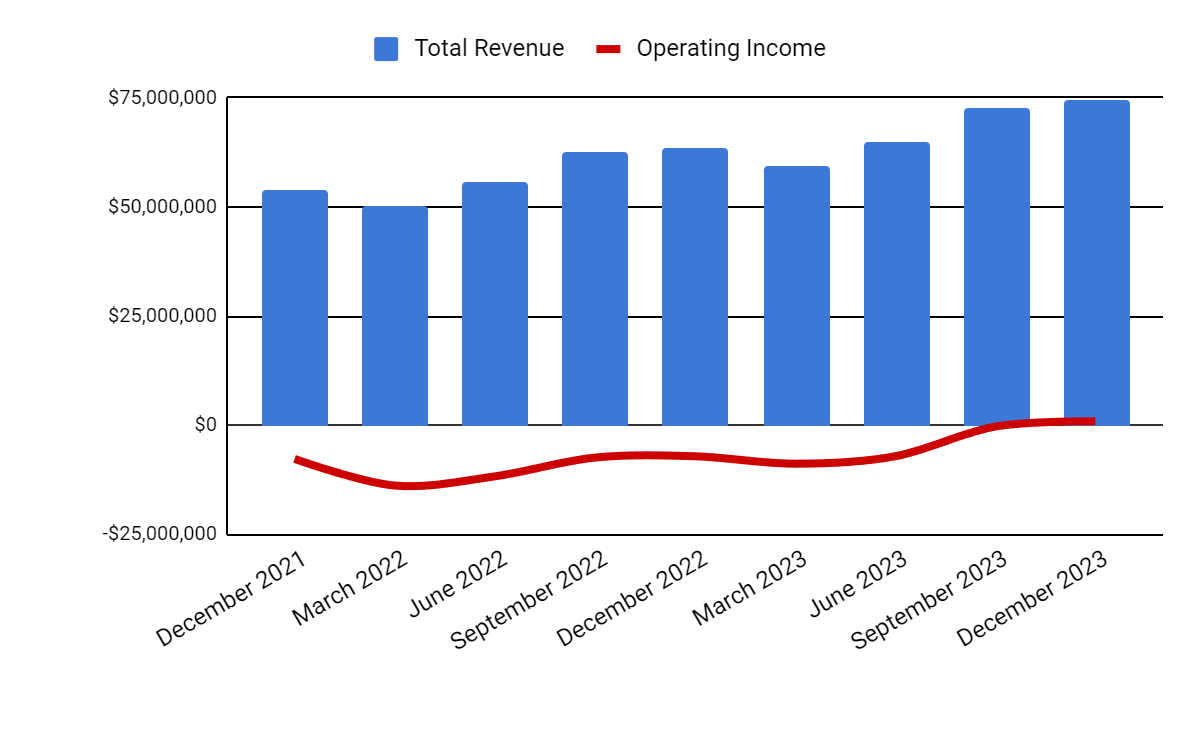

Total revenue by quarter (columns) has risen in recent quarters, while operating income by quarter (line) has turned positive due to gross profit and reduced SG&A costs.

Seeking Alpha

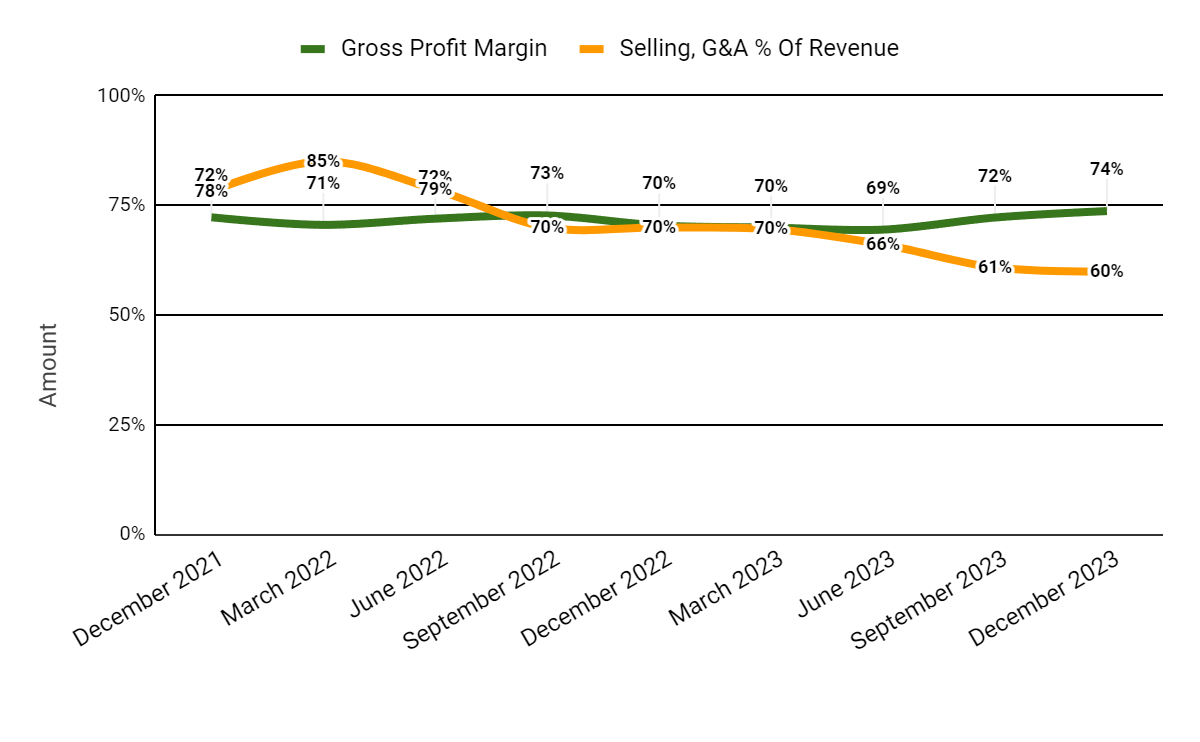

Gross profit margin by quarter (green line) has risen as a result of improved scaling efficiencies; Selling and G&A expenses as a percentage of total revenue by quarter (orange line) have dropped significantly due to management’s efforts to reduce costs.

Seeking Alpha

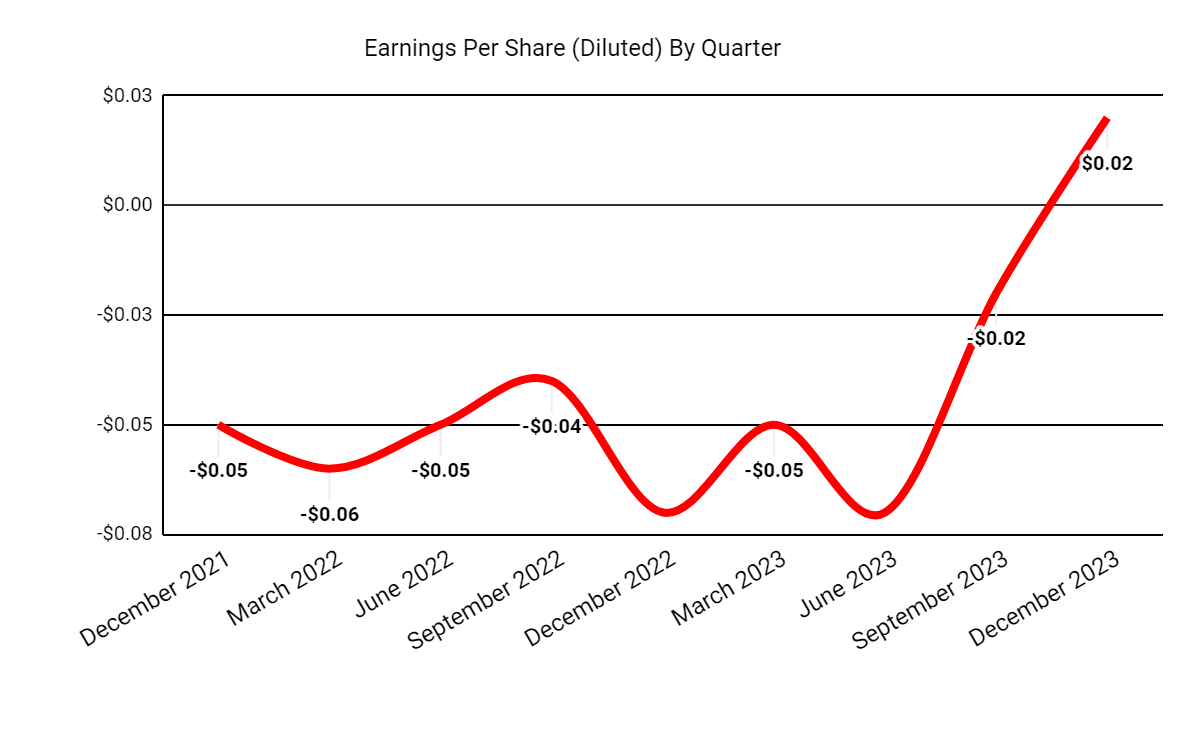

Earnings per share (Diluted) have risen materially into positive territory due to reduced costs and continued topline revenue growth:

Seeking Alpha

(All data in the above charts is GAAP).

Compared to partial competitor Informatica Inc. (INFA), the table below shows how AvePoint stacks up:

|

Metric |

Informatica |

AvePoint |

Variance |

|

EV/Sales (“FWD”) |

7.3 |

4.0 |

-44.5% |

|

EV/EBITDA (“FWD”) |

21.8 |

39.4 |

80.5% |

|

Rev. Growth Estimate (“FWD”) |

6.5% |

16.8% |

158.2% |

|

Net Income Margin |

-7.9% |

-8.0% |

-1.8% |

|

Operating Cash Flow |

$266,350,000 |

$34,690,000 |

-87.0% |

(Source: Seeking Alpha Data)

The comparison indicates that AvePoint is expected to grow faster, but the market is valuing Informatica at a higher forward EV/Sales multiple but a lower EV/EBITDA multiple.

I’ve created a major metrics table as a handy reference for the company’s recent results:

|

Metric |

Amount |

|

EV/Sales (“FWD”) |

4.0 |

|

EV/EBITDA (“FWD”) |

39.4 |

|

Price/Sales (“TTM”) |

5.4 |

|

Revenue Growth (“YoY”) |

17.0% |

|

Net Income Margin |

-8.0% |

|

EBITDA Margin |

-3.9% |

|

Market Capitalization |

$1,470,000,000 |

|

Enterprise Value |

$1,270,000,000 |

|

Operating Cash Flow |

$34,690,000 |

|

Earnings Per Share (Fully Diluted) |

-$0.12 |

|

2024 FWD EPS Estimate |

$0.11 |

|

Rev. Growth Estimate (“FWD”) |

16.8% |

|

Free Cash Flow/Share (“TTM”) |

$0.17 |

|

Seeking Alpha Quant Score |

Hold – 3.11 |

(Source: Seeking Alpha Data)

The firm’s Rule of 40 performance results for the most recent quarter produced only an 18.2% score, indicating AVPT needs significant improvement in this regard, as the table shows here:

|

Rule of 40 Performance (Unadjusted) |

Q4 2023 |

|

Revenue Growth % |

17.0% |

|

Operating Margin |

1.2% |

|

Total |

18.2% |

(Source: Seeking Alpha Data)

Why I’m Neutral On AvePoint

More than half of AVPT’s revenue comes from outside of North America, with significant growth in the regions of EMEA and APAC.

To continue its growth potential, management is working hard to integrate AI capabilities to enhance data management and governance functions.

However, the process is still in the early stages of experimentation, so it will likely be some time before the company sees material positive impacts.

Management sees a certain resilience in the firm’s small and medium business [SMB] segment, as it has used relationships with managed service provider partners to broaden its offerings.

Leadership has also made progress with cost reductions and increasing operating leverage, in recent quarters.

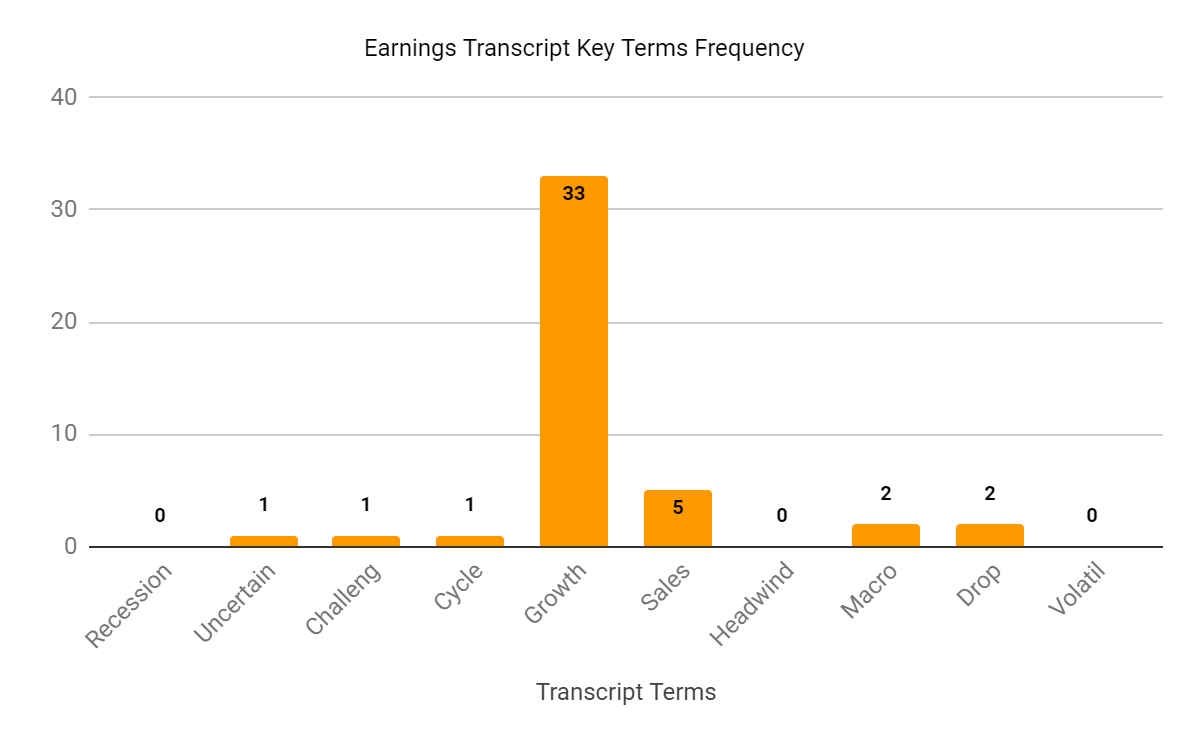

I’ve prepared a sentiment indicator from the company’s most recent earnings call, as shown here:

Seeking Alpha

The chart shows that AVPT continues to see macroeconomic uncertainties resulting in cautious client spending.

But, the company is seeing a strong increase in customer interest in proof of concept stage activity with integrating AI product features in the context of its Microsoft offerings.

Forward revenue growth estimates expect 2024 growth to be 15.6% over 2023, which, if achieved, would represent a slight drop versus 2023’s growth rate of 17.05% over 2022.

AvePoint still hasn’t reached the $100 million quarterly revenue mark, and its growth rate is slowing.

While it’s encouraging that the company has reached operating breakeven, like so many technology companies seeking to improve their bottom line in a higher cost-of-capital environment, it is likely coming at the cost of slower revenue growth.

As the firm has improved its operating results, the market has rewarded its stock with a highly favorable gain of 95.5% over the past year.

However, that gain appears to be leveling off recently, so the easy money may have already been made on AVPT.

Until management can boost growth while improving operating results, I’m Neutral on AvePoint, Inc. and believe the stock may struggle for meaningful upside in the near term.

Read the full article here