")

Year-to-date, the STOXX Europe 600 Insurance is up by 8.5% and has delivered a total return, including dividend payment, of almost 12.1%. Looking back, in 2022, we reported how AXA SA was our Favorite Insurer (OTCQX: AXAHY, OTCQX: AXAHF), and YTD, the company confirmed its best-in-class return story, delivering a total performance of 13.75%. Here at the Lab, we believe there will likely be more upbeat within the sector into 2024. Despite a positive stock price performance, European insurers were impacted by a declining premium due to higher risk-free yields; in addition, within the sector, IRS17 regulatory requirements had a mixed impact on earnings, and if we add credit risk concerns, the picture was not ideal. However, looking ahead, we remain positive on European insurance and, more importantly, with AXA investment. At the single entity level, this is based on four key themes:

- Balance sheet and scale: With inflation and higher interest rates for longer, insurance barriers to entry are more elevated. Competition will be lower, with smaller and new players having difficulties entering a market that requires significant investment in regulations and more needed technology investments. AXA’s past investment to enhance efficiency with automation in claims and a capillary distribution are key value drivers that cannot go unnoticed. In addition, GEO and earnings diversification pays off within the industry. We also believe that the company has M&A upside optionality supported by an anticipated acceleration of market consolidation. We believe AXA is best positioned to take advantage of this current environment;

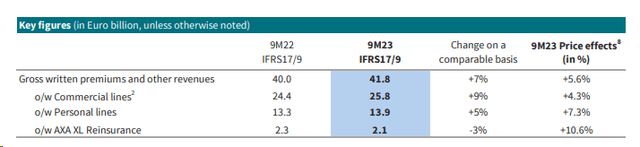

- Higher revenue generation: Here at the Lab, we expect a 5% increase in the global P&C industry. Therefore, top-tier players like AXA are better positioned to increase market share penetration. Going to the Life division, personal lines pricing activities are now accelerating. We should also consider the favorable combination of AXA Benefitting From XL’s Lower Risks and reinsurance favorable pricing dynamic, likely continuing through 2024. As a reminder, in the first 9months, XL reinsurance pricing was up by 10.6% (Fig 2). In our forecasted numbers, our pre-tax operating income reached €10 and €10.8 billion in 2023 and 2024, with an adjusted net profit of €7.7 and €8.4 billion;

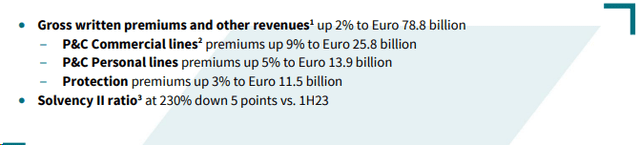

- Remuneration story: More substantial balance sheets mean potentially higher shareholders’ remuneration combined with capital rights allocation priorities. We forecast an unchanged flat solvency ratio through 2024; it is an already elevated level (in Q3, the AXA solvency ratio was at 230% – Fig 1). Indeed, the company is not only a safer investment, but its stronger balance sheet will allow AXA to withstand potential market weakness and provide options for growing capital returns payout. A possible 100 basis point EU yield reduction might impact AXA’s solvency ratio; however, the company is already well-capitalized, and we believe in a higher-than-expected payout story. The company also reiterated its commitment to evaluate disposal, and we think that Wall Street will likely appreciate any further news on the matter. We continue to see AXA’s earnings above €7.5 billion guidance, and for the above reason, if acquisitions are not in place, we might expect a buyback while growing the DPS (7% per year). Here at the Lab, we forecast a dividend of €1.82 and €1.95 in 2024 and 2025, respectively.

-

Combined ratio: With IFRS17 implementation, earnings sensitivity to lower yields should be limited. This and a favorable combined ratio dynamic make AXA a profitable growth story. Our estimates show higher net profit results thanks to a positive combined ratio development. In numbers, we implied a ratio of 91% in 2023 and 90.5% in 2024.

AXA solvency Ratio

Source: AXA press release – Fig 1

AXA XL results

Fig 2

Conclusion and Valuation

As we analyzed in March with a publication called AXA, which had an Immaterial Exposure To Credit Suisse AT1 Bonds, there are negative rumors about EU insurance exposure to Signa’s financial troubles. AXA did not comment, but from the news, we believe German insurers are involved. With IFRS17 earnings momentum, we forecast an EPS growth story trajectory for AXA (+8.5% vs a +6% sector average). This is supported by reinsurance margin expansion and pricing dynamic, asset management recovery, and life division attractiveness. We are beyond the bond yield peak, and our outlook on credit spreads is muted with a continuing price increase in the P&C division; we believe AXA is set to deliver superior returns. In this context, the company is our top pick for improving bottom-up fundamentals. At the aggregate level, the sector trades on a 2024 P/E of 10.5x and a dividend yield of 5.7%. Looking back, the insurance sector’s long-term average range was 9.5-11.5x P/E and 4-6% dividend yield. AXA trades at the bottom quartile, and we believe this is not justified. The company’s implied 2024 P/E is only 8.16x. AXA 2023 and 2024 EPS are at €3.45 and €3.78 in 2023 and 2024, respectively. Therefore, valuing AXA with a 10.5x P/E (in line with the sector), we arrived at a price target of €36.22 per share ($39 in ADR) (our previous buy rating was at €31 per share). The company’s dividend yield is also higher (6% vs. 5.7%). Downside risks include lower capital position due to macroeconomic drivers like inflation, interest rates, and equity market movements. On a standalone basis, AXA might be affected by inflation claims and natural catastrophes. This could lead to lower margins and significantly reduce the company’s earnings.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here