")

Dear readers/followers,

Why am I so positive about Bakkafrost (BKFKF) (BKFKY) as a company? Easy – I view Salmon as one of the better future-proof protein alternative from the animal kingdom that exists. I also have a very positive outlook on this company due to a significant advantage in this company specifically. It owns 50%+ of the fish farming licenses in one of the most attractive salmon farming areas in the entire world, the islands of the Faroes.

Now, a commodity company like this is going to be volatile, and Bakkafrost does not disappoint here. It goes up and down in JoJo-like motions with different timing intervals. The last up and down was during the last 8 months, where we saw the company troughing in the fall and going up again until now.

I bought both during my last article, which you can find here from back in July of last year. I also bought more when the company fell significantly in the fall.

As a result of this, my modest position in Bakkafrost is now at a very good level and RoR, beating the market inclusive of FX, dividends, and capital appreciation.

I’ve in fact owned a stake in the company for a number of years – and here I will show my reasoning for still keeping this one at a “BUY” for the time being.

Bakkafrost – Why you want Salmon on your plate and in your portfolio

Companies with products I can taste, touch, smell, or feel somehow are companies that I tend to favor or overweight in my investment decisions – provided they fulfill all of my other demands and characteristics, of course. So, my last article on Bakkafrost was actually a few years back – and the company has done a “turnabout”, essentially yielding zero percent RoR in 3 years.

First off, you want to know that Bakkafrost as far as companies go, is a small business, despite being a big part of salmon. It has a very thinly traded ADR with less than 3500 shareholders across the world. I invest in the native Norwegian ticker (Norwegian, despite the Faroes being Danish). And despite these small tickers and few shareholders, Bakkafrost is a top-10 fish farming company – that’s global. It’s based in Glyvrar on Eysturoy on the Faroe Islands, a series of islands north of the British Isles that hold a total population of ~52000. The capital is really no larger than the capitals of some remote Canadian provinces, like the Yukon.

The company’s rich history current market cap and Faroe focus ensures they are a top employer on the island with over 1,000 employees. Despite being very globalized, Bakkafrost remains 20%-family owned.

The latest company results go to show you how good this business is – but how volatile the trends can be.

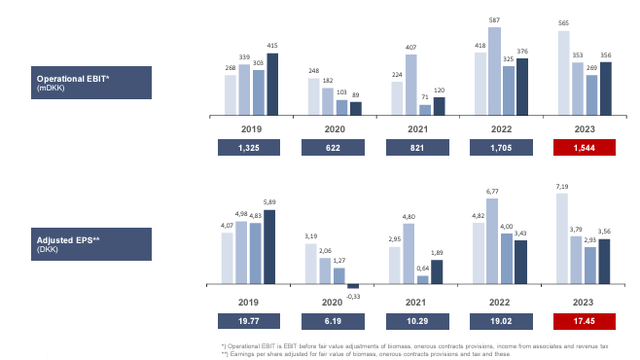

Revenues were down to around 1.5B DKK, down over 20%, but EBIT was down less than 10% on the operational side. The company also harvested over 3,000 tgw less than during the YoY period. This alone implies a price increase that consumers/customers seem to accept. The company also exceeded its high YoY in feed sales, and fish oil sales, another upside for the business.

Still, OCF turned negative and the company saw continued issues in its Scottish farming segment, leading to a dividend proposal of 8.7 DKK per share, less than I expected (But still decent for this company).

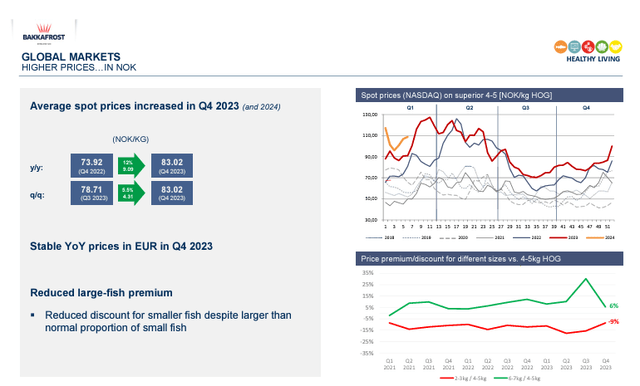

Primary drivers are global spot prices for salmon. Those were up, while the large-fish premium was down.

Bakkafrost IR (Bakkafrost IR)

Pricing held up mostly globally. Europe saw some margin pressure, but the US was stable, with good growth in China with some mixed competition in SA. The reduction in harvested products was not just in this company, but for global, and European salmon. Only the Americas saw increases in harvest, and that was only by 1%.

The strong 1Q23 that we saw at the beginning of the year is what is carrying the company’s positive year-over-year comps on an annual basis, and enabling the company to continue to grow.

Bakkafrost IR (Bakkafrost IR)

And as before, and as I’ve covered in most of my articles, the company’s fundamentals remain very healthy. The company’s equity is up, although the ratio is down by about 100 bps, but the company is not at any worrying sort of leverage or level, even with an increase in NIBD (Net interest-bearing debt).

Also, one of the main positives for this quarter really was the exceptional sourcing in FOF, Fishmeal oil, and Feed. The company saw some massive EBIT and EBIT margin increases – over a 12% increase, with a 129% EBIT increase. Whether this is sustainable will have to be seen – but I doubt it, so the possibility of a near-term downturn in the company results in 2024 is there, I’d say.

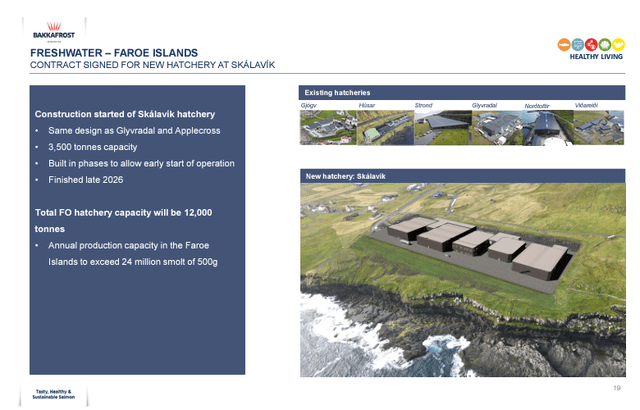

Still, the company does not let itself be bothered by the macro – and its expansion is continuing. Bakkafrost is building a new hatchery which will add an additional 3,000 tonnes of capacity to the company, with a current estimated finish in -26.

Bakkafrost IR (Bakkafrost IR)

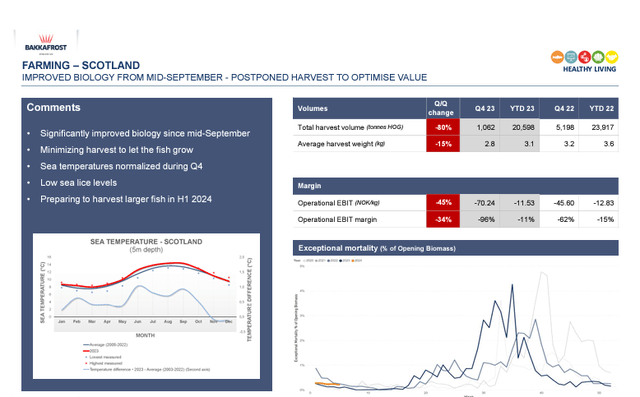

One of the reasons the harvest was so low, was also an actual postponement by the company itself. It’s focusing on letting the fish mature and get larger. The lower harvest volumes are not a result of some sort of biological problem, such as sea lice, one of the main issues with growing and harvesting salmon. Those are at an all-time low in terms of levels (Source: Bakkafrost).

Even in the Scottish geography, biology is significantly improved.

Bakkafrost IR (Bakkafrost IR)

My forecast for Bakkafrost going forward is mixed, and my “BUY” rating is no longer as strong as it once was. The company has seen a significant move-up, and we have an expectation for a reduction in global harvest rates in 2024, with no new supply growth coming in the US, and a small increase expected for the entire year.

Bakkafrost has, as of year-end 2023 already signed off almost 10% of the pre-harvested volume. With the normalization of the FOF segment, I expect the company’s 1Q to not come in at a good level on a YoY basis – the 1Q is a difficult comp, and this might lead to some weakness in the share price. Not in the company – those prospects are, as I see them, very solid, but in the valuation.

This marks a potential entry for interested parties. Here as well – I’m not shifting from buy at this time – but mainly perhaps as we pass 1Q and see a bit of normalization.

The company has moved to full vertical integration and presents, as I see it, one of the most attractive salmon companies on earth when you couple it with the company’s extremely attractive farming licenses.

Bakkafrost IR (Bakkafrost IR)

Let’s move to company valuation and see what we have going on on that front.

Valuation for Bakkafrost – Some things to like, but the upside is lower now than before

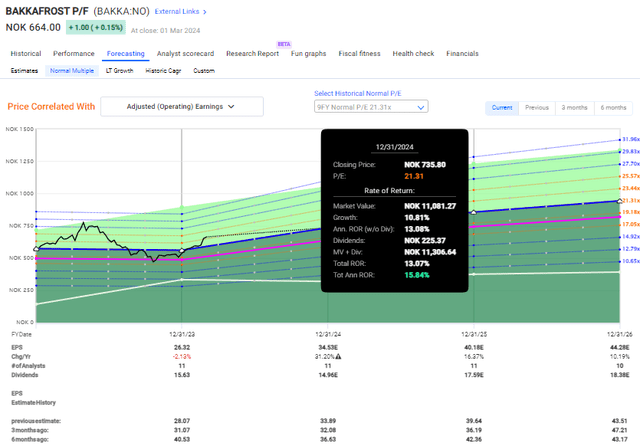

So, the simple truth is as follows; if you believe that the company is worth its 5-year average premium, then you should keep “BUY” in Bakkafrost. I believe this company is worth a premium, but I don’t think it’s as high as everyone says it should be. Still, I do see a 15% annualized upside – so I don’t shift my targets here – but I wouldn’t necessarily go all that much deeper until they drop down again if you like me are fairly exposed to your desired allocation at this time.

In fact, even at a normalized P/E close to the 10-year mark of 21x, which is where I see the company – and that would put the company at around 735 NOK at most for the native ticker in terms of P/E (means I’m giving the company a slight bump in both share price target and trim target, trim up to 800 NOK here where I would consider it “overbought”).

F.A.S.T graphs Bakkafrost Upside (F.A.S.T graphs)

Please keep in mind that this is more of a “bearish” thesis. I’m already discounting the currently accepted premium by more than 15% here. If you stick to the 5-year average, well, you get an upside of over 26% per year here to a PT of over 1,200 NOK – but I believe that to be a little too exuberant for my taste.

Also, Bakkafrost remains incredibly cyclical. The company misses estimates over 40% of the time negatively on both a 1 and 2-year basis, with high margins of error. Many of the misses were these last year, and for 2023 it was a negative 24%+ miss. Keep in mind that I said the company did not meet my expectations here.

Still, it’s a great company, and I can see a clear upside, as I believe the long-term growth trajectory in salmon protein will be unbroken, and Bakkafrost will be a clear part of this growth. For that reason, I continue to be positive about the stock, and I will give the stock another “BUY” rating at this time.

My position in this company is in fact larger than my positions in competing Norwegian businesses, such as Mowi. Bakkafrost simply does not only have better circumstances, they also execute better – the proof only needs to be looked at here, if you’re interested.

The risks to Salmon farming are non-trivial. The largest risk factor for the company concerns farming, where Bakkafrost is exposed to biological and climate risks such as storms, diseases, algae blooms, and other things. This is aside from your typical pricing and cyclicality risks. My point is, that this is not an investment where you want to be asleep at the wheel – but if you follow the trends and pricing as I do, then this can be a very profitable sort of potential.

I encourage you to take a look at Bakkafrost and see if it matches your risk profile.

Thesis

- I do need to mention that I at one point owned Bakkafrost shares acquired at a share price of 200 NOK/share. This was years ago and shows just how early I started accumulating stock in this company, which I view as the best in its field. I sold these later when the company hit close to 800, with the plan of buying them back when the company dropped.

- I did this the second time around when the company dropped below 500, then again when it touched 400 NOK, only to sell again at close to 750 NOK/share.

- Now we’re back to the third time. This time I bought at 549 NOK not long ago, I’ve raised my PT due to growth targets, and I give the company a PT of 735 NOK this time around. I’d trim once again at 800 NOK or above as of the 2024 period

- That makes the company a “BUY” for me here – and I am buying more as of March 2024, and keeping a close eye on the business.

Remember, I’m all about:

1. Buying undervalued – even if that undervaluation is slight, and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn’t go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has realistic upside based on earnings growth or multiple expansion/reversion.

I still can’t call Bakkafrost “cheap” here – it’s just not possible. But it fulfills every other criterion I hold for a solid investment.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here