Editor’s note: Seeking Alpha is proud to welcome Ignacio Llorente as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Investment thesis

Basic-Fit N.V. (OTCPK:BSFFF) presents a healthy combination of relatively low execution risk on a huge growth runway ahead, trading at an enormous discount to intrinsic value. At current levels an investment would enjoy significant margin of safety while allowing for multi-bagger potential. Additionally this investment is protected by a large and defined MOAT which puts it ahead of its competitors.

Introduction

In January 2022 I tried out Basic-Fit. After about a year I came to appreciate the value-for-money that I was obtaining and became curious about the company itself.

About Basic-Fit

Background & Founder / CEO roots:

Simple: It provides quality low-cost fitness experience in clubs that offer free-weights area, cardio area, functional training area, often a dedicated space for virtual classes and group classes area, and a stretching area.

Founder and current CEO Rene Moos, formerly a professional tennis player, opened a tennis club in the Netherlands which expanded and added fitness facilities. Eventually expanded into a large network of fitness centers called HealthCity, a mid to premium concept.

HealthCity acquired Basic-Fit in 2010. It was decided that Basic-Fit would operate under its own brand, which eventually fully overshadowed Health City.

Rene has gathered >40 years of experience managing fitness facilities and is widely acknowledged as one of (if not) the best in the industry. From listening to his interviews and studying his performance, he is prudent, honest, reactive, and acts with integrity.

Rene owned c. 15% of the company until very recently when he donated a portion to his family, reducing his stake to c. 10%.

Geographies and growth:

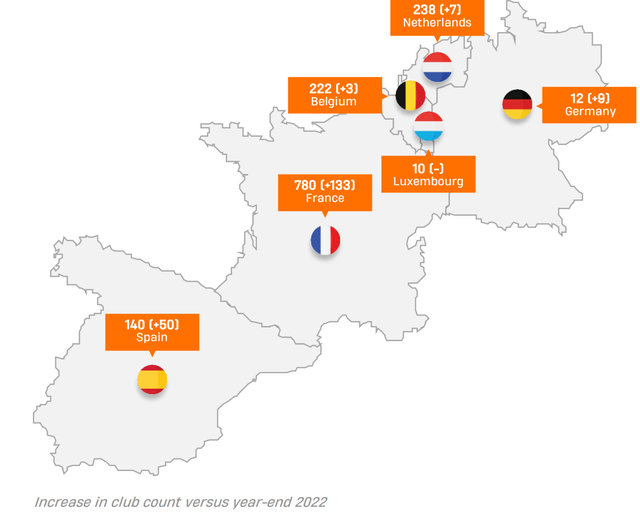

As of Q3 2023 Basic-Fit had 1,303 clubs distributed as per the image below. Note that since then Basic-Fit has announced the acquisition of one of the main Spanish competitors with c. 42 gyms in Spain, and has opened new clubs to reach c. 1,400 total clubs.

Basic-Fit Investor Presentation December 2023

In terms of future growth, according to their latest Investor Presentation they are aiming at 350 (+112) clubs in Netherlands, 350 (+118) clubs in Belgium & Luxembourg, 1,200 (+420) clubs in France, 450-700 (+310 to +560) clubs in Spain, and 650-900 (+638 to +888) clubs in Germany. The goal is 3,000 – 3,500 clubs by 2030. For reference, the largest competitor, UK’s PureGym opened 28 clubs in 2021, and 45 in 2022 and actively avoids countries in which Basic-Fit is present, operating in the UK, Denmark and Switzerland.

Interestingly, their largest competitor in Netherlands offered both low-cost option under the Fit for Free brand (87 clubs), and a mid-level offering under SportCity. In 2022 they rebranded all their Fit for Free to operate under the SportCity brand, as they realized their inability to compete with Basic-Fit in the low-cost segment.

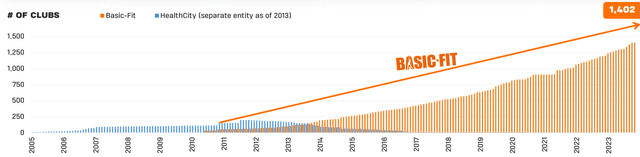

In terms of past growth, you only need to see the below metrics from their December 2023 Presentation, to understand the sheer consistency & proficiency in executing their growth plans:

Basic-Fit Investor Presentation December 2023 Basic-Fit Investor Presentation December 2023

As per their website Basic-Fit had 28 clubs when it was acquired in 2010, today they are the market leader by # of clubs in each of the markets they operate in, except for newly entered Germany.

MOAT:

The expansion strategy was executed over the past decade in parallel to the development of an important multi-faceted MOAT, which over time becomes increasingly difficult to replicate

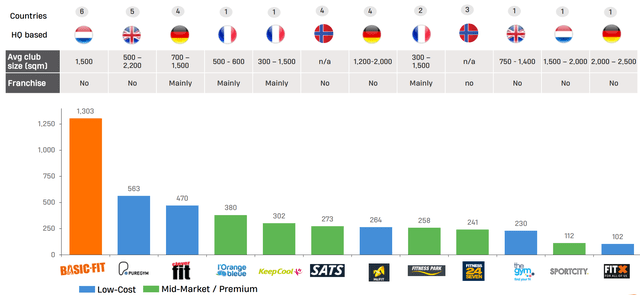

Size & Scale

By far the largest player in Europe with over twice as many clubs as the 2nd largest one. For reference Basic-Fit aims to open 200-300 clubs / year.

Basic Fit vs. Competition (Basic-Fit Investor Presentation December 2023)

Network effects

Subscription provides access to all Basic-Fits in your country (if basic membership) and in Europe (if premium membership). Its scale and growth technique described below translates to a very distinguished and attractive value proposition.

Bargaining power

Great advantage when it comes to new club Capex. As an example, average cost per square foot are c. 25% lower than competitor PureGym. Additionally, their decision to expand during Covid cemented favorable Capex negotiations, and maintenance contracts. As an example maintenance expected by mgmt to be fixed at €55k / club until 2030.

Superior technology & operational efficiency

Constant investments over the past decade in developing and improving a digital ecosystem around the offering. (i) automatization of the “gym attendance” process allows to operate gyms with no staff at all (they prefer to keep 2-3 employees / gym on average). (ii) full offering of digital services incl. nutrition & lifestyle advice, huge selection of virtual workouts and meditation sessions, etc.

Growth speed & technique

(i) They are able to simply walk inside a potential gym location with specialized cameras and AI software, and it will automatically design optimal layouts of the gyms in compliance with all regulations, and benchmark acceptable rent prices (huge time and money savings). (ii) No “gym by gym” expansion. Instead they focus on the demographic dynamics of each city & determine optimal gym locations -based on closeness to work and closeness to home – at once. As such, they expand city by city, purposefully self-cannibalizing to increase customer convenience and keep competition distant in the value proposition.

Management team:

I recommend you listen to the Capital Markets presentation from November 2023. You can hear the passion in the voice of the COO talking about what they have managed to accomplish over the past decade, and their plans for the next one. He notes with excitement that they are ready to open 300 clubs a year if they choose to. Long-tenured, passionate, realistic, and with significant net worth in Basic-Fit stock ensuring long-term alignment of interest.

Brand!

This one is quite notable. They consistently spend c. 5.5-6.0% of revenues in marketing. In a brilliant move, they offer a Basic-Fit backpack with your subscription. These backpacks must be amazing (I did not pick up mine) because they are absolutely everywhere around the cities in which they operate. It is helping Basic-Fit become one of the most recognizable logos around.

Pricing

While not priced spectacularly below their low-cost competitors, at €24.99 for the basic subscription it remains as competitive as they get, while still achieving club EBITDA margins of 40-50%.

Historical financials: Focus on free cash flow!

I will focus on the historical items that drive cash generation and I’ll spare you the smallest details. As the saying goes, it is better to be roughly right than precisely wrong.

In terms of Revenue, there are three main drivers: (i) number of clubs, (ii) avg. members / club, (iii) avg. revenue / member. To reach EBITDA you mainly have to subtract club-level Opex, Rent, and Overhead (incl. marketing)

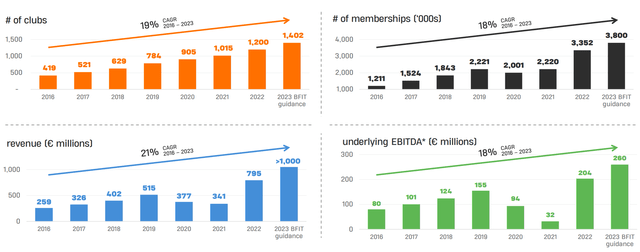

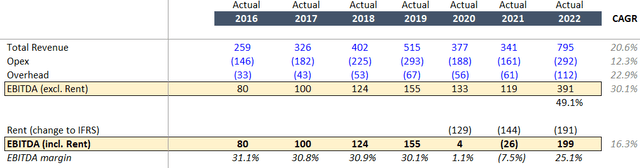

Historical performance extracted from Basic-Fit’s 2016 – 2022 Annual Reports down to EBITDA level below (€m):

Author (data from Basic-Fit historical financial reports)

As can be noted, Revenues grew at a 20.6% 6y CAGR as a result of consistent club openings, despite taking a huge hit due to Covid in 2020 and 2021, and only partial recovery in 2022. Management made the strategic decision to continue their expansion efforts during Covid through debt issuances and equity raise, which proved to be of great relief to suppliers at a time when no other gym was investing in growth. These efforts have translated into very strong relationships with suppliers and favorable conditions in future Capex & maintenance contracts.

The Opex grows significantly lower than Revenue, while Overhead grew slightly faster to develop the company’s growth capabilities and other cost control initiatives.

Historical EBITDA margins (IFRS reporting since 2019 turns rent into a Lease liability and therefore it is not considered an operating expense anymore, while I prefer to keep subtracting rent from revenue to calculate EBITDA, therefore focus on EBITDA incl. rent)were stable at c. 30-31% except for Covid years. In 2022, the company generated €199m of EBITDA with a low 25% margin.

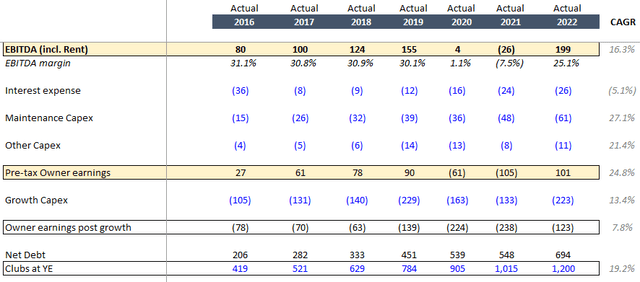

Looking at the cash items below EBITDA we have some cash outflows: related to cost of debt in interest expense, maintenance Capex for existing clubs, and other Capex (technology investments & other).

Author (figures from Basic-Fit historical financial reports)

We arrive at the pre-tax owners’ earnings.

This is the amount of hard cash the company can choose to do whatever it wants with. Given that they have a successful product and a European market to conquer they have invested all of it, and more (through debt), in growing the number of clubs. You can see their cash deployment in “Growth Capex” towards new clubs, partially financed through the Debt as seen in the increase “Net Debt”.

Any time “Owner earnings post growth” is negative the company requires some amount of debt to fund the expansion. Since they tripled the clubs from 419 in 2016 to 1,200 in 2022, debt has always been required.

Financial projections

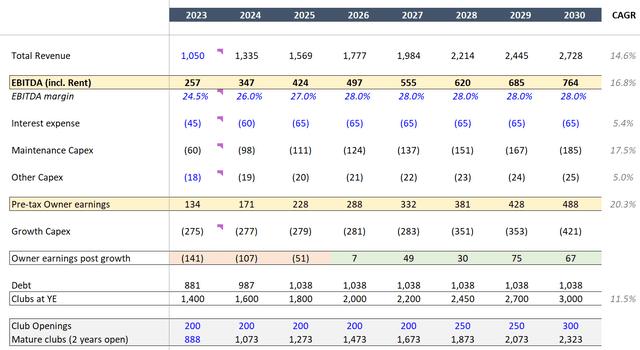

Towards the future you’ll see below my conservative projections (€m):

Author

To calculate total revenue I multiply revenue per member x number of members per club (3,250 on avg. per mature club, in line with mgmt. expectations, and 1,500 for non-mature clubs) x number of clubs.

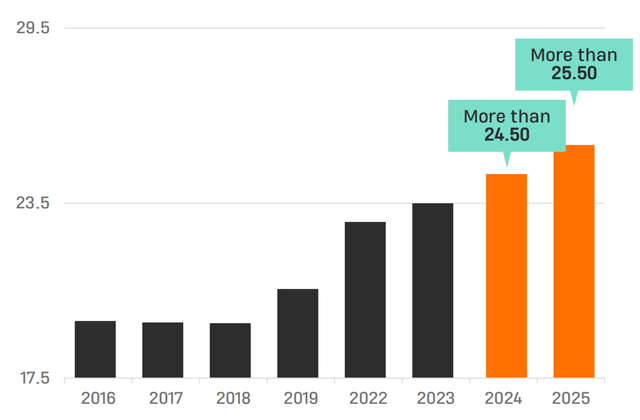

Avg. Revenue / member / month (13 months due to charges every 4 weeks) of €24 for 2024 and €24.5 by 2025 thereafter, so quite conservative as following price increases from €19.99 & €24.99 (basic and premium), to €24.99 to €29.99 respectively, as well as enhancements of perceived value of premium membership management expressed in the latest Capital Markets day the following expectation:

Yield per member evolution (Basic-Fit December 2023 Investor Presentation)

In terms of EBITDA margin: Despite improving operating metrics in 2023, inflation on wages as well as high electricity prices will take a toll on the margin. 24.5% margin seems quite conservative. I assume gradual recovery up to 28% (electricity issue is already confirmed to be solved for 2024), never reaching historical 31% levels again. This is conservative as their Overhead should increase slower than their revenue, and the increase in yield / member should directly flow to the bottom line.

Interest expense: I assumed a gradual increase to €65m / year, from €23m in 2022 as you can see in the Historicals, implying a cost on all debt of c. 6% including on new debt raised towards 2023 – 2025 growth plans, reaching a maximum of €1,038m. This CoD is much, much higher than historical figures. But let’s be safe.

As for the Maintenance Capex mgmt confirmed €55k / year / club until 2030 through agreements. I use €65k, to be safe. Finally for Other Capex c. 5% growth per year assumption is used.

Importantly, Growth Capex: Historically €1.2m / new club. Mgmt expects €1.25m. I assume €1.3m, plus a buffer of 0.7% to replace clubs that close. The number of club openings is in line with mgmt goal of 3,000-3,500 by 2030. I assume the low end of 3,000. This is very much feasible given they opened 185 in 2022, and >200 in 2023.

As seen in the line “Owner earnings post-growth”, to grow at a rate of 200 clubs / year they’ll need to continue using some debt financing until approximately end of 2025. After that, the company should be absolutely self-sufficient (in line with mgmt guidance).

In the line “Pre-tax owner earnings”, aka, hard-cash for the company to do what it wants with, will conservatively 2x by 2026, and c. 4x by 2030 from 2023 figures.

A note on franchising: While management has announced its intention of exploring franchising options to grow quickly in markets where they are not present, and leverage their extensive knowledge and technology, I’m assuming zero value will come from this (even if I don’t believe it).

Valuation

At time of writing, the stock is trading at c. €23.7, for 66m shares outstanding for a market cap, or equity value of c. €1,560m.

Zero growth perpetuity

The company today (2023) is generating c. €134m in pre-growth owner earnings yielding of 8.6% (or a 11.6x P/FCFE). Not bad at all.

Pro-Forma Owner Earnings Yield

Additionally, their clubs take c. 2 years to reach full potential or “maturity” as they call it, and c. 400 out of their current (as of Q3 2023) c. 1,300 clubs are still maturing.

In my projection you’ll see that by just 2026, this yield increases to c. 18%, again without a fully mature club base.

According to mgmt the combination of (i) maturing clubs and (ii) a noted increase in yield per member, translates to nearly doubling current EBITDA in the long-term with no additional clubs!

But let’s ignore all that and value a perpetuity based on their 2023 pre-growth owner earnings of €134m at an arbitrary 6.5% discount rate = €2,065m. That is an implied €31.3 per share, or a 32% upside from current trading levels. Any growth of that figure, including maturing existing club base, margin expansion to historical levels, new club openings, etc., represents additional upside.

2030 perpetuity

Assuming the company reaches its target of 3,000 clubs by 2030, using my projections we estimate a pre-tax owner earnings of c. €488m (again without a fully mature club base).

The value of such perpetuity using a 6.5% discount rate would translate to an equity value of €7,512 in 2030, or a 4.5x MOIC.

EV/EBITDA

If we take the 2022 EBITDA of €200m, a market cap (equity value) based on €25 per share of €1,650, and a Net Debt of €880m assumed for YE 2023 (it was €810 1H 2023) we reach an Enterprise Value of €2,530, implying a current EV/EBITDA multiple of 12.7x on 2022 figures, 9.8x on 2023’s estimated EBITDA of €257m, and 7.3x on 2024’s €347m EBITDA.

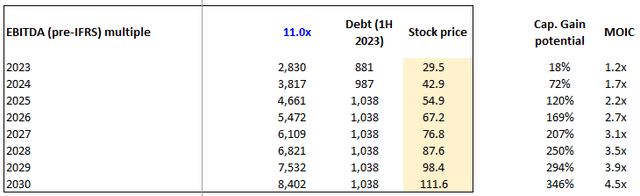

In terms of EV / EBITDA: Using a conservative 11x (ignoring an avg. of 14.4x during 2017, 2018, 2019, and 2022) we obtain the Enterprise Value, which I adjust for projected levels of debt, to reach the implied stock prices:

Author

As you can see, there is quite some margin suggesting a 2x MOIC by just 2026.

It becomes clear that on the downside, a buyer is protected by the level of cash flows the company is able to generate today, which already present a highly attractive investment without any growth considerations.

On the upside, there is significant potential for this to be a highly lucrative investment, if the investor possesses the patience required.

The asymmetry in risk-reward is truly surprising.

Why is such a good business available for so “cheap”?

Management is long-term oriented. Wall Street tends to be more focused on short term objectives which in my opinion are missing the bigger picture. In the article linked in this paragraph you’ll read about a recent downgrade from Barclays, citing things like “Basic-Fit will struggle to meet profit expectations in the next twelve months”, or “Basic-Fit has difficulty keeping up with consensus expectations”. If you contrast these comments with the impressive execution of expansion plans over the past decade while achieving operational metrics such as 40-50% club EBITDA margins, one can discern the disconnect between analysts covering this stock, and reality.

Throughout past years, a consistent theme from equity research analysts was “when will you be cash flow positive POST-GROWTH“. Management, perhaps unwisely, kept replying “soon”. However, as you can see in my projections, soon likely means 2026 (see in my projections “Owner Earnings post-growth” line). This misalignment has led to pointless “disappointments”.

Mgmt recently finally clarified that they will be “able to finance their growth until 2030 on their own”. This is indeed mostly aligned with my projection.

Additionally, the same analysts are laser focused on # of club openings. Even the CEO seemed frustrated with this nagging concern: He recently announced they would not provide specific guidance on new club openings anymore (other than the 2030 target). They clarified that they will grow in a matter that remains financially prudent, and hence be adapted in light of economic conditions.

Another misunderstood topic is the debt. As of H2 2023 they had €810m of financial debt. People often throw Lease Debt into the mix (€1,300m) and get scared. To put simply, if you don’t repay some portion of financial debt, you are bankrupt. If you don’t repay some portion of Lease Debt (which is rent!), you are completely fine.

Another common argument is “what is their PE ratio?”. Given high depreciation, their accounting Net Income is very low. However, having an infrastructure background I know better than to focus on accounting metrics vs. the actual cash generation. Always follow the cash!

Additionally, I note a bias by which people don’t associate a low-cost provider like Basic-Fit with an absolute winner stock. No matter how apparent their MOAT becomes once looked at closely.

Finally, I will say that it seems like a largely under the radar stock. I believe this will change once it becomes too large to be ignored.

Risks / red flags:

- Top management leaving, particularly the CEO and COO.

- Top management selling most of their stocks.

- Execution risk: Problems could arise that would hinder their ability to execute their growth plan. A mitigant is a track record of over a decade executing to perfection.

- Persistent strong inflation: Actually a blessing in disguise. Economics of Basic-Fit will allow them to handle inflation better than its competitors creating opportunities to take further market share.

- Strong economic recession: As the (very) low cost provider, a recession would not be a threat to their business.

- A decline in brand reputation: This could translate to long-term deterioration of their economics as it might allow competitors to catch up, helped by consumer preference.

- War in Europe: A war in any/all of its markets could have a devastating effect on their operations.

- COVID: Should a variation of Covid or a new pandemic arise, Basic-Fit would suffer. However, it would also be an opportunity to gain market share as they are better equipped than competition to survive.

- Competition: With a massive cash injections over a significant period of time and a steep learning curve to overcome, a competitor could challenge Basic-Fit’s position as the leader in Europe. There is no inherent superiority of their value proposition other than the fact that they are the only ones offering it. However, the barriers to reaching a position to threaten Basic-Fit’s growth story are high, and thick.

- Inaccurate capital allocation decisions: Use of cash for acquisitions out of their core business would be a serious red flag.

Main Upsides not considered:

- Franchising: Correctly leveraging their technology, brand, and know-how to quickly expand in a few additional key markets could bring immense value in the future. Management announced towards the end of 2023 their intention to explore this avenue of growth, and are aiming to have a clear conclusion by end of 2024.

- Achieving an EBITDA margin similar or higher to pre-Covid levels, which is entirely possible.

- Faster club rollout than anticipated through my conservative projections.

Conclusion:

A category leader managed by a highly experienced team striving for perfection in operational efficiency, expansion strategy, technology development, and capital allocation. At least for now, its execution of growth has been far, far superior to that of its competitors.

The company is trading at an inexcusable discount to its intrinsic value, by any metric.

Putting my money where my mouth is, I have made Basic-Fit my biggest holding. I hope to have very good news in a few years, and extremely good news in a decade.

Thanks for reading.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here