")

We’re upgrading Broadcom (NASDAQ:AVGO) to a buy post-4Q23 results and outlook. We now think our negative thesis of AVGO’s A.I. growth not being enough to offset macro weakness and drive outperformance has been priced into the outlook for next year. Management now guides FY24 revenue of ~$50B, trailing the consensus of $52.34B. On the call, management noted that $2B (EUC and Carbon Black) from the VMW acquisition would be divested, so the FY24 outlook was lowered. In spite of the current macro headwinds and the cyclical correction, we see room for upside supported by a new product cycle and increased content in FY24 in AI acceleration, cloud networking, broadband access, and enterprise storage end-markets. We also believe that the company is now better positioned to beat its guidance for FY24. The following outlines AVGO’s FY23 growth.

4Q23 earning results

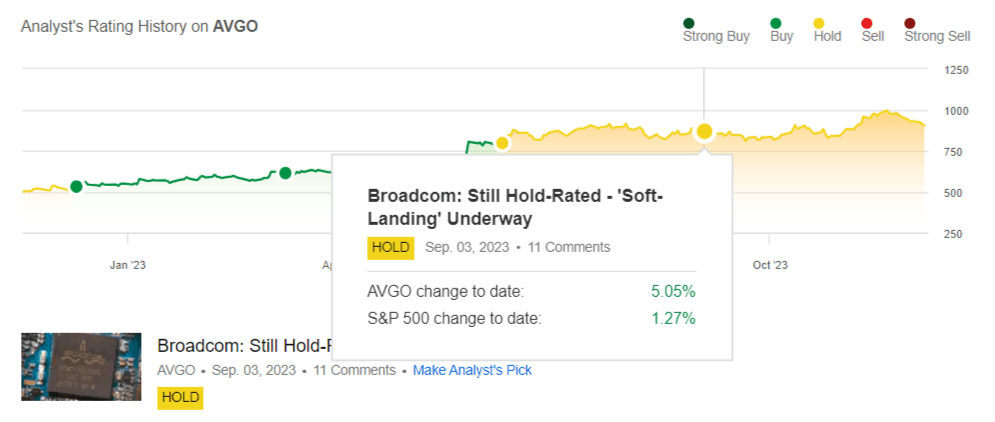

Our neutral rating has played out; since our last note in early September, the stock has been trading sideways, up 5%, versus the S&P 500, up 1% during the same period. We see better entry points into the stock at current levels and recommend investors begin adding on pullbacks.

The following outlines our rating history on AVGO.

SeekingAlpha

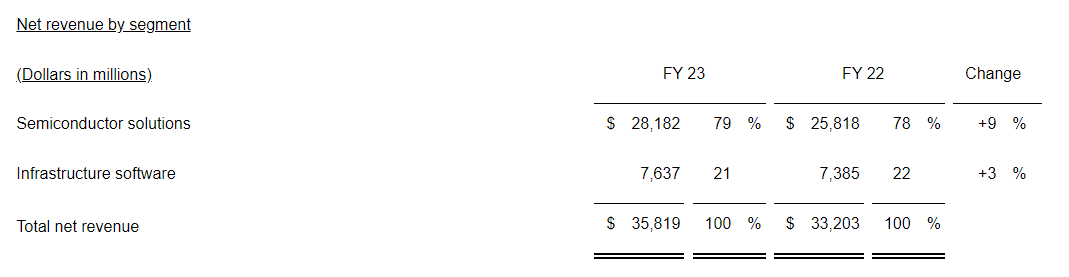

Additionally, management performed in line with its guidance last quarter without upside surprise; semiconductor solutions, representing 79% of total sales, grew 3% Y/Y to $7,326M compared to 21% Y/Y growth in 1Q23 to $7,107 and forecasts of 3.5% Y/Y and 6% QoQ growth last quarter. We now see demand tailwinds for the company’s semiconductor solutions business due to increased content in FY24 in AI acceleration, cloud networking, broadband access, and enterprise storage end-markets. Additionally, we’re constructive on management, exercising discipline in shipping to double-ordering and customer inventory correction. The following outlines AVGO’s net revenue by segment for 4Q23.

4Q23 earning results

Valuation

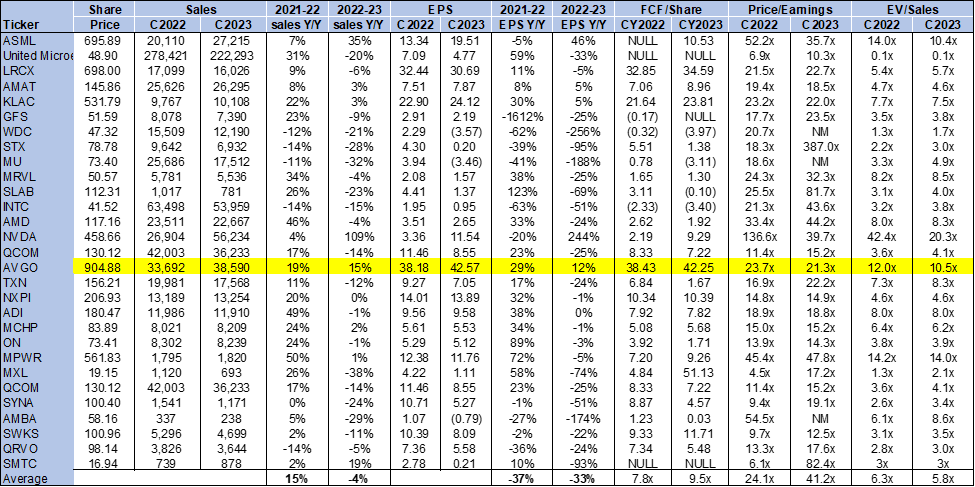

AVGO is expensive, trading well above the peer group average. The stock is trading at 10.5x EV/C2023 Sales, versus the peer group average of 5.8x. We think the premium valuation is somewhat justified at current levels; we see more room for top-line growth in 2024 as end market correction completes and AVGO gets more customer traction due to its new product cycle. On a P/E basis, the stock is trading at 21.3x C2023 EPS $42.57 compared to the peer group average of 41.2x.

The following chart outlines AVGO’s valuation against the peer group average.

TSP

Word on Wall Street

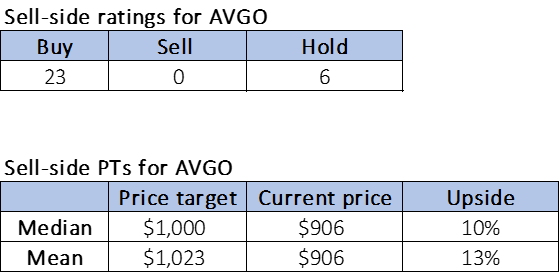

Wall Street shares our bullish sentiment on the stock. Of the 29 analysts covering the stock, 23 are buy-rated, and the remaining are hold-rated. The stock is currently priced at $906 per share. The median sell-side price target is $1,000, while the mean is $1,023, with a potential 10-13% upside.

The following outlines sell-side ratings and price-targets on AVGO.

TSP

What to do with the stock

We’re moving AVGO to a buy after a neutral stance. We think the company’s A.I. growth is now better gauged by market expectations. We see a clearer growth path for AVGO going forward, particularly after the closing of the VMW deal. We also think the share repurchase program will increase investor confidence in the stock into 2024. We think the stock’s risk-reward profile is becoming more attractive, and we recommend investors explore entry points in the near term.

Our investing group, Tech Contrarians, discussed this idea in more depth alongside the broader industry and macro trends. We cover the tech industry from the industry-first approach, sifting through market noise to capture outperformers.

Feel free to test the service on a free two-week trial today.

Read the full article here