")

When analyzing Bitcoin miners, I like to look at the mix of the miner’s synergetic optimization, which includes hash rate optimization, energy efficiency, cooling efficiency (if the data is available), and software and firmware optimization and utilization. Beyond synergetic optimization, I think it is also important to look at the miner’s strategic planning which includes mergers and acquisitions, product or service diversification, and adaptability in the mining space. Adaptability entails the ability, for example, to upgrade hardware to effectively compete for block rewards if mining difficulty increases, or the ability to quickly source cleaner energy if regulation demands so.

This article delves into the latest developments at Cipher Mining (NASDAQ:CIFR) as we approach the halving event, and the miner’s synergetic optimization and strategic planning based on data and insights gleaned from the Q3 earnings release and the latest operational report (November 2023).

Prep for the Halving and Beyond

Countdown to the halving event has begun and one of the main focus of Bitcoin miners is to maintain the maximum operational efficiency post-halving, as block rewards (the main source of revenue) will be cut in half. Pre-halving, BTC miners typically start aligning their operations in anticipation of the halving event by acquiring advanced hardware (in some cases more mining facilities) to push their hash rate to a higher level, as they aim to offset the reduction in block rewards and maintain a profitable business in the post-halving era.

Cipher Mining is gearing up for substantial growth, and its strategic planning is on point. The company recently acquired an ERCOT-approved mining site in Texas, called Black Pearl, under a purchase agreement with Trinity Mining Group. Black Pearl, has an interconnection capacity of up to 300 megawatts. In terms of power capacity or mining rigs, Black Pearl is anticipated to outsize Cipher’s other mining sites.

The company’s total self-mining hash rate at the end of Q3 was 7.2 exahash per second (EH/s) and an additional contracted 1.2 EH/s capacity from the newly acquired Bitmain rigs, making the current total hash rate of 8.4 EH/s. The completion of the Odessa facility is one of the main highlights of Q3. As of the third quarter, the Odessa facility was generating ~6.2 EH/s, using ~207 megawatts of power. The facility had mined roughly 3,531 Bitcoins YTD at the end of Q3, at an all-in electricity cost of ~$8,390 per BTC, with a recent maximum daily mining capacity of ~12.9 Bitcoins per day. The Odessa site currently runs ~90% of Cipher Mining’s BTC production.

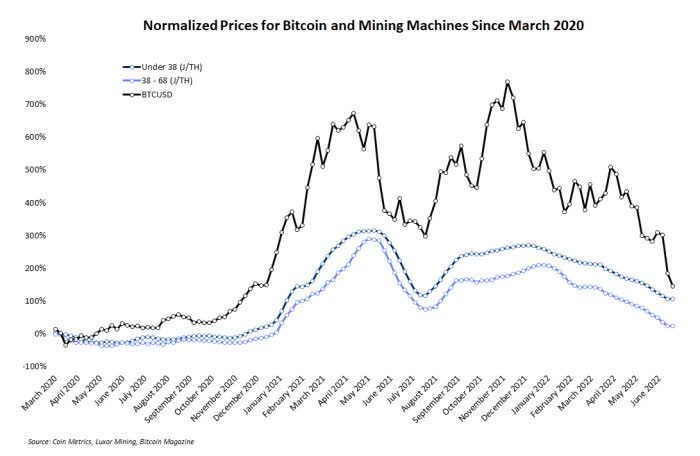

Bitcoin vs Mining Rig Price (Coin Metrics)

I’m impressed with the strategic planning of Cipher Mining in its rig purchase timings. The company is taking advantage of the cyclical nature of mining rig prices. Rig prices typically follow the Bitcoin price trend (as seen in the chart above), so they cost more in Bitcoin bull markets and are priced lower when the bear market kicks in. The company has been purchasing rigs at an average cost of $14 per terahash (TH/s). Cipher Mining announced yesterday (December 18) that it had entered an agreement to purchase 37,396 latest-gen Bitmain T21 mining rigs (which represent 7.1 EH/s). The Black Pearl site will be built using some of these rigs. The miner also has an option to acquire another 8.7 EH/s of T21s in 2024 and plans to reach 23.5 EH/s by 2025. The market reaction to the T21 rig purchase news was positive, seeing the stock price jump 17% in a single day.

By locking in our price for mining rigs at a very attractive $14/TH, we are controlling our biggest potential capital expense and locking in favorable terms ahead of what we believe will be a bull market for Bitcoin.

– CEO Tyler Page

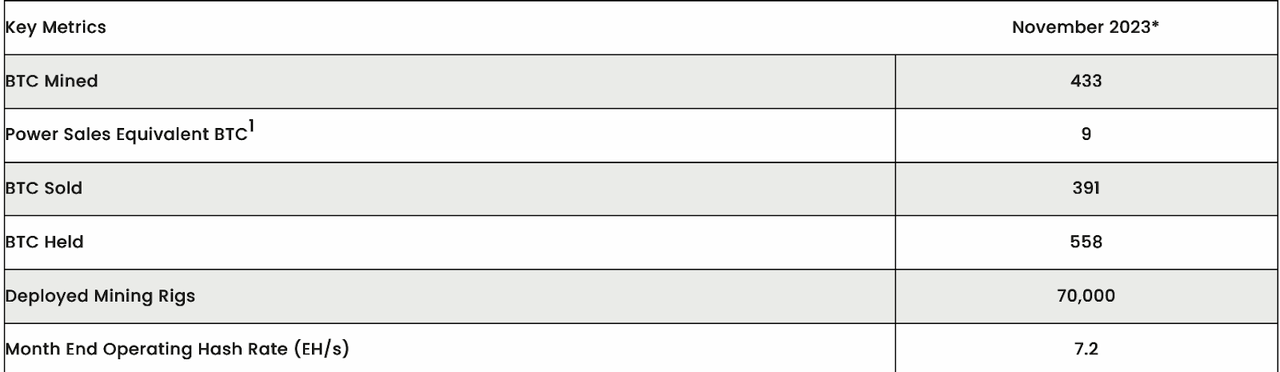

November Production Data (Cipher Mining)

Cipher Mining achieved an all-time high site hash rate of ~6.24 EH/s in November at the Odessa site, produced a total of 433 BTC from all its mining facilities, and held a total of 558 BTC. Cipher Mining produced ~5 more BTC compared to October’s total BTC produced with the same number of rigs deployed and amidst increasing BTC mining difficulty. This suggests a good level of synergistic optimization in Cipher Mining’s operations.

Cipher Mining – Financials and Valuation

Consolidated Statement of Operations (Cipher Mining)

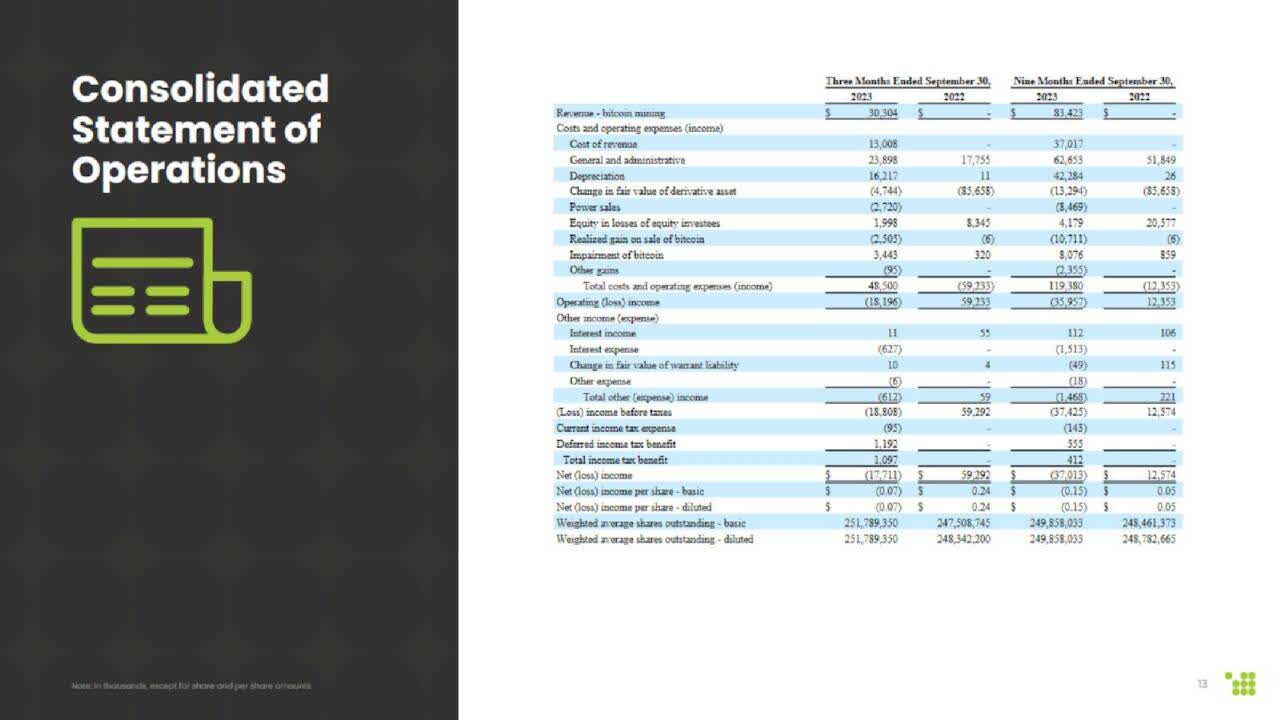

For Q3, Cipher Mining reported improved liquidity because the company’s largest site, Odessa, commenced running at full capacity and Bitcoin price started seeing significant price gains. At the end of Q3, Cipher Mining reported liquidity of $17 million, which included cash of $3.3 million and Bitcoin reserve valued at $13.7 million at the time the report was published. Q3’s total revenue from Bitcoin mining was $30.3 million. Q3’s cost of revenue was $13 million, consisting primarily of power costs at the Odessa facility and maintenance expenses for mining operations. Cipher also reported power sales at $2.7 million and a gain of $4.7 million due to a change in the fair value of the Odessa power agreement.

Q3’s SG&A expenses increased by 34% YoY, totaling $23.9 million. The increase was attributed to an increase in the number of employees at the company and other overheads. The company had 33 employees at the end of Q3 compared to 20 employees a year ago.

Cipher Mining had a net loss of $17.7 million, resulting in a net loss of $0.07 per share. Compared to Q3 last year, where a net gain of $59.3 million or $0.24 per share was recorded. Q3 last year included a one-time accounting gain of $85.7 million for the Odessa Power Purchase Agreement. This significantly boosted last year’s operating income. On a non-GAAP basis, Cipher Mining reported a net income of $5.9 million or $0.02 per share for Q3 2023.

Peers Market Cap (Seeking Alpha)

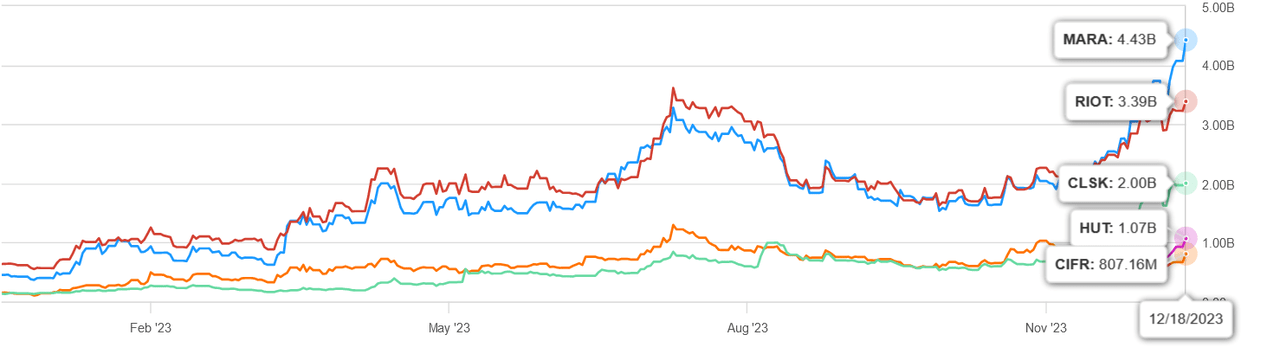

Using a weighted average market cap and P/S ratio calculation, I conducted a valuation analysis of CIFR in comparison to its peers – Marathon Digital (MARA), Riot Platforms (RIOT), CleanSpark (CLSK), and Hut 8 (HUT). The respective market caps for each company were summed up, giving a total of ~$11.7 billion. Then multiplying each peer’s P/S ratio by its market cap, summing these products, and then dividing by the total market cap gives the “market cap-weighted average P/S ratio,” which is 9.7x. Comparing this to CIFR’s individual P/S ratio of 7.5x shows that CIFR is trading at a slight discount to the weighted average P/S ratio of its peers and suggests that CIFR may be undervalued relative to the group.

Risks

There are lots of “ifs” in the Bitcoin mining business, as the business is tethered closely to the volatile and speculative nature of its primary asset, Bitcoin. Current speculation includes whether the SEC will approve a spot Bitcoin ETF next year, and if the price of Bitcoin will reach and surpass its 2021 all-time high post halving. This highly speculative nature is an inherent risk.

Another risk lies in the potential for dilution. While Cipher Mining may not heavily rely on stock issuance for fundraising, it does issue stocks from time to time. In Q3, CIFR issued approximately 2.8 million shares at an average fair market value of $3.12 per share. This issuance poses a potential risk of stock dilution. However, CIFR adopts a strategic approach to mitigate this risk. The company consistently sells a portion of its mined Bitcoin each month, generating monthly free cash flow. This practice affords CIFR the flexibility to capitalize on growth opportunities, cover OpEx, and fulfill existing CapEx commitments without solely resorting to continuous stock issuances.

Takeaway

CIFR impresses in both its strategic planning and synergetic optimization. The purchase of new miners at a fair price shows the strategic planning prudence of the management. While it does not hold a substantial Bitcoin reserve compared to some of its peers (MARA currently holds over 13,000 BTC and HUT holds over 9,000 BTC) its “sell some, keep some” approach offers benefits that directly affect the company and investors.

We are at an important inflection point for the company as we pivot to the next stage of growth, and we are excited to be expanding and investing in advance of what we hope will be a bull market for Bitcoin in the months and years to come.

– CEO Tyler Page, during the Q3 Earnings Call

The coming year is anticipated to be a very bullish year for Bitcoin and miners, and CIFR could be a good addition to any Bitcoin-related stock portfolio as the latest developments have shown that the company is rightly positioned to capitalize on next year’s anticipated momentum.

Editor’s Note: This article was submitted as part of Seeking Alpha’s Top 2024 Long/Short Pick investment competition, which runs through December 31. With cash prizes, this competition — open to all contributors — is one you don’t want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

Read the full article here