")

Overview

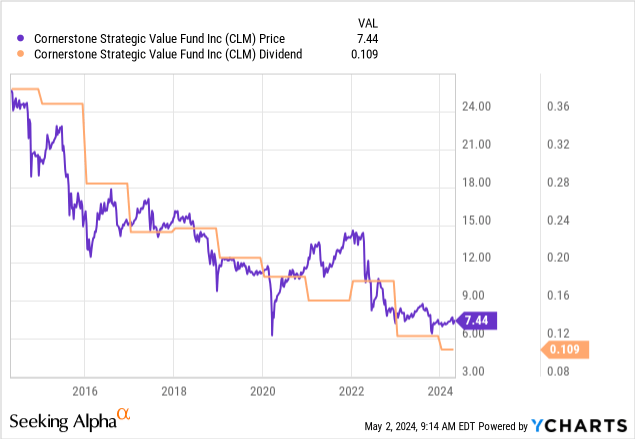

Taking a look at the price chart of Cornerstone Strategic Value Fund (NYSE:CLM) is sure to scare away some first-time viewers. The price has fallen by over -70% in the last decade alone. However, this Closed-End Fund’s appeal is all in the high dividend yield. Since this is an income-focused fund, the price decline hasn’t scared away the veterans who have held on to CLM for an extended period of time. However, I wanted to give this a fair shake and determine whether this is a sustainable choice for retirement.

Retired investors likely depend on the income generated from their portfolio to fund their expenses and lifestyle. While CLM’s yield of over 17% certainly has the power to create a large income stream with a lower amount of capital, the distribution history is inconsistent. At the same time, though, I do see the appeal of a fund like CLM when paired with a diversified group of other high-yielding assets with growing NAVs. This may include different asset classes like REITs, Business Development Companies, or other high yielding Closed-End Funds. In this scenario, a decreasing and inconsistent distribution rate may matter a lot less. In addition, the makeup of the distribution can technically be a bit more tax efficient since portions of it contain return of capital.

Like I said, I aim to give this fund a fair shake and have no intentions of attacking anyone’s current position. With that being said, the reason I question the sustainability is because the fund has a very poor NAV growth over time. The NAV (net asset value) of the fund has been absolutely decimated since its inception in 1987, despite giving you a pretty diversified exposure to a basket of top-tier stocks. In the same token, CLM’s high distribution has partially compensated for this NAV destructive through it’s high distribution rate.

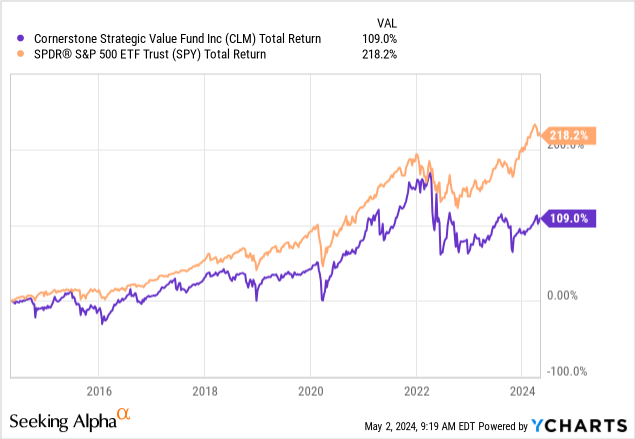

Somehow, the fund has managed to keep up a positive total return over long periods of time. Over the last decade, you’d still have managed to pull in a total return of over 100% with CLM. While this underperforms the S&P 500 (SPY), that’s totally fine, since I would imagine most retired investors don’t really prioritize staying on par with the greater index. However, this total return does not include investors taking advantage of the dividend reinvestment benefit as well as strategically maneuvering rights offering. I will circle back to this later on.

Strategy & Internals

So how exactly does CLM work as a fund? CLM is an actively managed fund operating as a Closed-End Fund that maintains exposure to a wide variety of growth and value stocks. The fund remains highly diversified across many sectors, even including real estate. As of the latest 2023 annual report, Information Technology remains the higher percentage of net assets amounting to 22.3%. This is followed by CLM also having 17.8% exposure to other CEFs, 11.1% to financials, and 9.5% in healthcare exposure. Here are the current top ten holdings:

| Holding | Sector | % of Net Assets |

|---|---|---|

| Apple Inc. (AAPL) | Information Technology | 7.2% |

| Microsoft Corporation (MSFT) | Information Technology | 6.6% |

| Alphabet Inc. – Class C | Communication Services | 3.8% |

| Amazon.com, Inc. (AMZN) | Consumer Discretionary | 3.6% |

| NVIDIA Corporation (NVDA) | Information Technology | 3.0% |

| Invesco QQQ Trust ETF (QQQ) | Exchange-Traded Funds | 1.9% |

| Meta Platforms, Inc. (META) | Communication Services | 1.8% |

| Tesla, Inc. (TSLA) | Consumer Discretionary | 1.7% |

| Technology Select Sector SPDR Fund | Exchange-Traded Funds | 1.6% |

| JPMorgan Chase & Co. (JPM) | Financials | 1.3% |

While the fund’s stated objective is to capture long-term capital appreciation, it’s obvious that it has failed to do so. It does make you wonder why the fund has failed to capture any sort of price appreciation over the last decade, when almost all of their top ten holdings have crushed it in the last ten years. In any case, their investment performance shows us that management has been able to capitalize with capital gains on investments.

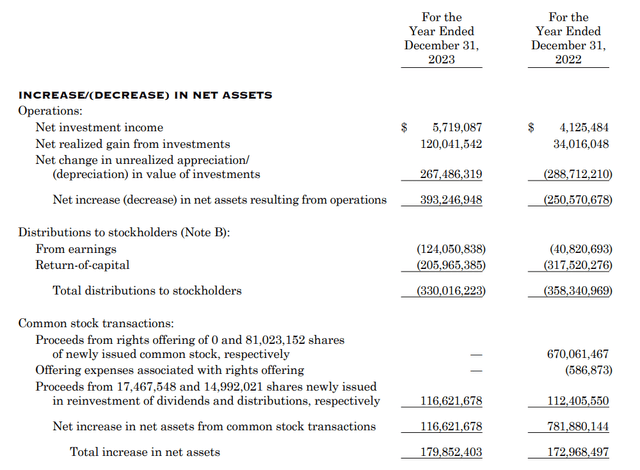

The 2023 annual report shows us that net assets increased by $392M, mostly due to unrealized appreciation of assets, as well as $115.7M of realized gains from investments. Surprisingly, only $4.29M comes from long-term capital gains. The performance of fiscal year 2023 saw a large improvement of the fund’s performance across the board.

CLM 2023 Annual Report

We can see a rise in net investment income totaling $5.7M, up from the prior year of $4.12M. In addition, we see realized gains totaling $120M, which was a significant improvement over the $34M in realized gains from the year prior. More importantly, we saw total net assets increase amounting to $393M, whereas the net assets decreased by $250M the prior year. While total distributions were lower for 2023, we can see that more of it was funded by the actual earnings rather than the return of capital. With a focus on the distribution, let’s take a look at the high yield and why it can be seen as problematic for some investors.

Dividend & Valuation

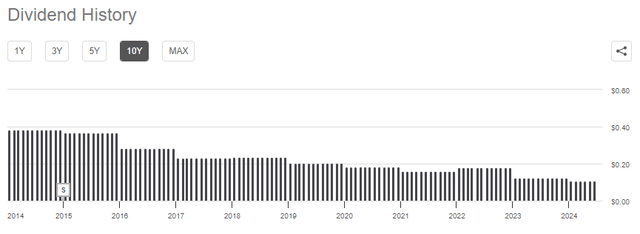

As of the latest declared distribution of $0.1086 per share, the current dividend yield sits at a whopping 17.5%. So what exactly does the breakdown of the distribution look like? Since this is a CEF, the distribution can be covered by capital gains, investment income, or return of capital. Referring to April’s Form 19a, we can see that the breakdown of the dividend mostly consisted of paid-in capital or ROC.

CLM April Form 19a

Excessive use of ROC can certainly be harmful in an environment where NAV growth is nonexistent. To be fair, the NAV has been absolutely decimated since the inception of this fund, and the continued use of ROC is likely one of the contributing factors. So how does CLM maintain a high distribution amidst a shrinking NAV and the continued use of ROC?

One of the ways is by implementing a rights offering! A rights offering is typically implemented by CEFs to raise capital from existing shareholders. This additional capital can be used to offset the lack of NAV growth by being invested into new opportunities that will benefit the fund. CLM can do this by offering investors the opportunity to purchase additional shares at a discounted price that is proportionate to their existing holding size.

Just for transparency, I’d like to add a disclaimer regarding the risk of this strategy. Following a buy & sell strategy based on timing the rights offering can be risky and requires you to be well-informed and actively participating. Buying CLM before the rights offering, failing to reinvest the dividends, and holding for extended periods of time can lead to losses.

A rights offering is beneficial on both ends of the transactions because it allows current shareholders the opportunity to increase their ownership stake while simultaneously providing Cornerstone with the additional cash to be used. CLM typically implements these when the premium to NAV sits near highs. 2022 was the last time a rights offering has taken place due to the price trading at an extreme premium to NAV of nearly 60%.

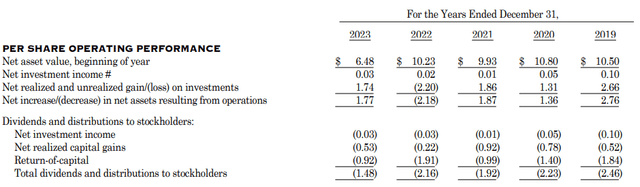

CLM 2023 Annual Report

As a result of the rights offering, we saw the NAV dip down to $6.48 at the beginning of the year. This is caused by the additional shares being issued, causing dilution to the already existing shares. While the price no longer trades at a large premium to NAV, these unique opportunities present windows to increase your dividend income by accumulating shares.

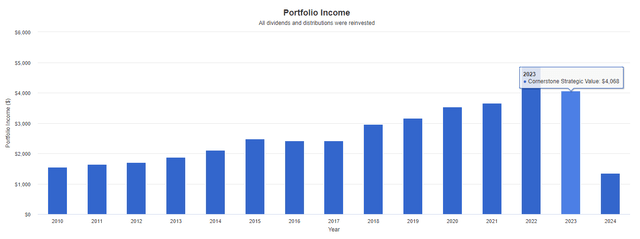

We can see how the high-yielding dividend income would have continued to grow over time using Portfolio Visualizer. Assuming a $10,000 initial investment in 2010, with dividends being reinvested, and no additional capital ever deployed, your dividend income would have grown substantially, despite the decreasing NAV and diminishing share price. In 2010, your annual dividend income would have been approximately $1,500. Fast-forward to 2023, your annual income would have now grown to over $4,000 while your position size would now be worth more than double your initial $10k investment.

Portfolio Visualizer

This doesn’t even account for the dividend reinvestment benefit you get when you own CLM. Since shares can trade at a premium to the actual NAV, CLM has implemented a benefit where you can essentially reinvest the distribution into shares priced at the NAV. However, this rule only applies when the market price sits higher than the NAV. When looking at the discount/premium history, this appears to be very frequent. This drip benefit results in immediate unrealized gains due to the difference between CLM’s price and the fund’s NAV.

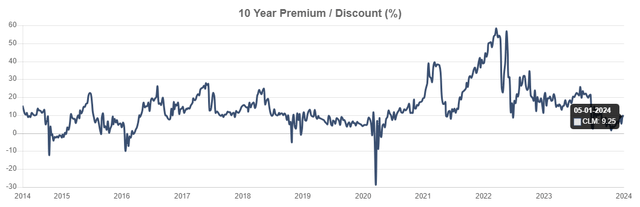

In terms of valuation, this might actually be one of the best times to enter CLM if not for the possibility of a rights offering taking place. Taking a look at the price relationship to NAV, the price has frequently traded at higher premiums than where it currently sits. The price currently trades at a premium to NAV of 9.25%. Over the last 3-year period, the premium to NAV sat a lot closer to 22.15%. Even before the pandemic, it looks like the premium commonly floated between the 10 – 20% premium range.

CEF Data

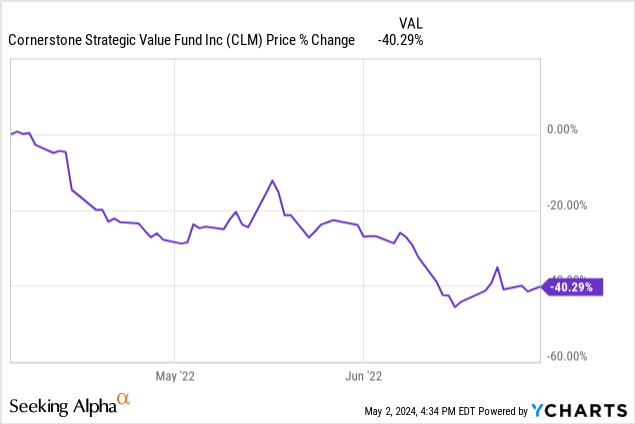

Since the price tends to fall after rights offerings, I propose a different kind of strategy rather than a buy, hold, and collect income approach. Instead, selling right before the rights future rights offerings will avoid you from holding on to shares that drop in price. Then you’d be able to accumulate more shares and increase your income at a faster rate if you reacquire shares after the initial price drop. The last rights offering in 2022 expired on June 10th. The initial rights offering was first announced on April 8th, 2022. Between these time periods, we saw the price fall by over -40% after the completion of the rights offering.

Risk Profile

I do not believe this Cornerstone fund suits every investor’s needs. To lay it out plain and simple, if you are after total return or price appreciation, look elsewhere. If you want to subscribe to the traditional dividend growth investing model where you can buy and forget about it, look elsewhere. I believe that CLM needs to be watched frequently in order to be best utilized. I sympathize with the investors who missed out on the last rights offering simply because they were not paying attention. Missing the chance to sell out before the rights offering and then buy back in at new lows was a major miss.

Seeking Alpha

In addition, without at least a partial reinvest of shares every month, you are likely to see disappointing results. The dividend payouts have decreased on a consistent basis for over a decade. However, this can be offset with continued capital being deployed by taking advantage of the DRIP discount at NAV as well as the rights offering whenever one is announced. This fund is not the equivalent of a regular tech-based CEF like BlackRock Science and Technology Trust (BST) that has a growing NAV. This is also not like a high yielding BDC or REIT where you can set it and forget it. Active participation is advised here to best utilize the fund’s ability to generate high levels of income.

Takeaway

Cornerstone Strategic Value Fund (CLM) ultimately does have lots of value that can be provided with its extremely high dividend yield of 17.5%. However, to best utilize the fund, you need to be actively aware of rights offerings, dividend dates, and figure out what is the best time to sell and rebuy. If you are someone who enjoys the lifestyle of active portfolio management, CLM is for you. The high dividend yield has been able to continue providing a positive total return, despite a shrinking NAV over time. In addition, since the distribution is funded by a majority of return on capital, the distributions are typically considered more tax efficient in nature. However, this extended use of ROC has also been a cause of stagnation of the possible NAV growth. Therefore, I rate CLM as a current Hold, with my eyes set on the next rights offering as a potential entry point.

Read the full article here