")

We previously covered Costco Wholesale Corporation (NASDAQ:COST) in September 2023, discussing its similarity to the Apple Inc. (AAPL) stock, with both stocks boasting exemplary support from existing members/ users and long-term shareholders.

We had also reckoned that the COST management might soon raise its membership fees, based on its upcoming six-year anniversary, naturally boosting its bottom line.

In this article, we will be discussing COST’s strategic growth flywheel across land/ building acquisitions and in-house manufacturing/ processing capability, funded by its highly profitable membership fees, which in turn, allows the retailer to offer competitively priced offerings at lower gross margins.

We shall also discuss why the retailer’s asset growth strategy trumps over a particular REIT.

The COST Investment Thesis Has Improved Drastically, Thanks To Its Highly Profitable And Sustainable Growth Trend

While we have been covering COST since May 2022, we only now recognize the full implications of the management’s asset-building strategy. This is why.

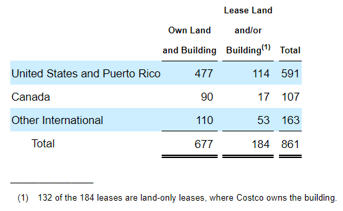

COST’s Assets by FY2023

Seeking Alpha

For example, COST owns 677 of its land/ buildings by the end of FY2023 (+2.4% YoY/ +9.1% from FY2019 levels of 620), with 132 (+4.7% YoY/ +15.7% from FY2019 levels of 114) of its leases are land-only and 52 (+1.9% YoY/ +8.3% from FY2019 levels of 48) as land/building-lease.

From the numbers above, it is apparent that the management prefers to acquire land and buildings over leasing them, with the same highlighted in its 10K, “our primary requirements for capital are acquiring land, buildings, and equipment for new and remodeled warehouses.”

The same has been reflected in its balance sheet, with an expanding net property and equipment value of $26.84B (+8.2% YoY/ +28.4% from FY2019 of $20.89B) and moderating operating lease right-of-use asset value of $2.71B (-2.1% YoY/ NA).

Most importantly, COST has guided FY2023 capital expenditures of up to $4.6B (+6.4% YoY/ +53.8% from FY2019 levels of $2.99B), further highlighting its laser focus on sustainable growth and warehouse/ logistics/ processing plants’ expansion, no matter the uncertain macroeconomic outlook.

Even then, investors may be rest assured that the management expects to achieve this growth through a mix of “cash from operations, cash on balance sheet, and short-term investments,” namely: minimal reliance on debt.

These factors have painted a much more optimistic picture for COST indeed, since the retailer has been able to achieve these impressive rates of asset growth, despite the moderating long-term debts of $5.37B (-17.1% YoY/ +4.8% from FY2019 levels of $5.12B).

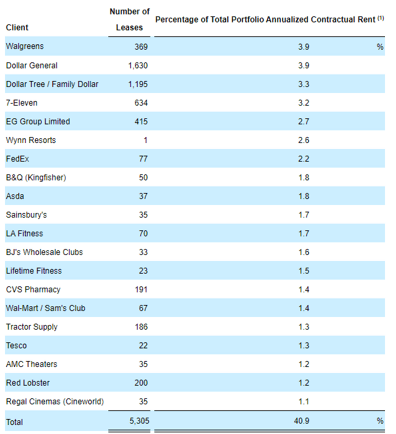

Realty Income’s 20 Largest Clients

Seeking Alpha

And it is for this reason, that we will be comparing COST’s performance against that of Realty Income Corporation (O), since the REIT leases its warehouse properties to multiple retailers, including the Walgreens Boots Alliance, Inc. (WBA), Dollar General Corporation (DG), CVS Health Corporation (CVS), and Walmart Inc. (WMT).

For context, WMT has employed a comparatively different approach to COST, with the retailer owning much of their properties in the US, while mostly leasing internationally.

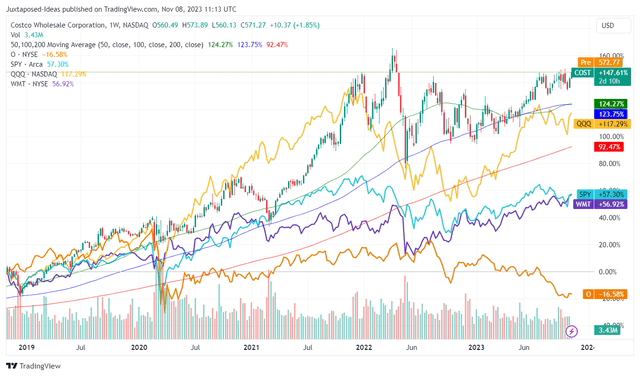

COST’s 5Y Stock Price Return

TradingView

For now, while past performance is not indicative of future performance, COST’s 5Y stock price returns of +147.61% have been more than impressive, well exceeding SPY’s +57.30%, WMT’s +56.92%, and QQQ’s +117.29% over the same time period.

Unsurprisingly, many REITs have been sold off over the past few months, explaining O’s underwhelming 5Y stock return of -16.58%, as Mr. Market increasingly worries about the elevated interest rate environment and the impact of rising interest expenses on their profitability and dividend payouts.

While O has also been growing its real estate assets from $16.56B in FY2019 to $42.23B by FQ3’23, expanding at an aggressive CAGR of +26.37%, its debt has also nearly tripled from $7.27B to $20.45B over the same time period.

This naturally triggers the expansion in its annualized interest expenses from $290.99M in FY2019 to $736.48M in the latest quarter, with a higher weighted average interest rate of 3.7% (+0.1 point QoQ/ +0.4 YoY).

For context, most of COST’s and O’s long-term debts are fixed rate debt, with any further rate hikes likely to have an immaterial impact on their interest expenses. While this means that O still records a reasonable TTM interest coverage ratio of 2.43x, this number pales in comparison to COST’s ratio of 53.16x.

Perhaps this has to do with COST’s lower payout ratio of 26.95%, triggering its lower FWD dividend yields of 0.73%, with dividends paid at the board’s discretion. This is compared to O’s AFFO Payout Ratio of 76.49% and dividend yields of 6.06%, with the REIT obligated to “distribute at least 90% of its taxable income to shareholders annually in the form of dividend.”

While their business models differ and naturally attract different types of investors, we believe that COST’s lower dividend payout is the beauty of the stock after all.

We believe that the management opts for sustainable dividend payouts that ensure the success of the company’s growth plan through land/ building acquisitions and investments into its highly efficient processing plants, which then supports the retailer’s bare-bones retail gross margins of 10.57% (+0.09 points YoY) in FY2023.

This in turn drives consumer loyalty, due to the immense value they are getting from the retailer’s well-diversified high-quality competitively-priced offerings, which then, drives its membership fee revenue growth to $4.58B (+8.5% YoY) and sustains its stellar renewal rates of 92.7% in the US (-0.3 points YoY) and 90.4% globally in FY2023 (+0.4 points YoY).

In addition to the above, COST continues to record a stable share count since FY2019 and 5Y Dividend Growth Rate of +12.37%, implying the management’s stellar capital allocation across business expansion and shareholder returns.

COST’s execution proves to be exemplary, in our opinion, when compared to O’s choice to grow at all costs, with an underwhelming 5Y Dividend Growth Rate of +3.69% and shareholders consistently diluted, as the REIT’s share count grows from 316.16M in FY2019 to 709.17M in FQ3’23.

For context again, WMT records an underwhelming 5Y Dividend Growth Rate of +1.86%, with the management preferring to use its cash to deleverage its balance sheet from $44.41B in FY2019 to $38.86B by the latest quarter. This is on top of the sustained share repurchases from 2.86B to 2.7B, with a decline in asset value from $127.04B to $123.99B over the same time period.

For now, COST’s profitable growth strategy, as discussed in depth above, has proven why it ultimately wins over many REITs’ strategies, including O’s, of buying/ selling assets and collecting rental, through shareholder dilution and debt leveraging, while having to continuously offer competitive dividend yields.

This is especially true since COST continues to collect both land/ property assets thanks to its highly profitable membership fees, which directly contribute to its growth flywheel, as it expands its presence in multiple global locations and enrolls new members.

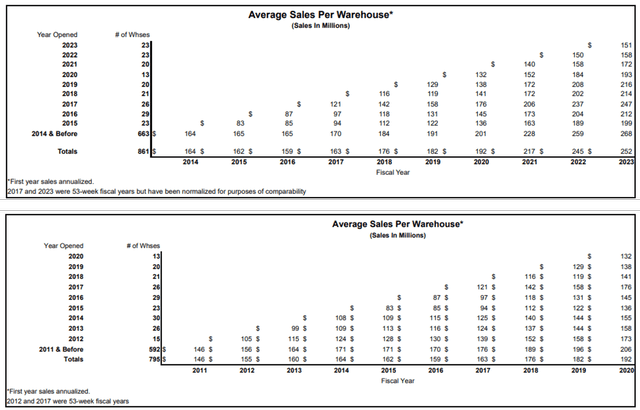

COST’s Average Sales Per Warehouse

COST

It may also be interesting to note that COST has been releasing its annual Average Sales Per Warehouse [ASPW] since FY2020, which further highlights the success of its expansion plan since 2011, with its total ASPW growing from $146M in 2011 to $252M in 2023, expanding at a steady CAGR of +4.65%.

Most importantly, it is apparent that the retailer has a highly powerful branding identity, as demonstrated by the increased speed at which its successive warehouse openings grow their first-year ASPW from $105M in 2012 to $151M in 2023.

This implies the great consumer demand for COST’s offerings, further underscoring the success of its membership-only strategy with minimal shrink reported.

We are very impressed by these feats indeed, since they further demonstrate why Mr. Market continues to rate the stock with its well-deserved premium.

The Fee Hike May Not Come So Soon After All

While we previously believed that COST may introduce a membership fee hike in this particular earnings call, we have been proven wrong indeed.

It seems that they prefer postponing the fee hike, for so long the macroeconomic outlook remains uncertain, based on the management’s commentary in the recent earnings call:

My answer, of course, is a question of when, not if. It’s a little longer this time around, since June of ’17. So we’re six years into it and – but you’ll see it happen at some point…

Post June 17th, we were in the high – the headline every day was inflation and (recession) economy. And so, we’re doing great. We’ve got great loyalty. If we wait a little longer, so be it…

These say about all the attributes of member loyalty and member growth. And frankly, in terms of looking at the values that we provide our members, we continue to increase those.

We suppose the COST management has a good point here, with many Americans already suffering from tightened discretionary spending as the inflation remains sticky with interest rates still high, worsened by the restart of the US federal student loan from October 2023 onwards.

This is especially true since the retailer’s operation in the US comprises a large portion of 591 warehouses, or the equivalent of 68.6%, of its 861 global warehouses by the end of 2023.

It may be more prudent to wait a little longer after all.

So, Is COST Stock A Buy, Sell, or Hold?

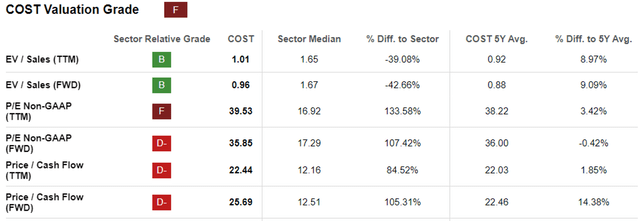

COST Valuations

Seeking Alpha

For now, we can finally understand why COST’s FWD P/E valuation remains elevated compared to the sector median, attributed to its highly profitable growth trend discussed above.

We believe that the stock’s long-term upside potential remains excellent to our price target of $678.28, based on its FWD P/E valuation of 35.85x and the consensus FY2026 adj EPS estimates of $18.92.

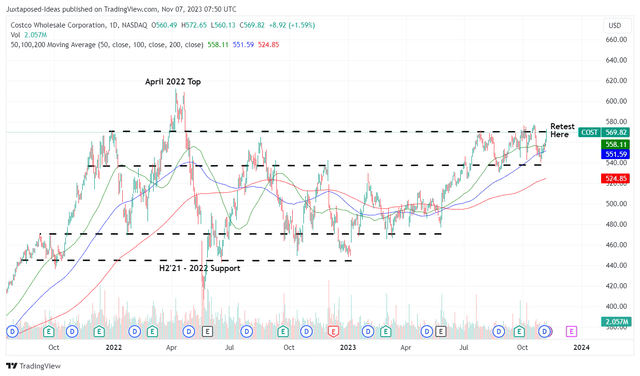

COST 3Y Stock Price

TradingView

However, we prefer to recommend patience for interested investors, since the COST stock is currently trading above its fair value of $507.63, based on its FY2023 adj EPS of $14.16.

The stock is currently retesting its critical resistance levels of $570s as well, potentially bringing forth more volatility in the near term. Investors may want to wait for a moderate retracement to its tried and tested support levels of $540s for an improved margin of safety.

In addition, investors must note that COST’s growth in comparable sales may further decelerate moving forward, thanks to the uncertain macroeconomic outlook as discussed above.

The retailer already reported a minimal increase of +4.5% YoY in October 2023’s net sales and +3.4% YoY in comparable sales (ex gas/ forex), compared to +6%/ +3.7% in September 2023 and +7.7%/ +6.7% in October 2022, respectively.

In the meantime, long-term investors may want to continue subscribing to their DRIP programs for the COST stock. This strategy has allowed us to regularly accumulate additional shares on a quarterly basis, no matter the uncertainty in the stock market.

Read the full article here