")

Crocs, Inc. (NASDAQ:CROX) is a leading lifestyle footwear brand with a stock that has outperformed the market over the past five and ten years. Accordingly, CROX posted a 5Y and 10Y total return of 28.8% and 21.6%, respectively. However, it doesn’t mean that CROX is immune to shorter-term market volatility, depending on when investors decide to enter their positions.

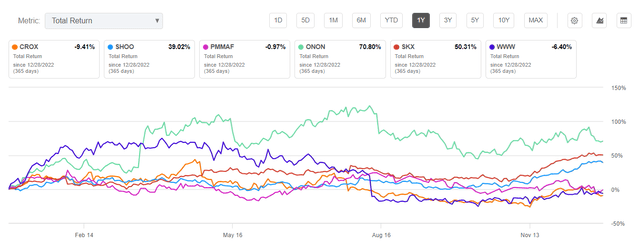

CROX 1Y total return % Vs. Peers (Seeking Alpha)

Why? Based on CROX’s 1Y total return of -9.4%, it significantly underperformed its peers set above. However, based on my previous article in mid-July 2022, CROX registered a total return of almost 78%, outperforming the S&P 500’s (SPX) (SPY) total return of 27% over the same period. My point is your entry point matters if you want to outperform the market consistently.

Observant investors should know that Crocs is a highly profitable brand with a global distribution strategy. In addition, it also has e-commerce and DTC channels, bolstering its wholesale distribution roadmap. However, CROX has experienced significant downside volatility since it fell from its late April 2023 highs after bottoming out in July 2022. Accordingly, CROX posted a decline of more than 50% through its November 2023 lows. Incidentally, CROX dip-buyers saw a fantastic opportunity to return after its initial post-Q3 earnings selloff, suggesting significant pessimism was assessed in its valuation.

From Crocs’ third quarter earnings release, investors should recall that the company revised its online strategy on HEYDUDE, as it continued to be hampered by the gray market headwinds. As a result, Crocs stopped focusing on diluting its pricing levers and turned its focus on building its brand and strategizing its product mix to compete more effectively. Furthermore, the inventory dynamics have improved, allowing Crocs more visibility into its medium-term outlook and focusing less on price competition.

As a result, Crocs needed to reflect near-term revenue growth headwinds on HEYDUDE, even though it maintained its outlook on its primary Crocs segment. Therefore, it behooved the reduction in overall revenue and adjusted EPS guidance for FY23, although the revisions aren’t expected to be structural. Accordingly, management envisaged a revised revenue growth outlook of between 10% and 11%, down from its previous estimates of between 12.5% and 14.5% increase. It also led to a reduction in adjusted EPS, as Crocs projected a revised outlook of between $11.55 and $11.85.

Despite that, the company underscored its “best-in-class” profitability, corroborated by Seeking Alpha Quant’s “A” profitability grade. Accordingly, Crocs is still expected to generate an adjusted EBIT margin of 27% in 2023, down slightly from last year’s 27.7%. These metrics are well above its 2019 pre-COVID level of 11.6%. While analysts expect Crocs’ margins to come under pressure in 2024-25, they aren’t likely to collapse back toward their pre-COVID levels, with FY25’s adjusted EBIT margin projected to be just below 26%.

Therefore, the doom and gloom over CROX’s recent demise, which fell more than 50% from its April 2023 highs, seems more like a steep pullback than a return to a secular bear market phase.

CROX last traded at a forward EBITDA multiple of 7.1x, well below its industry peers’ median of 9.6x (according to S&P Cap IQ data). Seeking Alpha Quant’s “B-” valuation bolsters my conviction that CROX remains valued at an attractive discount relative to its industry and sector peers.

However, astute investors know that valuation is just one factor in forming an investing opinion and shouldn’t be the sole decisive factor. Critically, we also need to assess whether CROX could be a value trap, suggesting market sentiments point to a secular downtrend bias, or its price action has remained constructive to buying the dips?

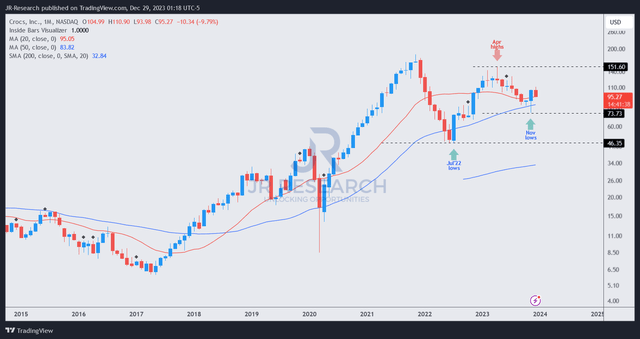

CROX price chart (monthly) (TradingView)

My analysis informed me that bullish investors need not be unduly concerned. CROX remains supported above its 50-month moving average at its recent bottom in November 2023, as dip-buyers returned after its initial post-earnings selloff.

However, some volatility was experienced by holders, likely attributed to Nike’s (NKE) caution on its market outlook on increased “promotional activity.” Therefore, it seems profit-taking occurred to cut exposure, but as long as the November low of $70 is held firmly, the long-term uptrend bias remains intact.

Consequently, I view the recent pullback as another opportunity for investors who missed its July 2022 and November 2023 bottom to add exposure, as CROX is not assessed as a value trap. While I don’t expect CROX to regain its all-time highs anytime soon, the risk/reward profile remains highly attractive to outperforming the market at the current levels.

Rating: Maintain Buy.

Important note: Investors are reminded to do their due diligence and not rely on the information provided as financial advice. Please always apply independent thinking and note that the rating is not intended to time a specific entry/exit at the point of writing unless otherwise specified.

I Want To Hear From You

Have constructive commentary to improve our thesis? Spotted a critical gap in our view? Saw something important that we didn’t? Agree or disagree? Comment below with the aim of helping everyone in the community to learn better!

Read the full article here