")

Overview

There’s something magical about collecting a dividend from business that I recently visit. For most of my life, I’ve lived within walking distance from my local CVS Health Corp (NYSE:CVS) and now I get a chance to become more than just a customer of their business. Now that the price has come down significantly, this may present an attractive opportunity for entry to pick up shares at a lower price point and ride the recovery back upward. However, being that the business is so parallel to Walgreens (WBA), I want to fully analyze what the risk profile looks like.

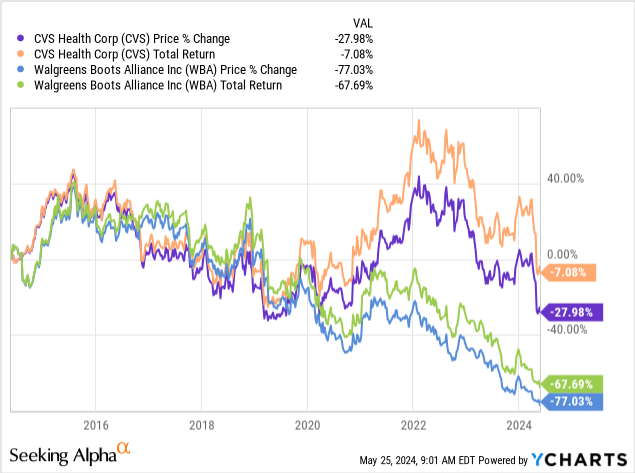

Walgreens and CVS are pretty similar on the surface level; They both operate physical stores that sell goods, with interiors that look almost the same, and they both have pharmacies that are usually at the back of the store. What differentiates CVS is that it operates through different segments which includes Health Care Benefits, Health Services, and Pharmacy & Consumer Wellness. Taking a look at the price and total return chart below, we can see that the returns and price of CVS and WBA have remained pretty aligned with one another. That is until the 2020 pandemic drop happened, we can see how the performance margin started to widen around there. So this leaves me cautious on whether or not this drop in price is the start of the same downward spiral that WBA was on.

What’s most enticing about this opportunity is that the current dividend yield sits at 4.8% which is above its usual range. This means that we have the potential to get a higher starting dividend income out of the gate. The price is now down nearly 30% on a year to date basis, falling from almost $80 per share down to the current levels. I think it would first be wise to review what exactly caused this drop and whether or not these headwinds will cause additional deterioration to the stock price.

Risk Profile

While the most recent earnings report had its own shortcoming, this price drop was already underway before these earnings. I believe it may be due to the fact that guidance for the year was slashed originally back in February. Guidance was slashed due to a rise in medical costs which have threatened CVS’s profit margin an resulted in a lower expected EPS for the fiscal year. The original estimates saw earnings per share landing at $8.50 for the year but this has now been reduced down to an EPS of $8.30.

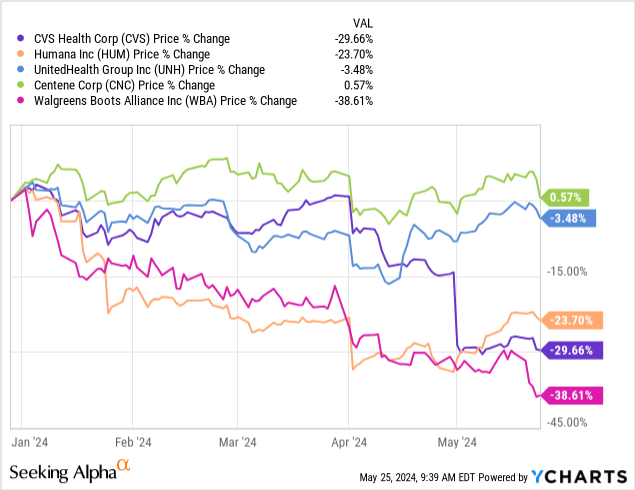

In addition, the cash flow from operations estimate decreased from $12.5B down to $12B, which I personally do not think is too bad of an adjustment because CVS may ultimately be able to offset this with some cost saving initiatives. Even through all of the increased costs, CVS managed to still raise their revenue guidance up to $371B, up from the prior $366B. My honest opinion is that a lot of the downward price movement has been a bit dramatic because these increased costs are a problem that is not unique to only CVS. Other healthcare related businesses are going through the same troubles at the moment. This shows when taking a look at the mediocre price movements of peers on a YTD basis.

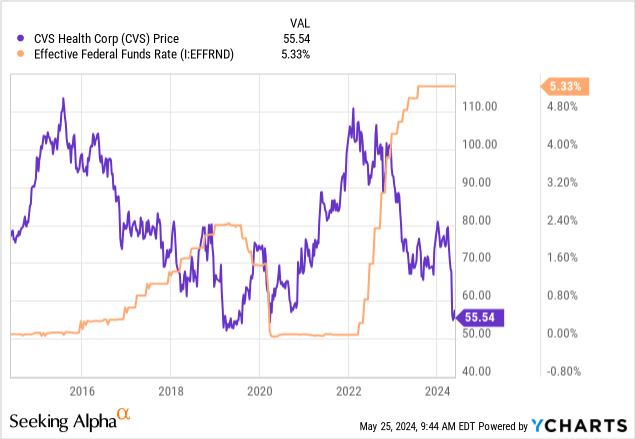

The risk outlook was only worsened by the recent earnings report from CVS. However, a lot of these increased costs and segment struggles may be a result of higher interest rates. Higher interest rates has the potential to make it harder to get affordable debt capital to fund operations and growth, slows consumer spending, and increases costs. Even looking back over a decade, we can see that CVS and the federal funds rate has always shared an inverse relationship. When interest rates were near zero levels, the price of CVS appreciated in both instances around 2015 to 2016 as well as after 2020 to 2021.

Conversely, when interest rates started to rise, we saw the price of CVS fall in the opposite direction. The healthcare industry as a whole follows this same pattern as these rates have such weighing effects of the cost of goods. Morgan Stanley believes that we may see the Fed begin cutting rates as soon as September of this year. This means we may continue to see the price slowly deteriorate until then. However, there’s also a chance that rate gets don’t happen until 2025 when you consider the fact that inflation still remains high and the labor market is still strong. These things may ultimately may the Fed push out their decision even further thereby making an entry at this price level a bit premature.

Financials

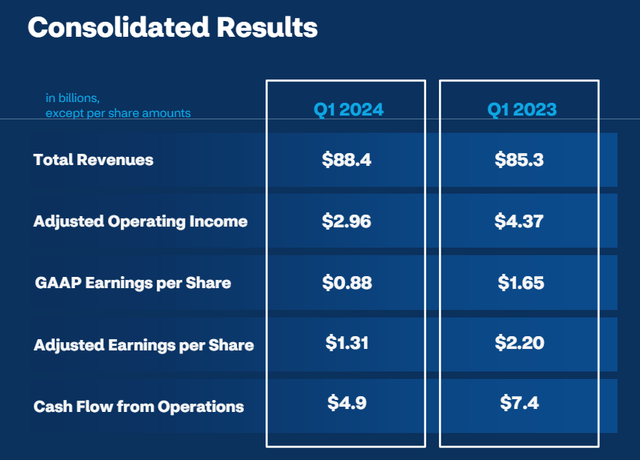

At the beginning of May, CVS reported their Q1 earnings and the results were a bit mixed. On one end, adjusted earnings per share came in at $1.31, missing expectations by $0.39. On the other hand, revenue came in at $88.4B for the quarter, representing a 3.7% year over year growth. Cash from operations for the quarter landed at $4.9B. Operating income, EPS, and cash flow from operations all decreased across the board but despite this, total revenues were able to grow.

CVS Q1 Presentation

This increase from revenue can be mostly attributed to growth within the health care benefits segment. In their Medicare business, there was an increase of 1.1 million active members which contributed to revenue growth within this segment moving up to $32.2B, an increased over the prior year’s Q1 total of $25.9B. This continued growth in members means that CVS sees total revenue for this segment landing around $129B for the entire year. This is an increase over the prior year’s guidance which saw this amounting to approximately $125B.

Additional revenue growth can be attributed to increases within the pharmacy and consumer wellness segment. This segment saw total revenues grow to $28.7B for the quarter, a slight increase up from the prior year’s total of $27.9B. This increase in revenue can be attributed to the rise in prescription volume being filled in combination with lower operating expenses. As a result, CVS saw same store pharmacy sales increase by 7% while same store prescription volume increase by 6%. However, despite the strong performance of Q1, CVS is staying conservative with their outlook and sees this segment aligning with last years performance overall.

Seeking Alpha

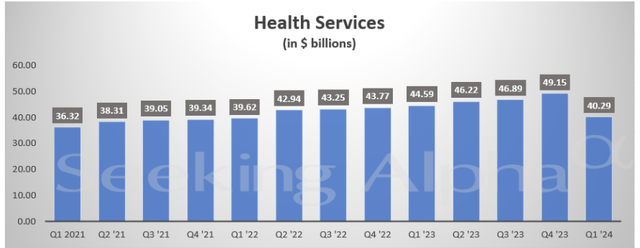

Lastly, CVS’s health services segment is where the majority of the decreases will be seen. Total revenues for the quarter decreased to $40.3B, down from $44.6B in the year prior. This can be attributed t a lower volume of pharmacy claims processed and the loss of a large client. Additionally, management has lowered guidance for revenues and adjusted operating income for the segment. Total revenues are expected to land at $167B and operating income should land around $7B, decreases from the original estimates of $168.7B and $7.4B respectively.

While decreases are never good to see, this business segment has grown steadily quarter after for 3 consecutive years now. A well-explained drop in this most recent Q1 due to cost increases and lower volumes should not result in such a dramatic downside movement. I think it’s too early to gauge how worrisome the situation is for CVS based on one quarter that fell short. I would like to see how the next few quarters play out to see if there are any improvements as well as to gauge what CVS’s efficient capital management looks like during times where revenue is not growing.

Unlike the situation that played out with Walgreens, CVS may have lower levels of cash from operations but they aren’t strapped for cash yet and the dividend remains covered. Revenue growth has averaged nearly 13% over a five year period and EBITDA growth has averaged 8% over the same.

Dividend

CVS has been a consistent dividend payer for quite some time. They maintained the same $0.50 per share quarterly payout from 2017 until the end of 2021. While this period of time had no growth, it is reassuring that they were able to maintain. Especially considering that a lot of other companies cut their dividend in 2020 to preserve capital. However, CVS started increasing their dividend again at the start of 2022. As of the latest declared quarterly dividend of $0.665 per share, the current dividend yield sits at 4.8%.

This is such an enticing dividend opportunity because the average yield sat around 2.78% over the last four years, indicating that CVS has fell in value and may present a nice entry opportunity. Even though the price has fallen and the yield is now elevated, I believe that the dividend still remains safe. For reference, the current dividend payout ratio sits at approximately 32%. While this is a bit above the sector median of only 26%, the current payout ratio still sits at a reasonable level and presents no threat to the dividend.

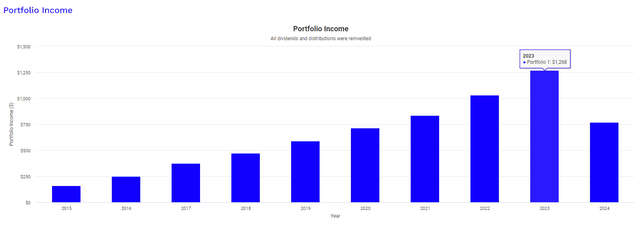

Portfolio Visualizer

Now even though the growth of the dividend has a period of time where it didn’t move, CVS can still be seen as a dividend compounder over time when dividends are reinvested. In this example, let’s assume an original investment of $10,000 with a monthly amount of $250 invested, as well as reinvesting the dividends every quarter.

Referencing the Portfolio Visualizer chart above, the dividend income received in 2015 would only total $162. However, after some time and consistency, your total dividend income received would now be $1,268 in 2023, an increase of almost 8x from your original total in year 1. Additionally, your original position of $10,000 would now be valued at over $40,000. This is the kind of dividend growth potential that makes CVS an attractive stock for people who want to compound their dividend income over time. The dividends received from CVS are also classified as ‘qualified dividends’, making them more attractive from a tax perspective.

Valuation

Now that the price has come down significantly, this may present an attractive entry opportunity. For reference, the average Wall St. price target for CVS sits at $71.37 per share. This represents a potential upside of 28.5% from the current price level. The highest price target that’s listed is at $101 per share but I tend to align more closely with the average price target. CVS currently trades at a price to earnings ratio of 9.73x, which is severely under the sector median price to earnings ratio of 17.44x. Additionally, the price to book ratio remains at 0.94x even though CVS has traded at an average price to book ratio of 1.43x over the last five year period.

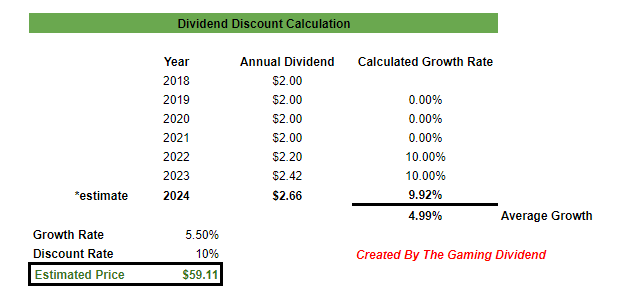

In order to have another source to reference, I decided that a dividend discount calculation may serve appropriate here to get an estimate fair value. Even though the dividend has a period of time that it was not increased, we can still use this method to determine a price target. Compiling the annual dividend payouts dating back to 2018 shows us that the dividend has increased at a CAGR (compound annual growth rate) of roughly 5% since then. The latest increases were about 10% and I used this as a reference point to come up with an estimated annual payout of $2.66 per share for 2024.

Author Created

Additionally, earnings are expected to grow at an average rate of 6.7% over the next decade but I wanted to take a conservative estimate of 5.5% when considering the current circumstances around the slashed guidance in combination with unfavorable market conditions, such as higher interest rates that are effecting pricing. As a result of this, I determine a fair estimated price of $59.11 per share. This represents a modest potential upside of 6.4% from the current price level. However, EBITDA growth has averaged nearly 8% over the last five years so I want to emphasize that this is a conservative estimate.

Even though the estimate is conservative, you have the potential to lock in double digit returns when we take the current high dividend yield of 4.8% into account. We also have to consider how future interest rate cuts may make the growth prospects more attractive. While we let some time pass to see how the market plays out, there’s still a ton of value in just collecting the dividend and waiting it out for now since liquidity remains fine with $9.8B in cash and cash equivalents.

Takeaway

CVS Health Corp has seen its share price fall due to slashed guidance and missed earnings but this isn’t the end of the world. The problems that CVS are facing also weigh down on many of its health care adjacent peers at the moment. The issues of increased costs, higher interest rates effecting margins, and lower volumes in certain sectors are all a result of external forces and not due to any sort of fundamental failure of CVS’s business model. The current valuation suggests a modest upside but this is complemented by a higher dividend yield than average. I believe that the increases in revenue, despite unfavorable conditions, shows us that CVS will likely recover once the tide turns and conditions improve. However, I want to wait on the sidelines for an additional quarter or two before initiating a position just so that there’s a greater length of data to assess how efficiently they manage their cash and which direction the segments are trending in.

Read the full article here