")

This article was coproduced with Chuck Walston.

Soaring net charge-off rates, along with higher credit provisioning costs and a double-digit decline in EPS, sent shares of Discover Financial Services (NYSE:DFS) plummeting to lows not seen since the COVID crisis routed the stock.

These woes struck the credit card company despite a resilient labor market and strong consumer spending. Some pundits contend that the end of student loan forbearance is affecting credit results, creating another headwind for credit card issuers.

On the positive side, Discover’s net revenue has increased, driven by higher net interest income. The company also reported strong loan growth. Add to that potential growth related to international expansion, and you can pardon bulls that might see the current headwinds as providing an opportunity to buy the stock at a more than reasonable valuation.

Sizing Up Discover

Discover ranks as the fourth largest credit card network in the U.S, behind American Express (AXP), Mastercard (MA), and Visa (V). However, unlike the latter two companies, Discover is also a bank. At the end of 2021, consumer deposits represented 68% of Discover’s total funding.

The firm’s Digital Banking segment generated about 99% of Discover’s revenue and net profit in 2022. Operating strictly as an online bank, and lacking brick-and-mortar branches, Discover benefits from lower overhead costs.

Within Digital Banking, credit cards are the largest product category, with interest earned on revolving credit card balances comprising approximately 83% of total interest income.

Operating as a closed-loop network, Discover’s credit card business issues cards directly to consumers that are accepted within its network. Discover only generates around 20% of revenue from noninterest income.

DFS generates over 80% of revenue via net interest income. Once again, the bulk of that stems from interest on credit card balances. Credit cards constitute a bit over 83% of Discover’s revenue with personal loans driving 7% of revenue and student loans providing 6%.

The company focuses on younger customers with minimal credit histories. This results in card holders that are likely to maintain credit balances from month-to-month. While this means Discover often records higher charge off rates, it also spurs increased revenue generated by interest.

The current macroeconomic environment presents a bit of a double edged sword for the company. Rising interest rates lead to surging profits for Discover as consumers grappling with inflation tend to turn to credit cards for purchases. At the same time, increased borrowing costs drive delinquency and charge off rates higher.

Why The Share Price Plunged

Results for Q3, reported in the middle of last month, provided some positives. Revenue of $4 billion was up 16.4%, beating analysts’ estimates by $80 million. Total loans also surged by 17% over last year.

However, diluted EPS landed at $2.59, a 27% year-over-year decline and well below analysts’ consensus of $3.17. This was largely related to higher-than-anticipated loan losses in the third quarter.

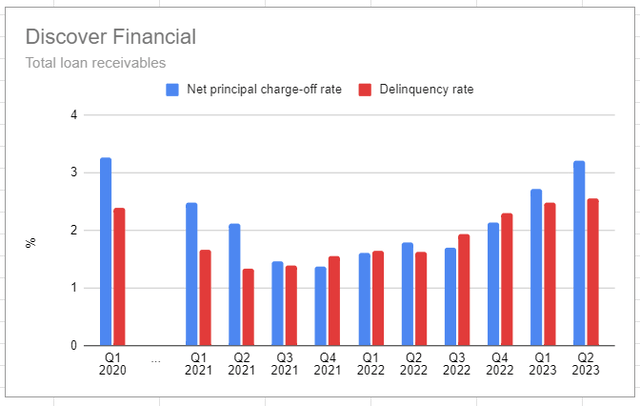

Reporting a net charge-off rate of 3.52%, the company recorded the fourth consecutive quarterly increase in that metric.

Discover’s net charge-off rate is running well above the number reported by commercial banks in the second quarter. It also compares unfavorably to the 2% charge-off rate reported by American Express. However, investors should be aware that AXP has a customer base with higher credit scores than that of DFS.

Seeking Alpha

Management now guides for a full year average net charge-off rate in a range of 3.4% to 3.6% with net charge-offs expected to peak in mid-to late 2024.

Discover’s provision for credit losses of $773 million was up from $549 million in the second quarter and $185 million year over year.

These less than stellar results followed the August resignation of CEO Roger Hochschild. Hochschild’s ouster is likely tied to the company’s discovery in July that it had been overcharging some merchants on swipe fees since the middle of 2017. This prompted an internal investigation into the matter and suspension of Discover’s share repurchase program. It also marked the beginning of the stock’s fall from a 52-week high of $122.50.

While this matter could mean Discover might be required to pay fines, be subject to regulatory actions, and/or higher ongoing compliance costs, the potential affected revenue amounts to less than 1% of Discover’s interchange revenue and less than 0.2% of total revenue.

Discover received a proposed consent order from the Federal Deposit Insurance Corporation advising that additional regulatory actions could occur, and management expects to pay out $365 million to the affected merchants.

Why The Current Pain Could Mean Long Term Gain

Lost in the negatives noted in Q3 earnings are a plethora of positives. First, investors should note that credit loss rates are normalizing following the abnormally low levels of the past two years.

Meanwhile, total loans increased from $102 billion in the comparable quarter to $120.4 billion in Q3. This follows 19% average loan growth in 2022, and management now guides for average loan growth in 2023 in the mid-teens.

Discover also has a history of outperforming competitors. The firm’s efficiency ratios are routinely below 40%, a figure that is markedly better than most banks. Furthermore, Discover has consistently generated returns on equity that are among the highest of its peers.

For example, take American Express, the rival with a business model that most closely mirrors that of Discover. Both run a closed loop network (Visa and Mastercard run networks but are not issuers or lenders.)

Discover has been far more consistent, outperforming in bear and bull markets. The total ten-year return for DFS is roughly 104% versus under 83% for Capital One.

The average net profit margin for COF over the last three years is 21.86%. For Discover, that metric is 26.70%.

Discover’s ROA of 2.54% and ROIC of 2.60%, outpace the sector’s 1.08% ROA and 1.35% ROIC. And Discover’s ROE of 24.59% places it well into the top 25% in its industry.

As previously noted, the firm suspended its share repurchase program pending the outcome of an internal investigation centered on overcharging merchants for swipe fees. I would characterize this move as a healthy dose of caution on the part of management. Nonetheless, that move waylaid the company’s plan, announced during Q1, to repurchase $2.7 billion in shares this year.

To put that in context, Discover has a current market cap of roughly $21.4 billion. It is also important to note that the company bought back approximately half of its shares over the last decade.

Last but far from least, the firm stands to benefit from increased online spending, as well as international expansion. Currently, Discover’s domestic credit card portfolio accounts for 80% of average earnings.

Dividend, Debt, And Valuation

Discover yields 3.38%. The stock has a payout ratio just above 19% and a 5-year dividend growth rate of 12.39%.

As of September 30, 2023, Discover’s Common Equity Tier 1 capital ratio, under the Basel III transition, was 11.6%. That’s well above the company’s 10.5% target rate. DFS has a BBB- credit rating, which is the lowest level of investment grade credit.

Discover currently trades for $83.38 per share. The 12-month average price target of the 16 analysts covering the stock is $105.82. The Price target of the 7 analysts that rated the stock following the last earnings call is $98.43.

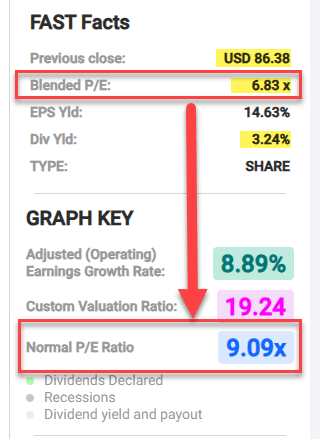

Discover’s forward P/E is 6.78x, well below the 5-year average for that stock’s metric of 11.83x.

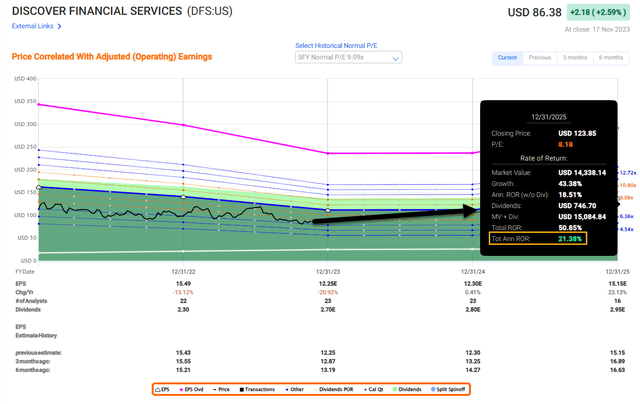

FAST Graphs

Is DFS A Buy, Sell, Or Hold?

The lukewarm Q3 results, partnered with the investigation related to swipe fees, battered Discover’s share price. Add to that management reporting higher stress from consumers with FICO scores on the lower end of the credit spectrum. Plus, concerns related to the cyclical nature of Discover’s business feed the bear argument against the stock.

However, in this period of higher interest rates, Discover will benefit from an increase in higher net interest margins. The company also has a solid history of outperforming rivals during downturns.

Those focused on the stock’s lukewarm performance last quarter are ignoring the firm’s solid history of growth. For example, Discover closed 2022 by reporting $3.8 billion in net interest income, up 41% year over year and a net interest of 11.3%, up 46 basis points year over year.

Trading near 52-week lows, I view Discover’s current valuation as a prime opportunity to invest in a top-notch company. Consequently, I rate Discover as a BUY.

My rating comes with the caveat that DFS has a higher level of uncertainty at this juncture; however, I contend those with a long-term horizon are likely to be richly rewarded by an investment in the company.

FAST Graphs

Note: Brad Thomas is a Wall Street writer, which means he’s not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: Written and distributed only to assist in research while providing a forum for second-level thinking.

Read the full article here