")

Introduction

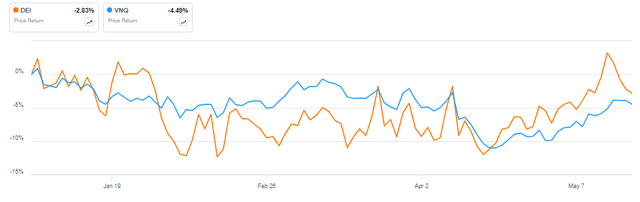

Douglas Emmett, Inc. (NYSE:DEI) has marginally outperformed the Vanguard Real Estate Index Fund ETF Shares (VNQ) so far in 2024, with the company’s shares down in the low-single digits.

DEI vs VNQ in 2024 (Seeking Alpha)

Looking ahead, I expect the REIT to track the sector average, with excellent performance in the company’s residential portfolio not enough to offset office market headwinds. Furthermore, the majority of the company’s interest rate swaps expire over the next two years, straining cash generation for shareholders.

Company Overview

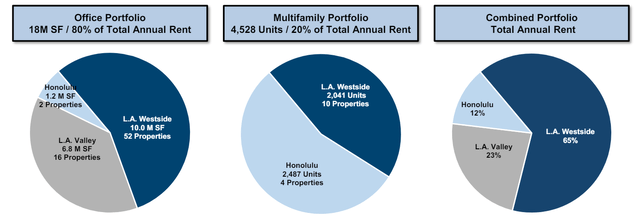

You can access all company results here. Douglas Emmett is an office REIT with sizable multifamily exposure – offices account for 80% of annual rent, with the remaining 20% coming from multifamily properties.

Portfolio Overview (Douglas Emmett Q1 2024 Investor Presentation)

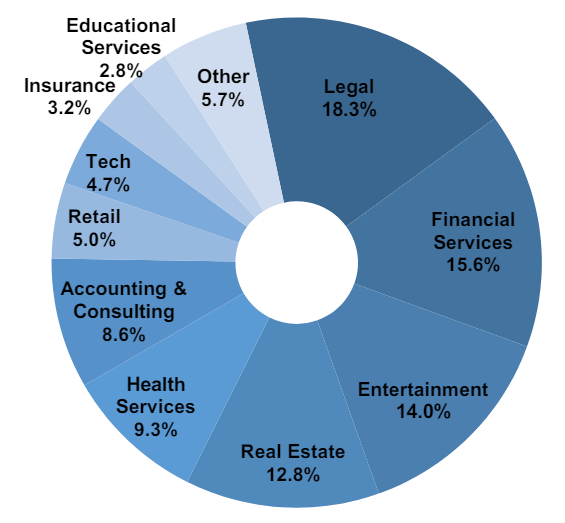

From a geographic perspective, 88% of annual rent comes from California, with the remaining 12% due from properties located in Hawaii. The tenant base is well diversified, with Legal (18.3% of annual rent), Financial Services (15.6%), and Entertainment (14%) as the largest industry exposures.

Tenant industry mix (Douglas Emmett Q1 2024 Investor Presentation)

Operational Overview

Douglas Emmett reports leased rate separately for offices and residential properties. For offices, the leased rate was down 2.7% Y/Y to 80.8% in Q1 2024 while the residential leased rate was down 0.4% Y/Y to 98.9%. Clearly, we see further weakening of the company’s office portfolio which was already distressed to begin with.

FFO was $0.45/share in Q1, down 4% Y/Y, driven by lower rental revenues and higher interest expense. Net operating income increased 0.3% Y/Y, with a 0.1% decline in the office portfolio offset by 2.5% growth in the multifamily portfolio.

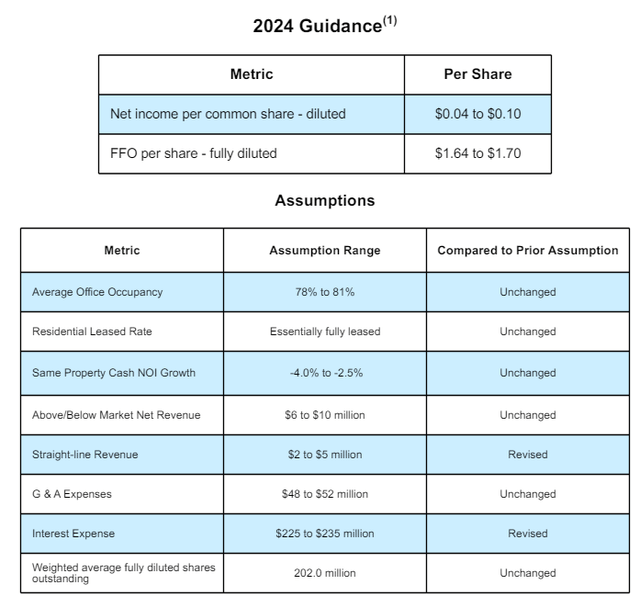

Unchanged 2024 Outlook

The company kept its 2024 outlook intact, with higher-than-anticipated revenues compensated by elevated interest expenses.

2024 Outlook (Douglas Emmett Q1 2024 Earnings Package)

As a result, Douglas Emmett expects to generate an FFO of about $1.67/share in 2024, down 10% Y/Y.

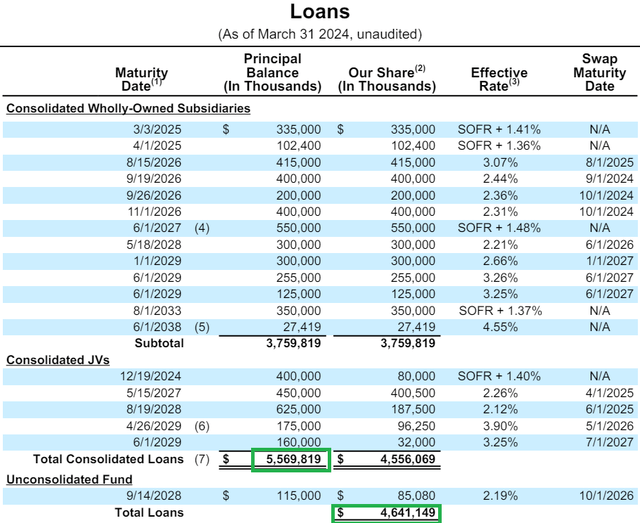

Debt position

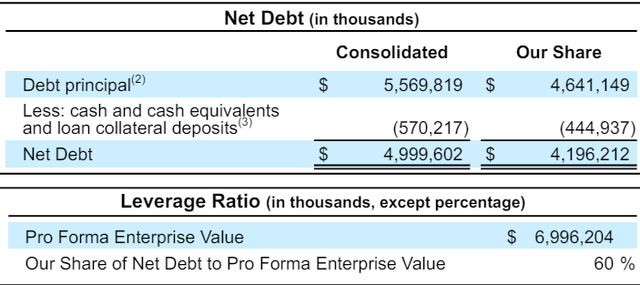

The company ended Q1 2024 with a consolidated net debt of $5 billion, or about $4.2 billion if we take into account the proportionate share the REIT holds in joint ventures.

Overview of debt outstanding (Douglas Emmett Q1 2024 Earnings Package)

If we use the more insightful $4.2 billion net debt figure, we can imply that net debt accounts for 60% of Douglas Emmett’s enterprise value.

Leverage and net debt overview (Douglas Emmett Q1 2024 Earnings Package)

The company’s debt is largely floating rate, but it makes extensive use of interest rate swaps to fix its interest costs. As a result, 68% of the company’s debt is effectively fixed-rate due to the use of interest hedges, with rates fixed at extremely low levels of just 2.66% for the fixed-rate portion of the debt. The downside is that 63% of swaps hedging interest costs expire in 2024-2025. The remaining 32% of the REIT’s debt is a floating rate, with a spread of about 1.4% over the secured overnight financing rate (SOFR), which is currently about 5.3%, resulting in a ~7% interest rate on Douglas Emmett’s floating rate debt.

To summarize, we can say that only about 25% of the company’s total debt is fixed at about 3% for the medium term, with swaps on this portion of the company’s debt expiring in 2026-2027.

| Debt type | Percentage of total debt | Hedges expire |

| Floating rate | 32% | N/A |

| Floating rate with short-term hedges | 43% | 2024-2025 |

| Floating rate with medium-term hedges | 25% | 2026-2027 |

Source: Author calculations

Market-implied cap rate

In Q1 2024, the company produced about $141.1 million in cash net operating income from its property portfolio (this amount excludes NOI owed to minority interests in joint ventures). Hence, we can estimate Douglas Emmett will generate about $565 million cash NOI against its $7 billion enterprise value in 2024, resulting in a market implied cap rate of 8.1%. Despite rent escalators of about 3-5% annually, I expect NOI to grow slower due to oversupply in the office market.

If we assume the fair market cap rate is about 6.8% for the company’s residential portfolio (which in itself is a conservative assumption, but in line with peers such as Independence Realty Trust, Inc. (IRT) and NexPoint Residential Trust, Inc. (NXRT)), we can reason that the market says that the 80% office exposure is currently trading at an 8.5% market cap rate, which in itself isn’t that exciting for an office REIT with lackluster occupancy.

Risks

With net debt accounting for 60% of enterprise value, retaining funds to reduce leverage is a key priority for management. This is evidenced by the meager 51.6% payout in Q1 2024. The company’s cash flows are likely to come under immense strain in the coming years as its interest hedges expire. As such, a delay in Fed rate cuts, currently widely anticipated to start in September, will adversely affect Douglas Emmett.

From an operational standpoint, the situation is very polarized, with a stellar performance in the residential portfolio offset by eroding occupancy in the office portfolio. At some point, one would expect office performance to stabilize, but with an 8.1% market cap rate, such a stabilization may already be priced in.

Conclusion

I like the residential exposure tilt Douglas Emmett offers, although it is only 20% of the company’s annual rent. Furthermore, I reckon that a good portion of vacant office space eventually gets repurposed for other uses, with residential as the first go-to option. As such, the experience the company has in residential may put it ahead of competitors when it comes to such redevelopments.

As things stand, however, the 8.1% market cap rate isn’t attractive enough for me to issue a buy rating on the shares, given the very troubled nature of the office market. As such, I am neutral on the shares.

Thank you for reading.

Read the full article here