")

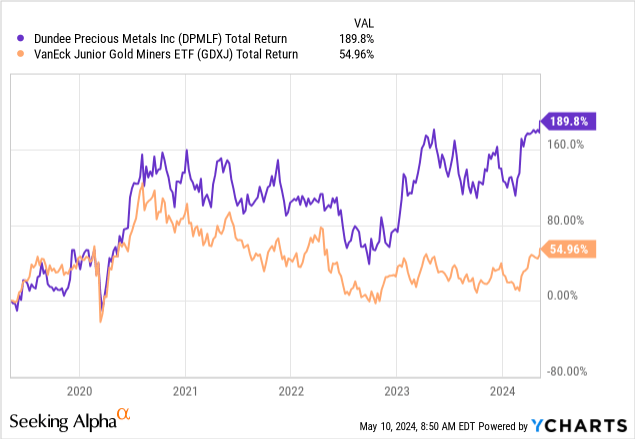

I have covered Dundee Precious Metals (OTCPK:OTCPK:DPMLF, TSX:DPM:CA) in the past in a number of articles, most recently here in January. Dundee is one of my core holdings among gold miners, because of its excellent management, operational outperformance, low costs, recent exploratory success, and growth opportunities. Despite being one of the best performing gold miners over the last five years, it remains highly undervalued. The company has a market capitalization of around $1.5 billion, $600 million in cash and no debt. It is guiding for production of around 245 thousand to 285 thousand ounces of gold in 2024, at all-in sustaining costs (AISC) sub-$1000 per ounce ($790-$830 per ounce). This means it should easily be able to generate in excess of $250 million in free cash flow per year at current gold prices. This would give it a forward FCF yield of around 30%.

Of course, all that glitters is not gold. In particular, I would point out two important reasons why the market is applying a discount compared with peers. The two reasons are interconnected with each other.

The first one is that Dundee will find it challenging to maintain current production rates in the next few years. Its producing assets, i.e. Chelopech and Ada Tepe, located in Bulgaria, are low-cost gold mines, but they are also relatively small in size. This is true in particular for Ada Tepe.

Ada Tepe is a very high-grade, open-pit gold mine. Since first production in 2019, Ada Tepe has performed exceptionally well, producing over 125,000 ounces per year at sub-$750 all-in sustaining costs. However, the deposit is small: its life-of-mine extends only to 2026. Its production is already declining: it is expected to produce between 90,000 and 110,000 ounces in 2024, with AISC between $710 and $830 per ounce. In 2024, it is off to a great start, especially from a cost perspective, having already produced 25,000 ounces in Q1 at $583 AISC.

Chelopech is the company’s flagship asset. It is a very low-cost underground copper-gold mine. In 2024, it is expected to produce between 155,000 and 175,000 ounces at AISC between $650 and $790 per ounce. The low costs are a result of the copper by-products, since the mine is also expected to produce between 29 and 34 million pounds of copper. In Q1 2024, AISC came in quite a bit higher at $849 per ounce. However, grades and recoveries are expected to improve for the balance of the year, and the company has reiterated its guidance.

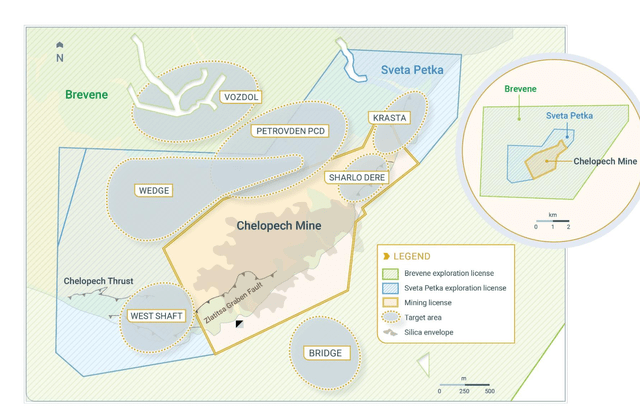

At Chelopech, the company has recently had great success in offsetting mine depletion by converting mineral resources into mineral reserves through in-mine and brownfield exploration programs. After the most recent update in 2023, Chelopech is now expected to have a life-of-mine extending to 2032. Of particular interest are the recently identified Sharlo Dere prospects, located within the Chelopech concession, to the north-east of the main underground development. Positive intercepts from drilling in 2023 included 8 m @ 14.15 g/t AuEq, 9.34 g/t Au & 2.87% Cu, 6.2 m @ 7.54 g/t AuEq, 6.70 g/t Au & 0.50% Cu, and 37.5 m @ 7.34 g/t AuEq, 5.69 g/t Au & 0.98% Cu. Sharlo Dere is not yet accounted for in the latest Mineral Reserve estimate for Chelopech, but it will in the next update this year.

Company’s Presentation

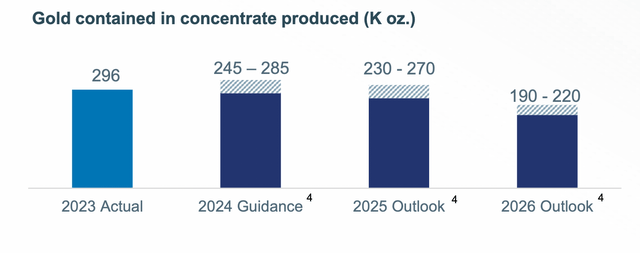

Despite these brownfield exploration efforts, the company’s outlook sees production decline sequentially over the next three years, from 245,000 to 285,000 ounces in 2024, down to 190,000 to 220,000 ounces in 2026. To offset the decline, the company has been looking into M&A opportunities, which leads us to the second reason for its undervaluation.

Company’s Presentation, Annual Meeting of Shareholders

A gold miner with a big cash position looking for acquisitions has historically been a recipe for value destruction. When in December, Dundee announced its proposed acquisition of Osino, the market reacted by selling it down by 10%. This is despite the fact that the acquisition made a lot of sense. Osino’s Twin Hills deposit, located in Namibia, would have provided near-term production, while at the same time offering a long mine life and exploration upside.

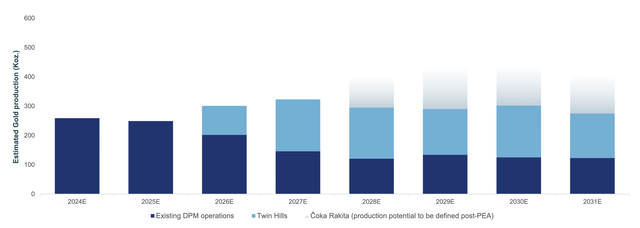

More in detail, Twin Hills would have added around 2.2 million ounces in reserves and 175,000 ounces per year in production, at AISC of $1011 per ounce over a 13-year life-of-mine. The deal would have included optionality and upside potential via the Eureka and Ondundu discoveries, located in the same concession. The new mine would have been located in a stable jurisdiction, with good infrastructure, in a country in which Dundee already had a presence (the company owned the Tsumeb smelter, which it recently sold after the acquisition didn’t go through). The initial CapEx estimate was quite high at $365 million, though it could have been entirely financed from the company’s balance sheet. As shown in the following visualization, the development of Twin Hills would have allowed Dundee to compensate for the declines at its Bulgarian mines, and actually grow production to around 300,000 ounces per year starting in 2026.

Company’s Presentation

Unfortunately, Osino has recently been acquired by Yintai Gold. I am summarizing the terms of the deal to show that actually the acquisition was very sensible, and that Dundee’s management was very disciplined in avoiding a bidding war with Yintai. Yintai’s offer represented almost a 32% premium over Dundee’s agreement, which clearly shows how valuable the original deal would have been if it had gone through.

Why, nonetheless, do I remain bullish on Dundee? First of all, in my experience, sensible and disciplined managements continue to make sensible and disciplined capital allocation decisions. I really don’t see how Dundee’s management would suddenly decide to throw caution to the wind, and splurge its cash pile on a questionable acquisition.

The main risk is, on the other hand, that Dundee does not find a suitable acquisition target, and has to shrink its production over the next few years. This would indeed be unfortunate, since we are, in my opinion, in the early stages of a secular bull market in gold. However, it seems to me that this is still very much a buyer’s market in the junior gold mining sector, and there are quite a few development projects that can be had at a reasonable price despite the recent gold strength.

In any case, even if the right opportunity does not materialize, Dundee still has a number of options from its current exploration portfolio. There are two main directions in which future production growth can be achieved.

First of all, there is Loma Larga. This is an advanced project in the Azuay province of Ecuador, that has encountered many problems during the permitting stage, which I discussed in more detail in previous articles. The asset is very high quality; it also has the size to compensate for the loss of Ada Tepe (it could produce about 200,000 ounces per year during its first five years of operation). The project has very strong government support, but unfortunately it has encountered fierce opposition from the local communities. As a result, drilling activities have stopped, and it is unclear whether Dundee will ever manage to fully unlock this asset. At the moment, the market seems to assign no value to it. I would not be too quick to totally write it off, though. First of all, Ada Tepe also encountered opposition from the local communities, but Dundee proved quite adept at working with them, and finally got the mine fully permitted and developed. Second, it seems that after a long pause, things are starting again to move.

In the first quarter of 2024, the government of Ecuador started the environmental consultation process with the local communities. This is a necessary step to move on to the exploitation phase that has been required by the Constitutional Court of Ecuador. A clear legislation about the form of this process does not yet exist, but an interim procedure has been put in place by the Ministry of Energy and Mines. It will be used for the first time for the Loma Larga project, which proves its strategic importance and the close relationships that Dundee has been able to cultivate within the government. Nonetheless, it is also clear that this will be a long process, and the company has prudently slashed its capital expenditure guidance for Loma Large (from $20 million spent in 2023, to only $10 million in 2024) to focus on higher priority projects. Overall, I see Loma Larga mainly as providing optionality, but it is does not play a major role in my investment decision.

On the other hand, the company’s exploration portfolio in Serbia looks extremely interesting. Besides Timok, which is a relatively small deposit going through the Feasibility Study stage, and currently on-hold, Dundee has made what appears to be a major discovery at Coka Rakita. Following some truly stunning intercepts announced in January 2023 (including RADDMET01 – 40 metres at 63.46 g/t Au), the company completed a Maiden Mineral Estimate in December. More recently, on May 1, it released a positive Preliminary Economic Assessment (PEA).

According to the PEA, Coka Rakita hosts a mineable Mineral Resource of 7.9 million tonnes, with a cut-off grade of 2.5 g/t and average grade of 5.68 g/t. The initial CapEx is expected to be around $381 million, which is similar to what Twin Hills would have required. The timeline for Coka Rakita, however, is more extended. If Twin Hills was expected to go into production by 2026, the same could happen for Coka Rakita not earlier than 2028. The PEA assumes start of construction by mid-2026, followed by commissioning, ramping up and first concentrate production in the first half of 2028. Development would entail construction of an 850,000 tonne per year processing plant and a 5-million tonne Dry Mine Waste Facility. The initial mine life is 10 years, with average life-of-mine gold production of around 129,000 ounces per year (164,000 ounces per year over the first 5 years). While construction costs are relatively high, sustaining costs are very low, averaging only around $8 million per year. As a result, AISC is expected to fall in the first quartile of the global production curve at $715 per ounce. The project has therefore solid economics, with an after-tax NPV at 5% discount rate of $588 million, an after-tax IRR of 33% and payback period of 2.4 years. These metrics are all better than Twin Hills. Twin Hills would have had a slightly lower annual production, but a longer initial life-of-mine, plus higher costs.

The above numbers assume a gold price of $1700 per ounce and a discount rate of 5%. On the one hand, I hope we will never see such low gold prices; on the other, I would consider 10% more appropriate as a discount factor in today’s inflationary environment. The following are my own estimates for the NPV of Coka Rakita based on different gold price assumptions and discount rates.

| Gold price ($/oz) | Discount rate | NPV |

| 1700 | 0.05 | 590,000,000 |

| 2000 | 0.05 | 855,000,000 |

| 2500 | 0.05 | 1,296,000,000 |

| 3000 | 0.05 | 1,738,000,000 |

| 1700 | 0.1 | 357,000,000 |

| 2000 | 0.1 | 545,000,000 |

| 2500 | 0.1 | 858,000,000 |

| 3000 | 0.1 | 1,171,000,000 |

To conclude, Dundee Precious Metals is a well-managed and highly profitable intermediate gold miner. In the medium-term, it faces the challenge of declining production, in particular after the loss of Ada Tepe in 2026. The acquisition of Osino would have been highly accretive and would have allowed to plug the hole in its production profile. Its failure clearly represents a setback. Nonetheless, I would not discard the possibility that Dundee manages to find another attractive acquisition target in the near-term. Additionally, the recent release of the PEA for Coka Rakita has confirmed initial hopes that this is a very high-quality asset. Its NPV at current spot prices is roughly equivalent to the company’s entire enterprise value, making Dundee significantly undervalued. Loma Larga provides further optionality, together with Tierras Coloradas and Timok. Overall, this is a team of exceptional explorers and mine builders, that has recently achieved some of the best intercepts in the sector. Unfortunately, the company is also, I believe, misunderstood and under-followed, but this is also what makes it an attractive value proposition.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here