")

I came across Easterly Government Properties, Inc. (NYSE:DEA) while screening for high-yielding investments.

DEA has many positive investment attributes such as stable, long-term tenants from the U.S. government and attractive valuations at just 10.0x Fwd P/FFO.

However, my main concern is that in the past few years, costs have been rising faster than revenues at DEA, leading to a shortfall in the REIT’s cash available for distribution compared to its dividend rate. This situation makes DEA’s dividend vulnerable to a cut.

Company Overview

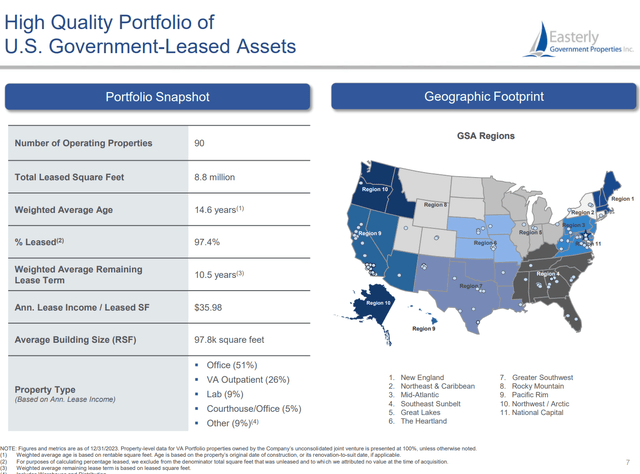

Easterly Government Properties is a real estate investment trust (“REIT”) focused on acquiring, developing, and managing properties that are leased to U.S. government agencies (Figure 1).

Figure 1 – DEA overview (DEA investor presentation)

The company has 90 operating properties with 8.8 million sq. ft. of leased real estate throughout the United States. DEA’s properties are primarily leased to government agencies like the FBI, DOD, and the Department of Veterans Affairs.

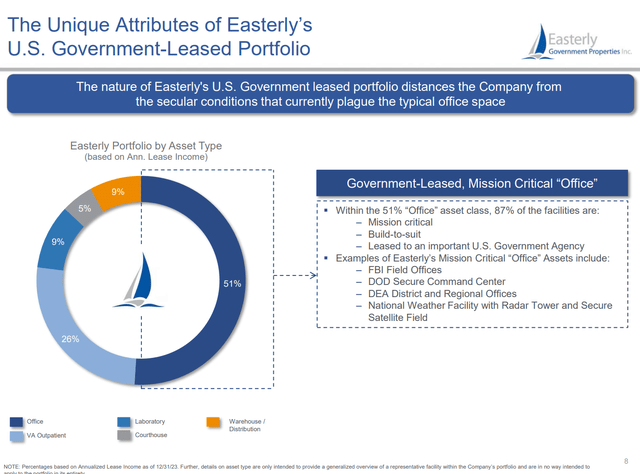

By asset class, 51% of DEA’s properties are office space, 26% are VA outpatient clinics, 9% are laboratories, 5% are courthouses, and 9% are warehouses and distribution centers (Figure 2).

Figure 2 – DEA portfolio overview (DEA investor presentation)

Why Lease To The Government?

Leasing to the U.S. government has many advantages. First, lease payments are backed by the full faith of the U.S. government. Although there have been recent concerns regarding the federal deficit and rising debt levels leading to a debt downgrade by the rating agencies, there is no doubt that the U.S. government has unlimited capacity to pay obligations in U.S. dollars.

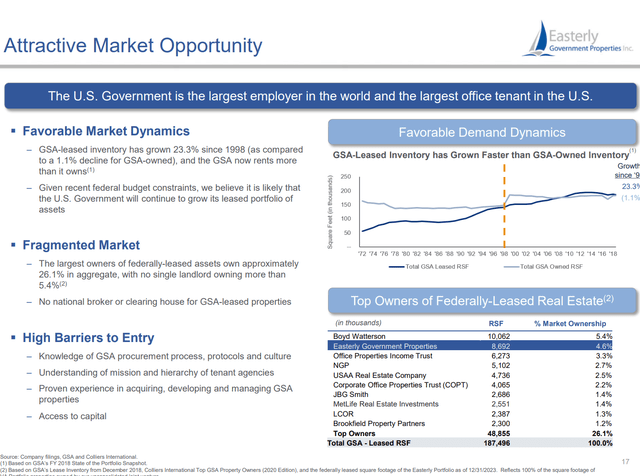

Second, the U.S. government is the largest employer in the world and is the largest office tenant in the U.S. with high barriers to entry (Figure 3). Due to budgetary constraints, the U.S. government has been favouring renting office rather than owning them outright, leading to long-term growth tailwinds for DEA’s business.

Figure 3 – Government leased real estate has long-term tailwinds (DEA investor presentation)

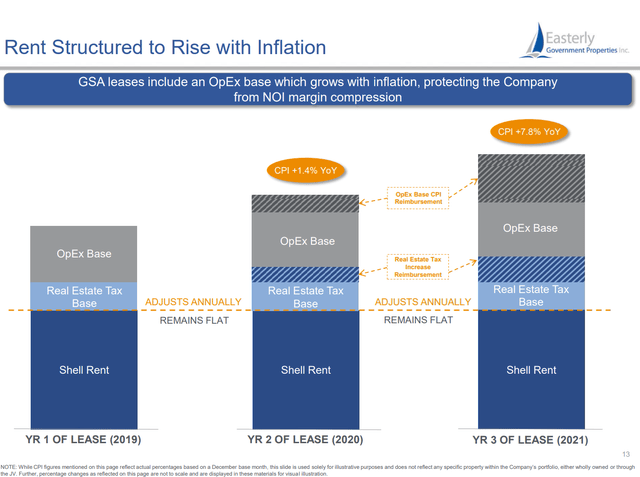

Furthermore, DEA typically structures its lease agreements with adjustments for inflation (Figure 4). This protects the company from NOI margin compression during inflationary periods.

Figure 4 – Typical DEA rent structure (DEA investor presentation)

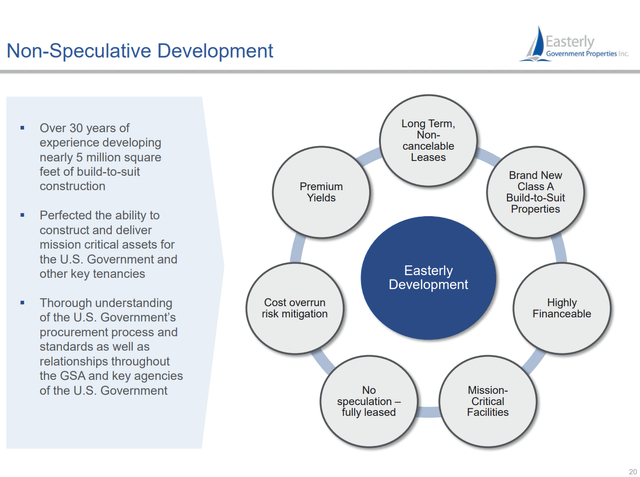

However, there are also important downsides to consider with respect to DEA’s business. Since DEA often acquires or develops properties to suit specific government needs (“build-to-suit”), these properties may not be suitable for other businesses and thus Easterly Development may have a bargaining disadvantage when it comes to lease renewals (Figure 5).

Figure 5 – DEA build-to-suit government needs (DEA investor presentation)

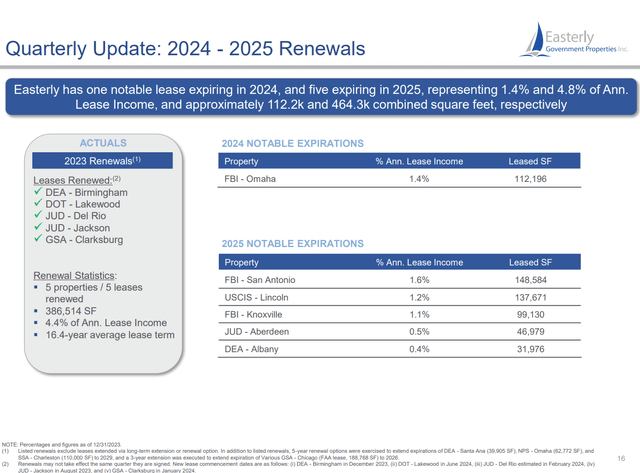

Fortunately, the U.S. government appears to negotiate in good faith and to date, DEA has not had any major issues renewing its properties at prevailing market rates (Figure 6).

Figure 6 – DEA has been able to renew its leases with no issues (DEA investor presentation)

DEA Has Proven Ability To Grow

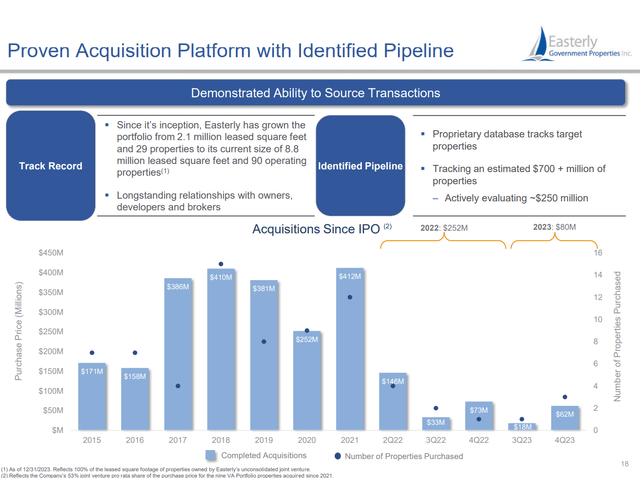

Since coming public in 2015, DEA has grown via a two-pronged approach of acquiring existing real estate or developing buildings to suit specific agency needs as mentioned above. To date, DEA has acquired $3.3 billion in government-leased real estate (Figure 7).

Figure 7 – DEA has grown through acquisitions (DEA investor presentation)

DEA’s proven ability to acquire or build has allowed the company to scale up from 29 properties and 2.1 million leased square feet at IPO to 90 properties and 8.8 million sq. ft. in less than a decade.

Financial Overview

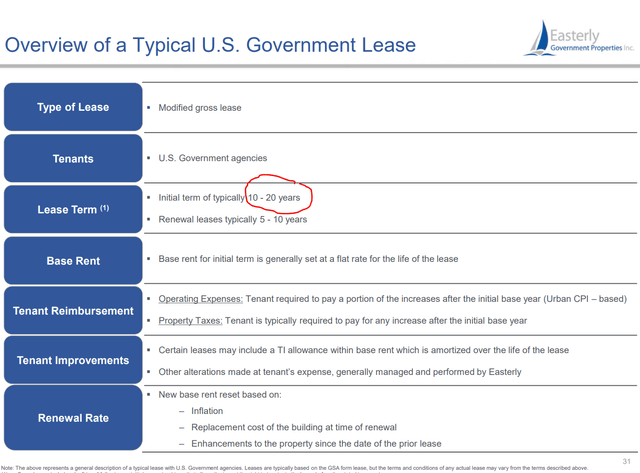

While other office REITs have suffered in the face of changing worker trends towards working from home (“WFH”), DEA’s business appears relatively unscathed due to the long-term nature of its government leases and the government’s creditworthiness (Figure 8).

Figure 8 – Typical government lease is for 10-20 years (DEA investor presentation)

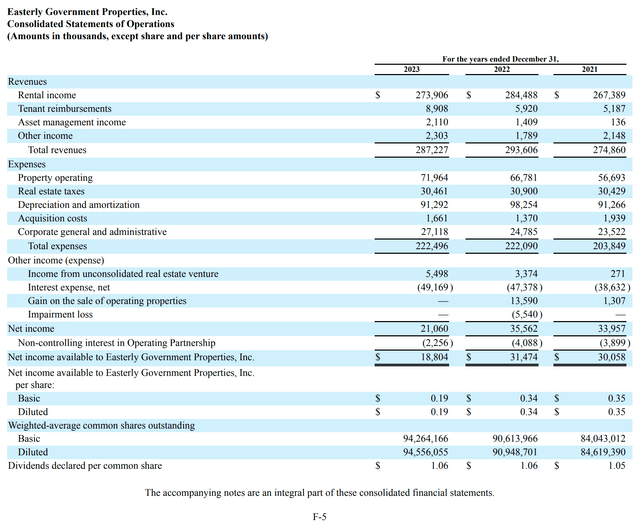

For example, revenues for DEA were $287.2 million in 2023, down a nominal 2% YoY due to some disposals, but still 4% higher than 2021 levels (Figure 9).

Figure 9 – DEA financial overview (DEA 10-K report)

However, significantly higher operating and interest expenses have led to a deterioration in DEA’s net income and cash flows in 2023. Net income for 2023 was only $18.8 million, down 40% YoY due to $6.4 million lower in revenues, and the absence of a significant one-time gain.

Compared to 2021, 2023 operating expenses were $18.7 million higher, more than offsetting the $12.3 million increase in revenues. Interest expenses were also $10.6 million higher, leading to net income being $11.3 million lower than 2021.

Valuation Looks Attractive

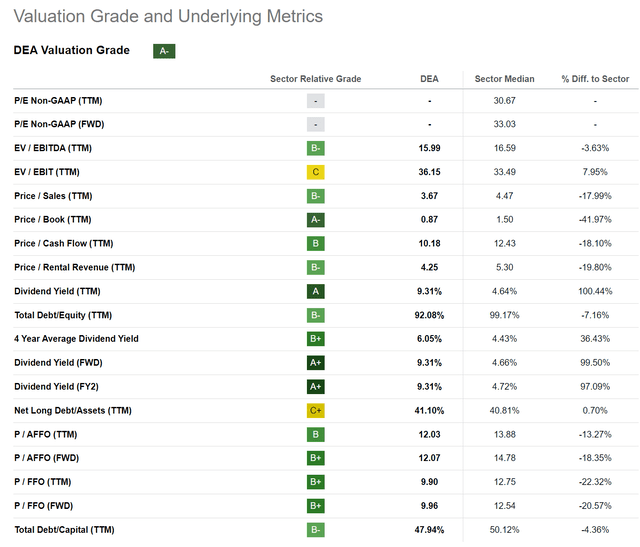

Valuation-wise, DEA does look attractive, as it is trading at 10.0x Fwd P/FFO compared to real estate peers at 12.5x (Figure 10).

Figure 10 – DEA valuation looks attractive (Seeking Alpha)

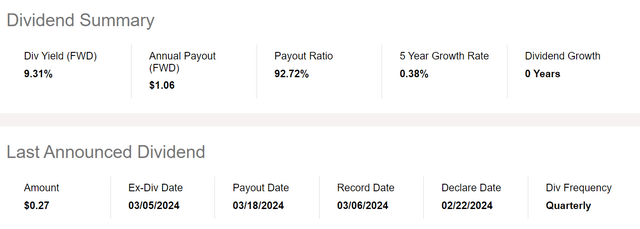

Furthermore, DEA is currently paying a $1.06/share dividend, which works out to a 9.3% dividend yield, almost double that of peers.

But Is The Distribution Sustainable?

To be honest, the item that first caught my attention was Easterly Government’s dividend yield (Figure 11).

Figure 11 – DEA pays a 9.3% dividend (Seeking Alpha)

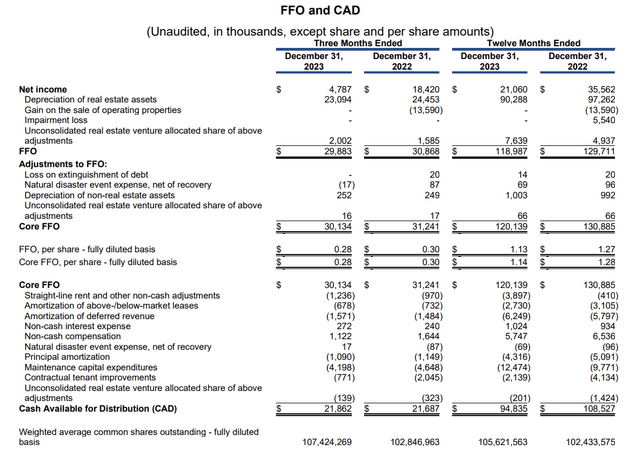

However, digging into the details, I have concerns as to whether DEA’s dividend rate is sustainable. For example, if we look at the company’s funds from operations (“FFO”), we can see that DEA generated $120.1 million in Core FFO in 2023, or $1.14/share (Figure 12).

Figure 12 – DEA FFO vs. CAD (DEA Q4 earnings press release)

However, FFO excludes important cash outlays like maintenance capex and tenant improvements. Looking at Cash Available For Distribution (“CAD”), we can see DEA only generated $94.8 million in CAD or $0.897/share. This is significantly less than the company’s dividend of $1.06/share, so DEA is paying more than it generates in cash. For comparison, in 2022, DEA generated $108.5 million in CAD or $1.06/share, which was just able to cover its 2022 dividend of $1.06.

In the short run, companies can usually afford to pay more in dividends than it generates in cash, as they can borrow from the bond markets or bank loans to make up the difference. However, if the overpayment is persistent and widens, then investors need to be careful, as that could portend to a dividend cut.

Conclusion

Easterly Government is a REIT focused on acquiring and developing real estate that is leased to the U.S. government. The REIT has seen strong asset growth since its IPO in 2015, more than quadrupling leased square footage to 8.8 million sq. ft.

Relative to peers, DEA appears attractively valued, trading at 10.0x Fwd P/FFO with a 9.3% dividend yield. However, I am concerned that this dividend may not be sustainable, as DEA has been paying more than it generates in distributable cash.

While I like DEA’s high-quality tenants and attractive valuation, I am concerned the REIT may be too aggressive in its distribution policies, so I rate it a hold.

Read the full article here