")

Enphase Energy (NASDAQ:ENPH) is a leading solar technology company specializing in end-to-end solar power and storage solutions for rooftop solar systems for residential homeowners (with an increasing commercial base). Its revenue base is mainly exposed to the US, with its leading microinverter technology and increasing presence in energy storage systems. Accordingly, the US market generated almost 65% in revenue on a trailing twelve-month basis. Enphase’s European market is a critical growth driver underpinning its international revenue exposure.

Over the past year, Enphase has been battered by a “perfect storm” of challenges that called into question its relatively expensive valuation. Accordingly, ENPH has declined more than 60% over the past year, notwithstanding its recent recovery as it bottomed out in November 2023. I presented in my previous update to Enphase investors in early October, highlighting why it could be “on the verge of a huge bottom.” However, while that prognosis came a month too early, ENPH bottomed out resoundingly in November, as the recovery continued this month.

As a result, ENPH has recovered its pivotal $110 support level, undergirding its long-term uptrend since early 2021. However, ENPH buyers must continue demonstrating conviction of its recovery before more momentum-driven investors are attracted to return, anticipating further gains.

Therefore, the critical question facing investors is, what has changed dramatically over the past two months that led dip buyers to return with such confidence in helping ENPH to bottom out? Observant investors should recall that Enphase posted its most recent third-quarter or FQ3 earnings release in late October, which led to a sharp selloff toward the $70 level before bottoming out the following month.

It also led to a slew of analysts’ downgrades as Wall Street became increasingly concerned about Enphase’s recovery momentum. Three critical challenges spurred investor/analyst pessimism in October/November. These include high-interest rates, regulatory challenges in the US and Europe regarding net metering, and inventory normalization issues that took longer than anticipated.

The good news is that at least one critical headwind seems to have been resolved: the Fed rate hikes. With the Fed highlighting three rate cuts in 2024, it could untether one of the growth impediments that have afflicted Enphase’s installers, as downstream customers hobbled with higher financing charges. Although the Fed has not initiated the rate cuts, the market is a forward-discounting mechanism. Therefore, I believe the market has likely attempted to price them in early, suggesting the worst in ENPH’s waterfall decline is likely over. As a result, the market’s focus will likely return to Enphase’s underlying business, which has remained highly resilient, notwithstanding the “perfect storm” of challenges.

Investors will likely expect more constructive commentary from management regarding the normalization of its inventory management. Enphase highlighted it expected these issues to persist until Q2 of 2024, based on its visibility in late October. Given ENPH’s recent recovery, the market will likely expect Enphase to clarify improved inventory level dynamics. As a result, I assessed a faster normalization phase could spur a further re-rating tailwind for ENPH, leading to a more robust revenue growth recovery in 2024 than what analysts had penciled in.

Presently, Wall Street anticipates a nearly 16% decline in YoY revenue growth for 2024, reflecting management’s caution about persistent downstream headwinds through the first half of 2024. In addition, Enphase’s adjusted EPS is also expected to fall almost 5% YoY in 2024. Consequently, it could mark two consecutive years of negative adjusted EPS growth for Enphase, possibly explaining why ENPH was hammered over the past year. However, I believe the market has attempted to price in these challenges at ENPH’s October/November lows.

Moreover, with the Fed’s rate hikes out of the way, I’m confident it should help provide more clarity to Enphase and the solar supply chain. Therefore, I expect the company to assure investors with a more confident outlook at its Q4 earnings call. With ENPH still priced at a premium (forward EBITDA multiple of 29x), I believe the market isn’t expecting anything less than an improved recovery cadence.

Enphase bulls could point to the company’s robust profitability metrics (rated “A” by Seeking Alpha Quant), notwithstanding the challenges. In other words, the company has demonstrated its remarkable ability to maintain profitable growth through the cyclical headwinds. Moreover, Enphase operates in a secular growth industry, as the energy transition momentum should regain traction with a more dovish Fed from here.

Therefore, I expect Enphase to remain a key beneficiary of the industry’s recovery, given its market leadership. In addition, the company still has substantial firepower to deploy its $1B stock repurchase program, as it utilized about $110M of its authorization in Q3. Management stressed that it viewed ENPH favorably at the levels at which it bought back its shares in Q3, with an average cost of about $130. Therefore, I wouldn’t be surprised if management highlighted a more aggressive repurchase cadence in Q4, returning more value to Enphase holders.

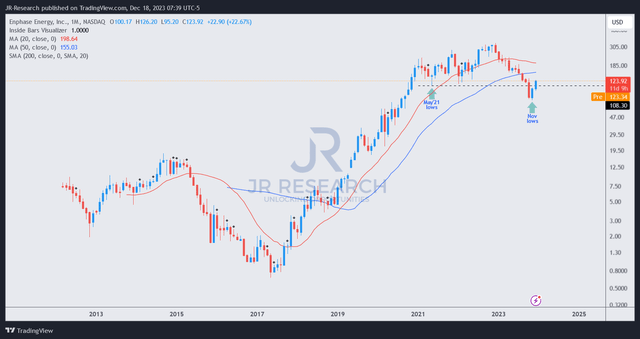

ENPH price chart (monthly) (TradingView)

Notwithstanding its sharp decline since topping out in December 2022, ENPH remains in a long-term uptrend. Therefore, from the price action perspective, it merely represented a steep pullback against a long-term uptrend bias, with dip-buyers returning aggressively in November 2023.

As a result, ENPH has recovered the pivotal $110 level, although it needs to hold it through the end of December to validate the bear trap or false downside breakdown (see price action glossary).

However, as explained earlier, I am convinced that the worst in ENPH is likely over. ENPH’s price action has remained constructive, allowing investors to add exposure to ENPH’s early recovery as we move past the Fed’s rate hike headwinds. Long-term investors looking to benefit from the anticipated cyclical recovery should hop aboard the “solar coaster” early.

Rating: Upgraded to Strong Buy.

Important note: Investors are reminded to do their due diligence and not rely on the information provided as financial advice. Please always apply independent thinking and note that the rating is not intended to time a specific entry/exit at the point of writing unless otherwise specified.

We Want To Hear From You

Have constructive commentary to improve our thesis? Spotted a critical gap in our view? Saw something important that we didn’t? Agree or disagree? Comment below with the aim of helping everyone in the community to learn better!

Read the full article here