")

Investment Thesis

Euroseas’ (NASDAQ:ESEA) stock price is up 94 percent in the last year (as of March 18, 2024) and it recently posted Q4 2023 results. Revenues were $49.1 million, down 3 percent from Q3 but up 14 percent from Q4 2022. EPS (diluted) was $3.56, down 23 percent from the preceding quarter – but up 24 percent from Q4 2022. The company reported an average TCE of $29,266/day.

It declared a $0.60 dividend, which translates to an annualized yield of 7.1 percent, based on its Feb 21 closing price of $33.59. ESEA has paid out dividends in seven of the last eight quarters, with a payout ratio in the 11-17 percent range. The Q4 dividend was 20 percent higher than the previous quarter.

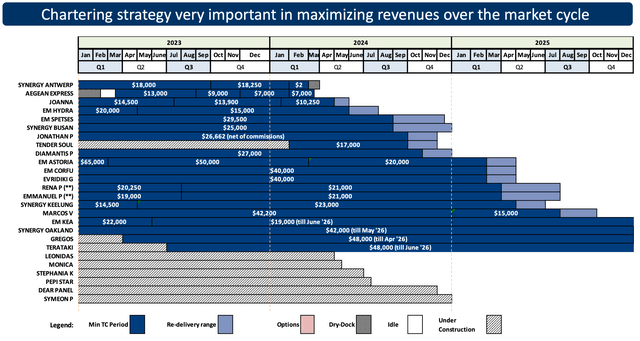

The company has embarked on a newbuild program, aiming to increase its TEU capacity by nearly 30 percent during 2024. It will do this by acquiring seven newbuilds for its fleet this year, one of which was the 2,800 TEU Tender Soul. It was delivered and went straight into an 8-10 month TC at $17,000/d. The next in line for delivery—the equal-sized Leonidas Z—is already contracted through March 2026 at a day rate of $20,000.

However, to finance these newbuilds, ESEA expects to take on an additional $165 million in debt—more than double its current debt.

When compared to its peers along fundamental indicators, ESEA performs well.

Company Overview

Euroseas, Ltd., is a NASDAQ-listed container shipper registered in the Republic of the Marshall Islands, with operational offices in Greece. Incorporated in 2005, it owns 20 small containerships (thirteen feeders and seven intermediate, with an average TEU capacity of about 3,000). Its most recent fleet addition is the MV Tender Soul. ESEA took delivery of this vessel on February 6, 2024, and it immediately commenced an 8-10 month charter at $17,000/day (see earnings report, p. 1). Six more feeder ships are on order; delivery is expected in 2024.

The Pittas family is ESEA’s major shareholder. Through various investment vehicles, it wholly or partially controls at least 58 percent of the company’s shares (see its 2022 20-F filing, pp. 76-77). Institutional investors are notably absent from the list of major shareholders. Given its significant ownership stake in the company, investing in ESEA is also a bet on the Pittas family’s motivations and incentives for caution.

Earnings Visibility

As of Feb 21, ESEA reported 71 percent charter coverage for 2024:

Contract backlog as of Feb 21, 2024 (p. 7, Q4 2023 presentation)

Additionally, ESEA announced on Feb 28 that its newbuild, the 2,800 TEU Leonidas Z, will commence a 2-year charter at $20,000/day upon delivery.

The company was previously able to fix a few of its ships on more extended contracts at desirable rates. Take the Gregos, a 2,800 TEU feeder sailing at $48,000/day until 2026. The day rate development of a few of its other vessels illustrates market trends:

- The 1,732 TEU Joanna is down to $10,250/d, compared to $14,500/d in early 2023.

- The 2,788 TEU EM Astoria sailed at $65,000/d in early 2023, $50,000/d through 2023, and since March 2024, just $20,000/d.

- The 2,800 TEU Tender Soul, a brand-new vessel delivered in Feb 2024, was contracted at $17,000/d.

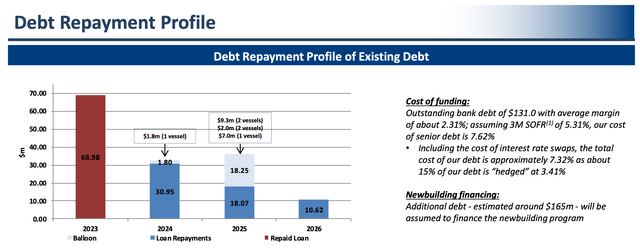

Debt Repayment Profile

p. 19 in ESEA’s latest presentation provides an overview:

Debt repayment profile (Q4 2023 presentation)

After repaying nearly $69 million in 2023, ESEA is due to repay $33 million this year. The important part to note is the “newbuilding financing” paragraph. ESEA carries $131 million in debt today but assumes it will draw another $165 million – a 125 percent increase – as part of its newbuilding program.

Fifteen percent of its debt is hedged – at 3.41 percent – leaving it exposed to interest rate fluctuations.

Dividend Policy and Share Repurchase Program

As mentioned above, ESEA has paid dividends in seven of the last eight quarters:

DPS and payout ratio, Q1 22 – Q4 23 (Seeking Alpha)

Before this, the last time it paid dividends was in 2013.

The company initiated a $20 million share repurchase program in 2022. By February 21, 2024, it had expensed $8.2 million of those funds. Said CEO Aristides Pittas, “We will continue to ensure that we properly reward our shareholders via dividends and share repurchases (..).”

(A note on the broken dividend streak: Seeking Alpha and Euroseas own “Dividend History” page shows no dividend for Q2 2023. However, the Q2 2023 press release on Euroseas’ website refers to a dividend of $0.50 for the second quarter. I have chosen to remain conservative and present the seven clear dividends.)

Fleet Review

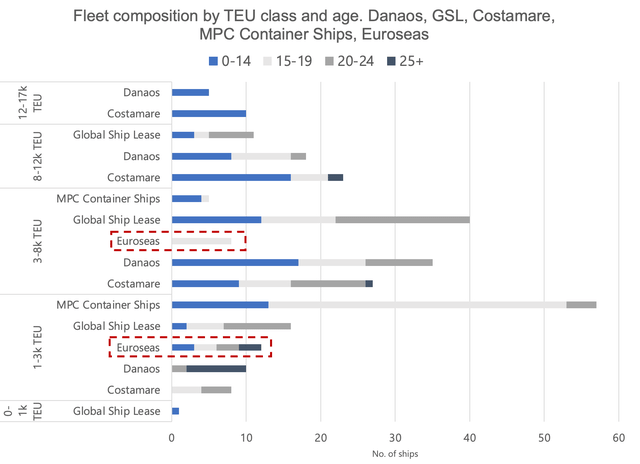

ESEA will be compared to its closest listed peers. Their fleets are a mix of the smaller and larger segments, but all have a presence in the feeder and intermediate segments.

- Danaos Corp. (DAC), which controls 68 container ships (and seven bulkers)

- Costamare, Inc. (CMRE), which also controls 68 container ships (but 21 bulkers)

- Global Ship Lease (GSL), which also(!) controls 68 container ships (but no bulkers)

- MPC Container Ships ASA (OTCPK:MPZZF), which controls 62 container ships.

Regarding ESEA’s fleet composition, it controls vessels in all age groups and, as the illustration below shows, focuses on the smaller segments.

Drawing a bell curve around the horizontal bars is almost possible, but MPZZF’s practically singular focus will break the curve on the below 3,000 TEU category.

Fleet composition compared to closest listed peers (Author’s calculations based on fleet data pulled from company websites, as of March 17, 2024)

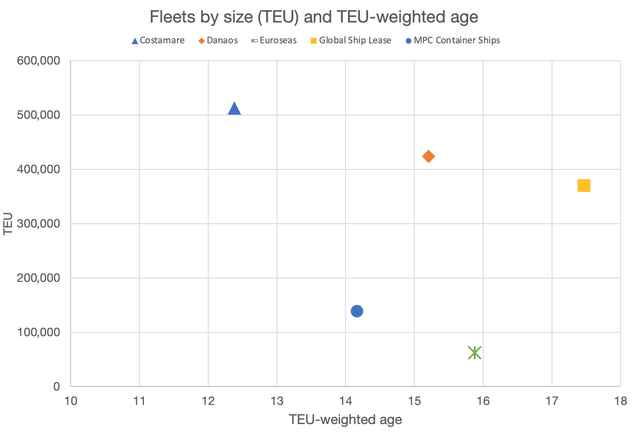

ESEA’s age profile is in the middle of the pack. It is much smaller than its peers (about one-ninth of Costamare’s). Comparing ESEA’s fleet to its peers on a TEU-weighted basis, the following image appears:

Fleets by TEU and TEU-weighted age. Euroseas and closest peers. (Author’s calculations based on fleet data pulled from company websites as of March 17, 2024)

A quick simulation of the effect of introducing an additional six feeder newbuilds shows that the TEU-weighted age of the fleet will go down to 13.7 years by the end of 2024:

| TEU-weighted age on March 17, 2024 | TEU-weighted age on December 31, 2024 | |

| 20 vessel fleet: six more newbuilds on order | 15.8 years | – |

| 26 vessels: all newbuilds delivered | – | 13.7 years |

This simplified analysis assumes that each ship on the existing fleet on water was delivered in the middle of the year (June 15), newbuilds delivered in the middle of the quarter of its announced delivery, and ESEA does not sell any vessels during the year.

Fundamentals

This section will compare Euroseas against its closest listed peers across the following metrics:

- Price/Earnings. An initial impression of its pricing compared to its peers

- EV/EBITDA. Another view of its pricing is comparing its EBITDA to its enterprise value.

- Dividend Yield. Does it yield more or less than its peers?

- Net debt to EBITDA (ttm). How is its debt load compared to its peers? How vulnerable is the company to lower rates?

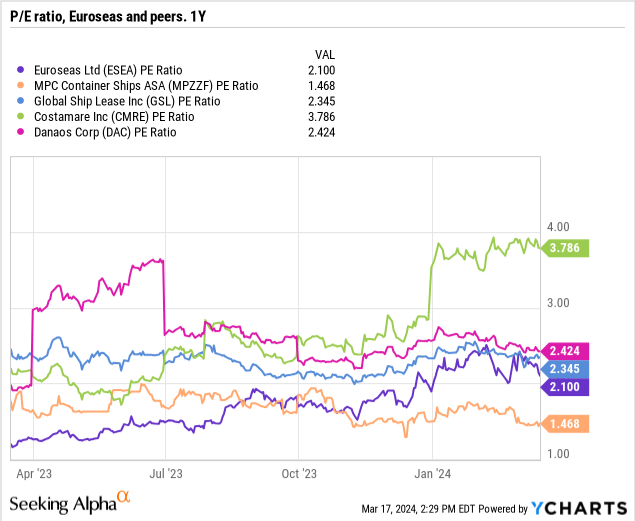

Price/Earnings

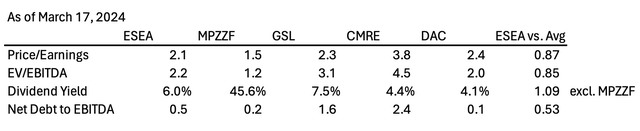

Euroseas has traded at a P/E close to its peers for the past year. In this group, the exception is Costamare, which recently went from less than 3 to close to 4 P/E. Costamare’s container fleet is mainly on extended charters. Still, it also has a significant exposure to the dry bulk market. Thus, one explanation could be the Baltic Dry Index’s rise from a trough of about 1,300 in mid-January to m 2,300 in mid-March.

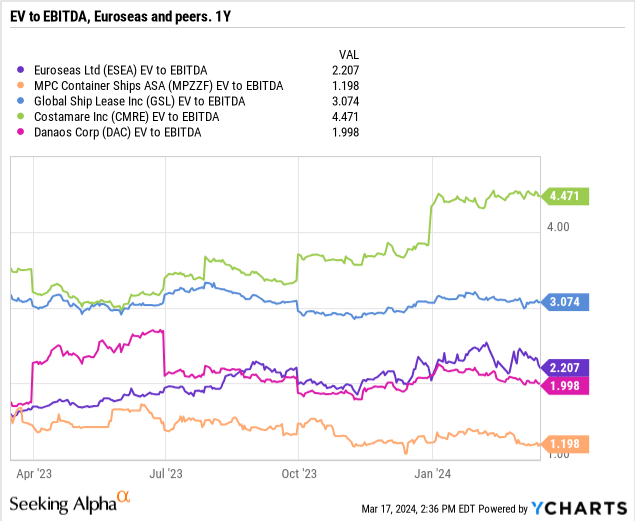

EV/EBITDA

Again Euroseas is in the middle of the pack. Regarding Costamare, the effect of dry bulk rates is also relevant here.

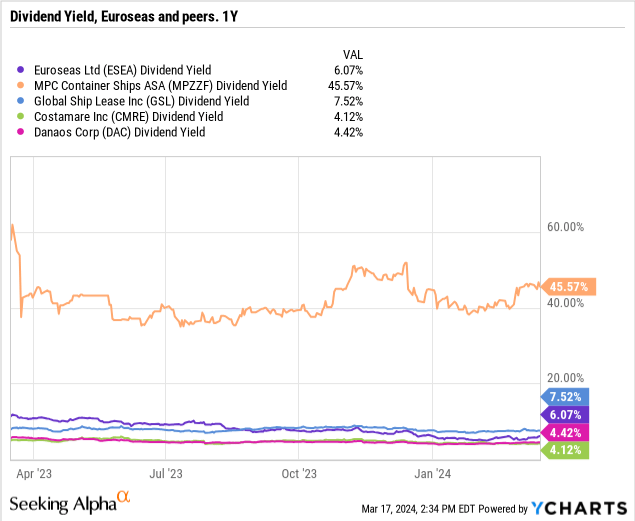

Dividend Yield

Euroseas and its peers have yielded between 4 and 8 percent for the past year. The exception is MPZZF, which has been running very high dividend yields for some time.

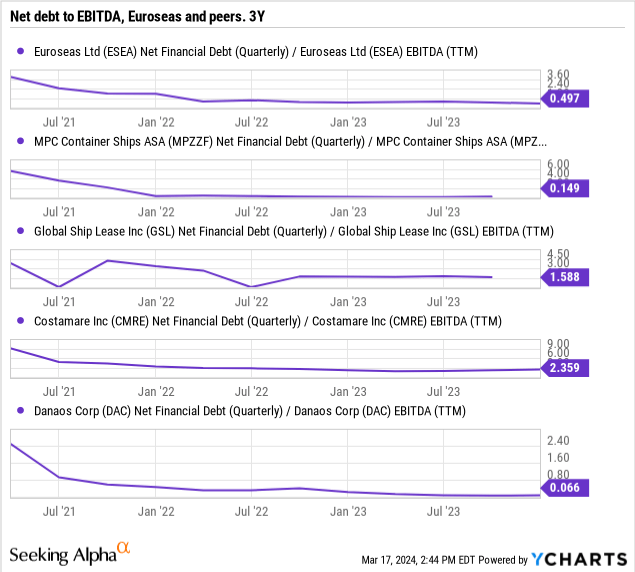

Net Debt to EBITDA

All four companies have followed the familiar deleveraging journey many if not most, companies within shipping have been on during the past few years. It’s unheard of to be net cash in a capital-intensive industry, which is the case for Danaos Corp. It has practically no debt.

Euroseas is just a little behind when compared using this metric, having traded at less than 1x EBITDA for the better part of a year.

Even Costamare, at a relatively high ratio of 2.4 in this peer group, is currently at low levels historically.

The table below summarizes these figures. ESEA is slightly cheaper than the average of this peer group as measured by P/E and EV/EBITDA.

Summary of valuation indicators (Author’s work based on YCharts graphs shown above)

Its dividend yield is slightly above average (MPZZF has been excluded as its dividend yield has been very high. In my view, it is not representative and sustainable). Finally, its net debt load is lower than average.

In conclusion, this fundamental analysis shows that Euroseas performs well when compared to its peers.

Market Outlook

On January 18, ESEA presented at New York-based Capital Link’s “Corporate Presentation Series,” where it discussed the market outlook extensively. It noted that while TC rates for its relevant segments (1,700-4,400 TEU) have come down since their pandemic peaks, rates are still above 2019 levels. The pandemic rates allowed shippers to enter long TC contracts, ensuring healthy cash flows into 2025. However, the global order book ballooned simultaneously despite uncertainties regarding future propulsion systems.

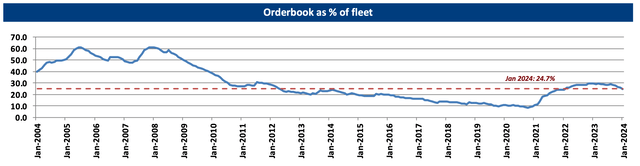

Order Book: The Worst in Years

This dynamic has caused the global order book (all ship sizes) to rise to nearly 30 percent of the fleet. It has since come down to just under 25 percent. A level not seen in about ten years:

Global order book as a percentage of fleet, 2004-2024 (ESEA Capital Link presentation (using Clarkson’s Research as their source))

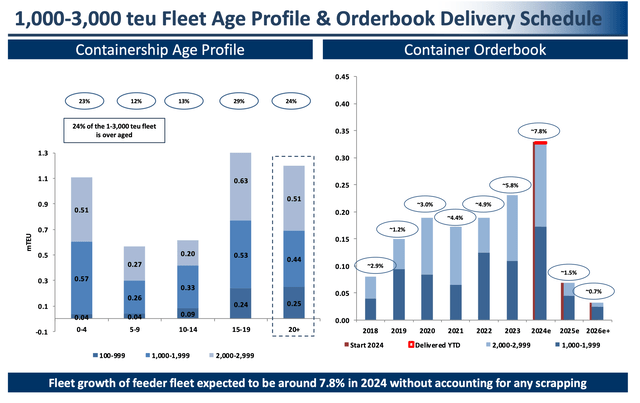

ESEA’s core feeder segment looks somewhat better but is still its worst in years, as measured by the new supply coming on water. Without any scrapping, the feeder fleet will grow by nearly 8 percent this year:

Feeder age profile and order book delivery schedule (ESEA Capital Link presentation (using Clarkson’s Research as their source))

The fact that many feeder ships are old (one in four ships are 20 years or older) may help, but uncertainties regarding future propulsion systems prevent owners from ordering as many ships as they otherwise would have. Also, just because a ship is 20 years or older does not automatically mean scrapping.

The market supply as a whole also has to be taken into account. According to the same presentation, TEU supply across all containership classes will grow by more than 11 percent this year, much higher than in 2023 (8 percent), which was still high. Individual segments do not exist in isolation: While a mega ship of, say, 14,000 TEU serves a different purpose than an intra-regional feeder of 1,000 TEU, the same clear distinction cannot necessarily be made between a 2,800 feeder and a 4,000 TEU intermediate ship. It’s ultimately all connected. Nevertheless, the feeder segment looks more promising than the rest.

Trade Growth: Not Enough to Absorb Added Supply By Itself

BIMCO reported soberingly on January 10, 2024, that – across all segments –

Once all the ships have been delivered [this year], the container fleet capacity will have grown by 10%. However, the container trades are expected to grow significantly slower. We forecast that the increase in container volumes will increase the demand for ship capacity by 3-4% in 2024.

The expected increase in container volumes this year aligns with ESEA’s message in its presentation (see p. 11). There, it reported an expected trade growth and GDP growth of 3-4 percent in 2024 and 2025.

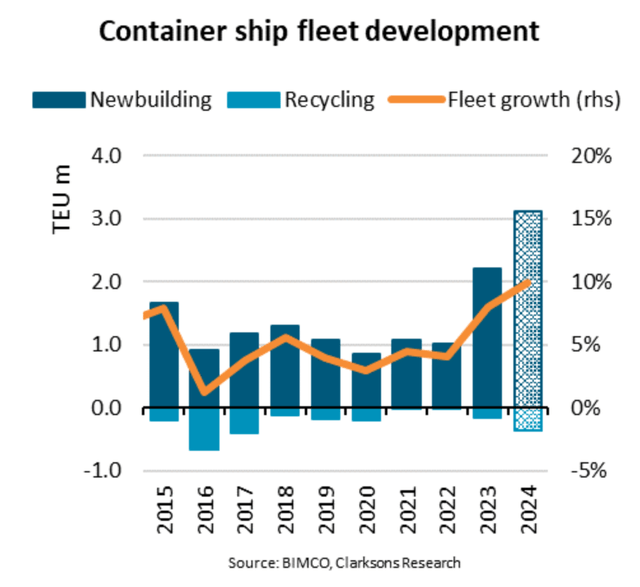

Recycling activity was very low in 2021-2023 and is not expected to pick up much this year:

BIMCO fleet development forecast 2024 (BIMCO, Clarksons Research, cited in Container News [March 17, 2024])

Is the World De-Globalizing?

The Russian invasion of Ukraine and the Houthi’s attacks on shipping in the Bab al-Mandab, thereby preventing the use of the Suez Canal, are two major world events that have altered shipping routes.

However, trends in international trade are also a factor.

Mainlane East-West trade volumes, largely driven by “western” economies, are expected to be 1.6 million TEU lower in 2023 than in 2019; though the eastbound Transpacific has gained 2.3 million TEU, only 100,000 TEU has been added to the westbound Asia-Europe trade, whilst Transatlantic, and backhaul volumes from North America and Europe to Asia, have shrunk. Volume growth has been focussed on trade involving developing economies.”

In other words, less global trade is moving East to West than before. U.S. imports from Asia over the Pacific are increasing, but it’s sending little back on the return. At a basic level, this trend implies that supply chains will be more dispersed: More countries and ports will be involved, thus requiring smaller ships. This could mean that intermediate and feeder ships will play a more critical role as we advance.

Conclusion

This article has provided an in-depth review of Euroseas, Ltd. It has considered its ownership structure, debt repayment profile, and fleet. It has also been compared to its closest listed peers using standard valuation metrics for dividend stocks. This has revealed a company that performs well compared to its peers and has been able to pay consistent dividends for two years. Finally, the market outlook was discussed. While there are positive signs in the market, the high level of uncertainty and sizeable global order book weighs on the industry’s prospects. Ultimately, this resulted in a Hold recommendation.

Read the full article here