I have written more and more over the past two years that the supply side of the economy is what is driving economic growth.

Why?

Well, I tried to explain this phenomenon in a recent post.

The argument goes this way. Technological change appears to be the real driving force in the U.S. economy these days.

Technological change is dependent upon innovators, both in the business world and in the academic community, and the innovators, in building the “new” world, are responding to situations where they believe advancements can be made.

Demand may not even exist for the “new” products and services at the time that the “new” is created and brought to market.

Furthermore, many of the “new” products are brought to market based on corporate “time pacing” strategies and have little or nothing to do with where the demand rests at the time the corporation brings the product to market.

Thus, it seems as if the supply side of the economy is generating most of the growth these days.

And, how has the supply side contribution been shown?

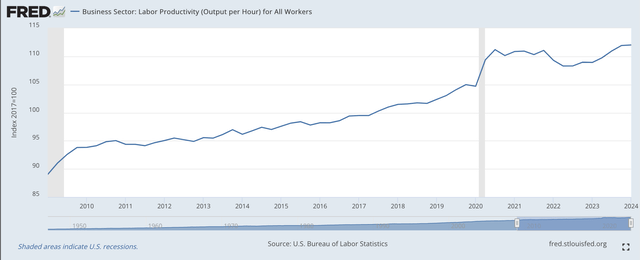

The supply side has been shown in the continuing increase in labor productivity.

In the following chart, we see how labor productivity has grown since the end of the Great Recession in 2009.

Labor Productivity (Federal Reserve)

From the end of the Great Recession until the start of the small recession that took place in 2020, the compound rate of growth in labor productivity was 2.1 percent.

One can see all the disruptions that took place during the COVID-19 pandemic and subsequent recession, but one can also see that the growth in labor productivity continued as the decade of the 2020s proceeded.

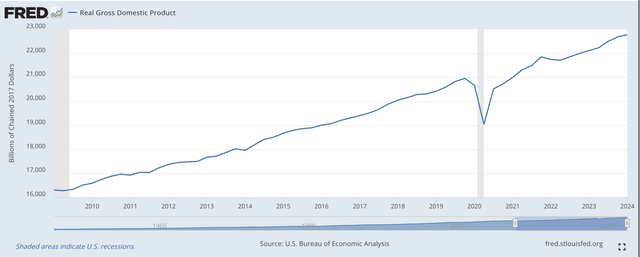

And, what happened to the real growth of the economy? Well, the performance of real GDP is pictured in the next chart.

Real Gross Domestic Product (Federal Reserve)

Notice…overall…the continued upward movement of the two charts over the complete period.

The compound rate of growth of real GDP was 2.3 percent, compared with the 2.1 percent compound growth rate in labor productivity.

Also, note that after the period of the COVID-19 spread and following the recession, the growth rate in the economy continued.

It appears that these two series moved very closely together over this time.

It seems as if the growth in labor productivity might have had something to do with the growth rate in the economy.

And, what about monetary policy during this period?

Well, this was the time period that Ben Bernanke, as Chairman of the Board of Governors of the Federal Reserve System, changed the focus of monetary policy.

Mr. Bernanke introduced a monetary process he referred to as “quantitative easing.” And, he oversaw three rounds of quantitative easing during his time as the Fed chair.

A round of quantitative easing saw the Federal Reserve add securities to its portfolio on a regular basis after the Fed announced to the markets what it was going to do.

There were no real market reactions to this policy, and the growth of labor productivity and the growth of the U.S. economy proceeded smoothly.

The supply side drove the economy, and inflation remained very modest during all three of the periods of quantitative easing.

Then the Covid-19 pandemic hit.

The Federal Reserve responded with another round of quantitative easing.

Then, because of all the disruption going on in the economy, inflation raised its head.

The Federal Reserve, in March 2022, responded with a round of quantitative tightening.

The economy picked up, and… as one can take from the charts… the supply side took over again.

As I have written steadily since then, there has been plenty of money in the economy, money that entered the economy during the fourth round of quantitative easing in the fight against the pandemic, so that the quantitative tightening did not distract the growth of the economy coming from the supply side.

And, here we are.

The U.S. economy has been growing more rapidly than analysts had suggested as the technological innovation in the country continued to accelerate.

The supply side is dominating the performance of the economy.

The Federal Reserve has “allowed” the supply side to dominate by sticking with its policy of quantitative tightening.

Mr. Bernanke must be very happy.

The Fed’s Policy Rate of Interest

Jay Powell, the current Chairman of the Board of Governors of the Federal Reserve System, given this scenario, is faced with what to do with the Fed’s policy rate of interest.

Mr. Powell had been suggesting that it will be reduced sometime this year… maybe several times this year.

Now, he seems to be backing off from this idea. Maybe there will be one reduction… maybe two… but, we may not even see these reductions.

What’s going on?

Well, two things.

First, the economy seems to be doing very well. We can wait and see if a drop in the Fed’s policy rate of interest is really needed.

Second, there is a presidential election coming this fall. Mr. Powell must be feeling the pressure. If the Fed does something, Mr. Powell… and the Fed… will probably be put under heavy criticism for what he… and the Fed… is doing.

The criticism?

Mr. Powell will be criticized for making a policy choice aimed at helping the current president get re-elected.

My guess is that Mr. Powell would like to avoid any decisions about changing monetary policy through November of this year.

We’ll see.

The Fed’s Balance Sheet

There was very little change in the Fed’s balance sheet this past “banking” week.

There was some usage of the Reverse Repurchase Agreement market, but the move was minor.

Overall, the Fed has now reduced its securities portfolio by a little more than $1.6 trillion. Also, the Fed has now reduced its use of Reverse Repurchase Agreements by $1.0 trillion.

Overall, Reserve Balances with Commercial Banks, a proxy for excess reserves in the banking system, have been reduced by $518.4 billion since March 16, 2022.

Thus, the Federal Reserve continues on its program of quantitative tightening.

Read the full article here