")

Introduction

Ferrari’s (NYSE:RACE) stock is one of the best businesses available in the market. Its predictability, and high profitability, together with its brand value addressing a well-protected niche of customers, make Ferrari a unique business. Personally, I am a bit surprised Berkshire Hathaway (BRK.A, BRK.B) has not yet stepped in and scooped up some shares. In fact, part of Ferrari’s moat is its high predictability which allows investors to make very good educated guesses about the future of this company. Moreover, Ferrari is also a dividend growth company, having grown its dividend at an 18.14% annual rate for the last five years.

Ferrari’s business model hinges on one core idea its founder Enzo Ferrari had: “Ferrari will always deliver one car less than the market demand”. As a result, Ferrari generates a sense of craving in its customer base, which is willing to pay high prices to secure a slot in the future order books of the Prancing Horse. Last, its TAM is estimated to be around 26 million people around the world (the so-called high-net-worth-individuals with more than $1 million of investable assets). Currently, Ferrari’s penetration is around 0.3%. This is why I consider Ferrari a growth stock.

Ferrari’s FY 2023 Results

Before we go over the results Ferrari recently reported for the fourth quarter and the whole fiscal year, I want to take a step back and go to Ferrari’s Capital Markets Day held in June 2022. Ferrari’s 2026 guidance was as follows:

- Net revenues around €6.7 billion

- Adj. EBITDA of €2.5-€2.7 billion (38%-40% margin)

- Adj. EBIT of €1.8-2 billion (27%-30% margin)

- Adj. diluted EPS €7.2-8

We should consider that these results were given when the company had just reported for FY2021 €4.3 billion in revenue, €1.5 billion in EBITDA (35.9% margin), and an EBIT of €1.1 billion (25.2% margin).

Let’s see where Ferrari is now that it reported its FY 2023 results.

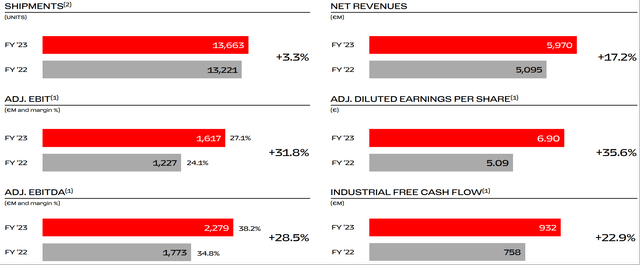

Simply put, 2023 was (another) record year for Ferrari.

Shipments were up 3.3% to 13,663 units. But net revenues were up 17.2% and breached €6 billion at CC. When we talk about pricing power… well, here is the perfect example to look at.

But things get even better as we move towards more important items on the income statement, those which usually support share price appreciation.

- Adj. EBITDA increased 28.5% to €2.3 billion, which is a 38.2% margin.

- Adj. EBIT increased 31.8% YoY reaching €1.6 billion or a 27.1% margin.

- Adj. EPS increased even more YoY to €6.9 or 35.6%.

On top of all these results, industrial FCF came just a bit shy of €1 billion and increased 22.9% YoY.

Ferrari Q4 2023 Earnings Presentation

How should we interpret these results? Ferrari delivered a master class in profit making, showing how every additional euro in revenue is much more accretive to its profits than the previous one. As a result, a 17.2% growth on the top line becomes a 35.6% growth of its EPS. Pricing power, efficiency, operating leverage, and buybacks all cooperate with this kind of income statement, which makes Ferrari’s execution almost flawless.

Let me spend a few words on the shipments increase. Some investors were worried that, after the pandemic, Ferrari’s sales were increasing too fast. The fear was that Ferrari would seek profits by selling more cars, damaging its exclusivity. But, as things normalize after the post-pandemic years, we see a very nice and smooth and moderate uptick in sales. This is exactly the volume increase I want to see. What matters most is that a shipments increase of 3.3% can generate 17.2% revenue growth, which fosters 35.9% bottom-line growth.

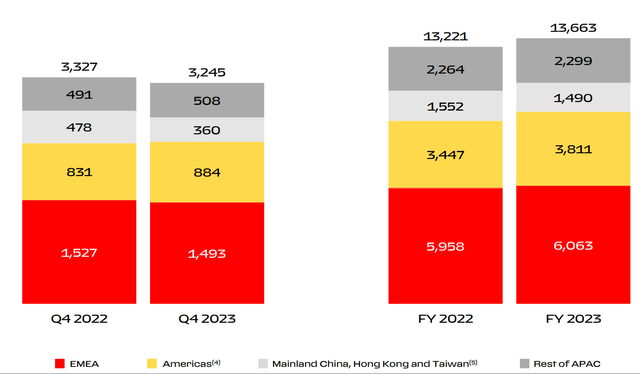

If we look at the sales breakdown by geographic regions we can easily spot how the majority of Ferraris are sold in the Western world. What may surprise some is China’s decrease, though by only a few tens of units.

Ferrari Q4 2023 Earnings Presentation

The fact China decreased a bit didn’t happen by chance. As already said, Ferrari controls its shipments quite carefully. In the earnings call presenting Ferrari’s Q4 results, Mr. Benedetto Vigna, the CEO, explained why Ferrari wants to keep China’s volumes low:

We will keep China, let’s say, around 10%, because it is not margin accretive. But again, it’s important that in each country as our history testifies, we let grow the attachment to the brand with the right speed. Because if you grow too fast, the clients don’t get used to what is Ferrari. This is what we have done in other countries and this is what we intend to do also in China.

I think these words brilliantly show how Ferrari works. The company is in no hurry to boost sales. It first needs to grow a loyal attachment to its brand. This happens by making customers feel the exclusivity and the privilege of being a Ferrari owner. Only where Ferrari’s customer base has reached this awareness can Ferrari unleash its full potential and increase its profits. So far, China is in the early stages as a market for Ferrari. Therefore, Ferrari needs to be even more exclusive in China than in other countries. In this way, China will turn into a margin-accretive country too. At that point, Ferrari will have the chance to direct some of its increasing volumes towards that market.

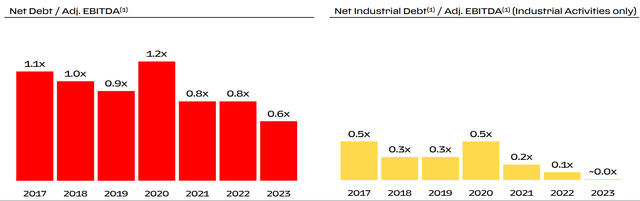

Let’s take a quick view of Ferrari’s leverage. Thanks to continuously growing FCF generation, the company has become almost net industrial debt free, as the chart on the right with the yellow bars shows. This is net of distribution to Ferrari’s shareholders of 85% of the industrial free cash flow generated through the fiscal year.

So why does the net debt/adj. EBITDA show the company still with some debt? Because Ferrari also has a financial services branch. This is where the debt comes from. Since I want my portfolio to be full of unleveraged companies, Ferrari fits perfectly with my plan.

Ferrari Q4 2023 Earnings Presentation

Moving on, we have to consider Ferrari’s 2024 guidance. As I tried to explain a few times, Ferrari usually underpromises to then overdeliver. I believe this is done on purpose for two reasons. First of all, Ferrari has great visibility on its order books. Therefore, Ferrari already knows its 2024 and 2025 sales. Secondly, Ferrari doesn’t know how personalized a car that has already been pre-ordered will be. Therefore, I have come to realize Ferrari guides as if it were to sell cars with very little personalization, to then surprise investors quarter by quarter because each car has generated much more revenue than first anticipated. We can then factor in sponsorships, mainly linked to the Formula 1 racing team and its results. This can swing by a couple of hundred million in the yearly net revenues.

Let’s spend a few words on personalization. This is becoming Ferrari’s new golden goose, paving the path for unprecedented growth.

Just in the last earnings call, the word “personalization” came up 30 times. A year ago, it came out only eight times. As Ferrari explained its top-line expansion, we listened to these words:

Personalizations continued to strengthen and in the last quarter, we witnessed a consolidation of the trend registered in the first nine months. In 2023, personalizations stood at approximately 19% in proportion to revenues from cars and spare parts, mainly driven by paint, liveries, and the use of carbon.

Together with the strengthening of personalization, Ferrari keeps having its order books full. The company disclosed in its earnings call, that “the exceptional visibility of its order book” allows the company “to look at the high end of the 2026 target with stronger confidence”.

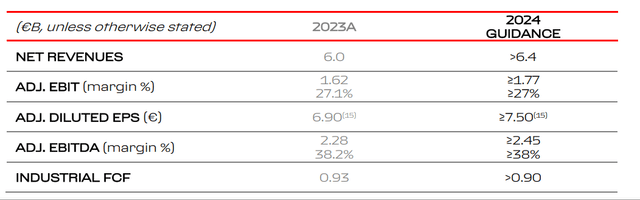

Let’s then look at the company’s guidance for this fiscal year.

Revenue is expected to come in above €6.4 billion. Adj. EBITDA should be at least €2.45 billion (over 38% margin), while adj. EBIT should come in above €1.77 billion (over 27% margin). We see a little decrease in industrial FCF. While I expect Ferrari to beat €0.93 billion in FCF, the company has been a bit prudent because it expects its capex to increase a bit during its investment cycle to launch the first e-Ferrari in late 2025.

Ferrari Q4 2023 Press Release

The only issue with Ferrari is its poor performance in Formula 1. It has been years since Ferrari has raced for the championship title. The same day of the report, Ferrari announced it signed the seven-time FY world champion Lewis Hamilton for its racing team in 2025. Better news could not be shared with Ferrari’s fans across the world.

Valuation

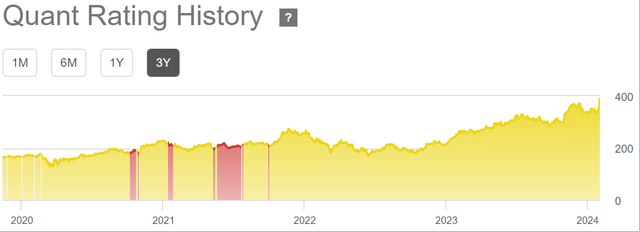

Here comes the tricky part. Ferrari is a high-quality business. However, it trades at a premium. This can make investors wary. Even the SA Quant Rating system has not been able to identify a buy alert since 2020.

Seeking Alpha

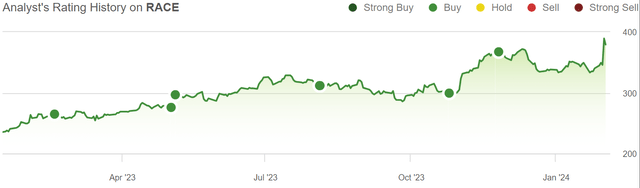

And yet, since my first strong buy rating in May 2022, the stock has returned 77%.

Seeking Alpha

It may seem I am bragging. I would actually want to use this situation to explain why I thought Ferrari was a strong buy even though it was already trading at a high valuation.

Let’s look at Seeking Alpha’s Factor Grades for RACE. The only issue here is with valuation. Growth is fine. Profitability is excellent. In the past six months, we have even had great momentum. Earnings revisions garner an A+ grade.

Seeking Alpha

It seems to me SA’s Quant Rating system weighs valuation more than those other metrics which actually can lead to strong price appreciation due to multiple expansion. With Ferrari, as said, it is rather easy to forecast its growth pace and its future profitability. Therefore, what seems today as a high premium may not be as demanding when considering where Ferrari is headed.

For example, back in May 2022 the stock traded around $190 and its TTM EPS was $4.93. This gave a TTM PE of 38. But those who bought at that time also bought a stock that was trading at an estimated 2023 EPS close to $7. This gave us a fwd PE of 27. Well, Ferrari actually reported EPS of €6.9 which is about $7.46. This means the fwd PE back then was 25.7. Not bad for a company like Ferrari. In fact, I think this valuation is more than reasonable and makes the stock seem cheap. We can run the same exercise with any other metric and we would find out the same thing.

Since Ferrari grows its top line at a 9-10% rate, while the bottom line grows even faster, it is easy to see how fast this company can compound.

Let’s do the same exercise looking forward. Right now, Ferrari’s TTM PE is 50. Very high, indeed. And yet, the company has proven to be able to grow its EPS above 15% per year. We could expect 2024 EPS to be around $8.58. This is a fwd PE of 44. But Ferrari usually over-delivers so we could assume the fwd PE to be a bit lower. Compared to 2022, the stock has become more expensive. And yet, I see no reason why the story around Ferrari should be changed. To me, the stock remains a buy. Perhaps, the only thing to do right now is to be a bit patient and dollar cost average instead of buying all at once. Every once in a while, Ferrari does dip. But it is hard to forecast when and why it should. As a long-term investment, I hardly find better companies to pick.

Read the full article here