")

In my previous article, I expressed my bullish view on Alphabet Inc. aka Google (NASDAQ:GOOGL), highlighting the normalization of the advertising business, and their AI model of Gemini. Alphabet released their Q1 FY24 result on April 25th, beating the market expectations. Their advertising business continues the growth momentum with a 14.4% increase in Google Search. Most importantly, their cloud business grew by 28.4% year-over-year, and the operating income more than quadrupled to $900 million.

I continue to think Gemini has the potential to strengthen Google’s leadership in the search market. I reiterate a “Buy” rating with a fair value of $217 per share for the class A — GOOGL — shares.

Cloud Growth Acceleration and Margin Improvement

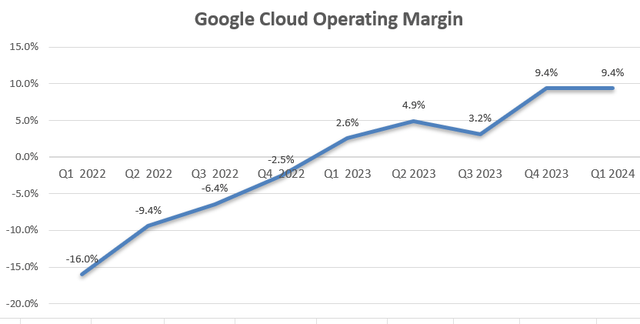

My biggest takeaway for this quarter is Alphabet’s ongoing improvement in the operating margin of Google Cloud. As depicted in the chart below, Google cloud’s operating margin has shown steady improvement over the past few quarters. My biggest concern in the past was their unprofitable cloud business. By comparison, Amazon’s (AMZN) AWS achieved a 27.1% operating margin in FY23. It indicates that Alphabet has a huge room for the margin expansion in the future.

Alphabet Quarterly Earnings

I think there are several factors contributing to the margin expansion of Google cloud:

- -Scale: Compared to Amazon and Microsoft (MSFT), Alphabet is the smallest players in the cloud infrastructure business. Due to the lack of scale, it is harder for Google to achieve operating leverage from their cloud business. To provide cloud infrastructure, all hyperscalers need to invest heavily in the early stage to build up data centers and expand all kinds of services including database, security, data analytics, and AI models.

- -Alphabet started to manage their overhead costs after FY22, and they underwent some restructurings to optimize their cost structures. In Q1 FY24, the total of headcount declined by 5.1% year-over-year, reflecting Alphabet’s layoffs and slowdown in hiring.

- -As communicated over the earnings call, Google Cloud has experienced strong growth in average revenue per seat, resulting in additional revenue growth from AI and Google Workspace. As indicated in my previous article, Alphabet has been investing in their Gemini AI model, and applying Gemini to all of Alphabet’s platforms. In February 2024, Alphabet launched Gemini 1.5 Pro and in April 2024, they made Gemini 1.5 Pro available in 180+ countries. The advanced AI models strengthen Google Cloud’s core advantage, enabling enterprise customers to adopt AI computing and transition to cloud.

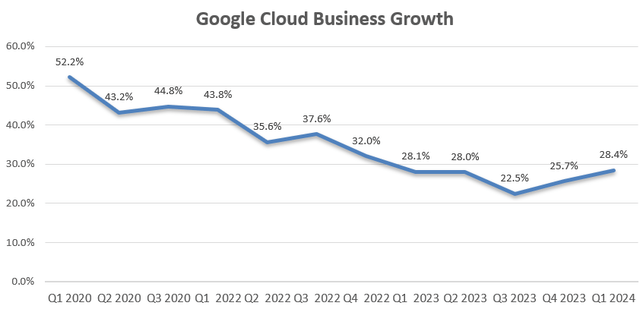

In addition, Google Cloud business has started to accelerate growth since Q3 FY23, as illustrated in the chart below. Starting from late FY22, enterprise customers began to optimize their cloud spending, resulting in some growth deceleration for all the major hyperscalers. It appears that cloud optimization activities have been moderating in recent quarters. Microsoft’s cloud business also grew by 21% in the recent quarter. I anticipate the cloud infrastructure will continue to grow at a fast pace in the near future, considering the structural demands from digital transformation, AI, and cloud computing.

Alphabet Quarterly Earnings

Growth Acceleration of Core Advertising Business

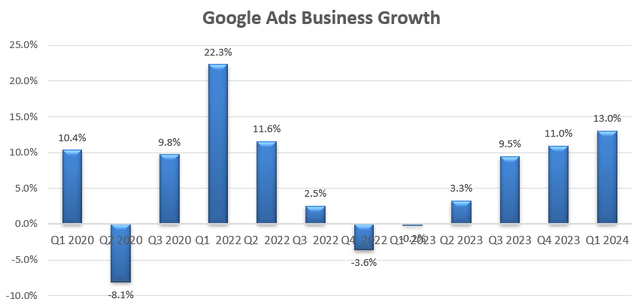

Google Search increased by 14.4% in revenue, and YouTube Ads surged by 20.9% year-over-year. As I forecasted in my previous article, Google Ads business started to recovery since Q2 FY23. Similar to Meta Platforms (META), Alphabet has started to apply their AI model to their core advertising business. The large language model could potentially make digital marketing more attractive to advertisers, in my view.

Alphabet Quarterly Earnings

As indicated over the earnings call, AI models are being implemented across their advertising ecosystem including targeting, bidding, creative and measurement. With both Alphabet and Meta developing their in-house AI models, I anticipate that both Alphabet and Meta continue to apply their AI functionality to their core digital advertising business in the near future.

FY24 Growth Forecast

I think about the following factor for Alphabet’s growth:

- – Google Cloud: Both Microsoft and Alphabet are delivering 20%+ revenue growth in the past quarters. As discussed previously, cloud optimization activities have begun to moderate in recent quarters. Therefore, the growth of cloud infrastructure is unlikely to decelerate in the near future. Additionally, enterprises have been investing heavily in AI related workloads, resulting in increased demands for cloud infrastructure. I forecast Google Cloud will grow at 25% in FY24.

- -Advertising Business: The business growth is tied to enterprises’ budge for digital marketing. Expert Market Research forecasts that the global digital marketing market will grow at a CAGR of 13.1% from 2024 to 2032. Considering the current high-interest rate environment, I anticipate enterprises will remain cautious with discretionary marketing spendings. Alphabet and Meta possess the advantage of in-house AI models which could boost ROIs for advertisers; thus I forecast Alphabet can maintain their leadership in the digital advertising market. I forecast they can deliver 13% of growth for their advertising business.

- – Google subscriptions, platforms, and devices: the business has consistently delivered double-digit revenue growth driven by a growing number of subscribers and price increases. I expect the company to continue the growth momentum, delivering around 10% revenue growth.

As such, I calculate that the total revenue growth will be around 14%, with cloud contributing 3% growth, ads adding 10%, subscriptions contributing 1%.

Valuation Update

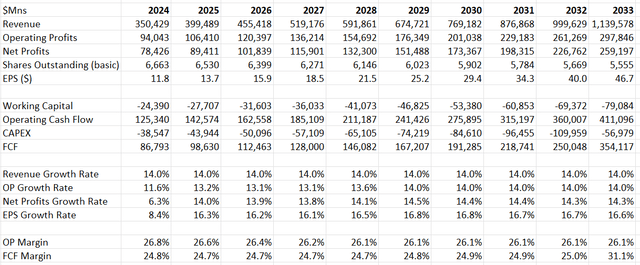

As Alphabet needs to invest heavily in their AI business, they have allocated more than 10% of total revenue towards CAPEX in the past two years. I forecast that they need to maintain similar investments in R&D and CAPEX to build up their advantage in the AI area and compete against with other AI companies like OpenAI, Microsoft, Meta and Amazon.

Due to these heavy investments, it is unlikely for Alphabet to expand their margin notably in the near future. In addition, in the coming years, Alphabet is going to incur higher depreciation costs due to their increased CAPEX spending in the past few years. As such, I assume they must allocate 14.8% of revenue towards R&D, 9.1% towards sales/marketing, and anticipate a 20bps leverage from gross profit.

Alphabet DCF – Author’s Calculations

The WACC is calculated to be 12.3% with the following assumptions:

- -risk free rate: 4.6% per US 10-Y treasury yield (US10Y)

- -beta 1.15 (SA)

- -equity risk premium 7%; cost of debt 7%

- -tax rate: 17%

- -debt balance: $13.2 billion; equity $283 billion.

Alphabet ended the quarter with $108 billion in cash and cash equivalents. Adjusting the cash and debt balances, the fair value is calculated to be $217 per share for the class A shares, as per my estimates.

Key Risks

Competitions from other AI companies: I view the competition from other AI companies as the biggest risk for Alphabet’s search business. Google Search still relies on keyword searching currently. However, as the technology advancement of AI, the way of future internet search could be entirely different. For instance, end-uses could have a conversational type of Internet search. OpenAI and other AI companies could potentially enter the search market to compete against Alphabet and Meta.

High CAPEX Spending: There were several analysts raised concerns about their capital expenditures over the earnings call. Alphabet spent 11.1% of revenue on CAPEX in FY22 and 10.6% in FY23, and their capital expenditure is unlikely to slow down in the near future, as discussed previously.

Conclusion

I am encouraged by their cloud business growth acceleration and notable margin improvement. Compared to Amazon’s AWS, I think Google Cloud has a huge room for margin improvement in the near future, in my view. I believe their investment in Gemini and other AI capabilities could potentially enhance their core advertising and cloud businesses. I reiterate a “Buy” rating with a fair value of $217 per share for the Alphabet Inc. class A shares.

Read the full article here