")

Hibbett (NASDAQ:HIBB) is an American footwear retailer with brick-and-mortar operations concentrated in the country’s southeast.

I wrote about Hibbett in October 2022 with a Hold rating. The stock was trading at a low multiple on current earnings (less than 10x). However, I didn’t like the company’s historical operations (particularly its lack of SG&A expense control) and considered it a risky proposition for a then very feared recession.

In the year and a half since that article, Hibbett’s stock moved down almost 50% into mid-year 2023 to recover 100%, now 35% above the price I issued a Hold in 2022.

In this review, I find the company’s sales have decelerated, which is understandable given the context and the pandemic comparables. However, the company has controlled costs, a positive departure from the previous trend. On the competitive side, the company seems to be one of the less damaged partners of Nike’s DTC strategy because of its store locations and target demographics.

Despite the price increase, Hibbett continues to trade at low multiples of current earnings. The company is also well prepared to weather several economic downturn scenarios. I consider the stock an opportunity, albeit in a low concentration, given the always-present risk of Nike’s strategic shifts.

Resilient operations

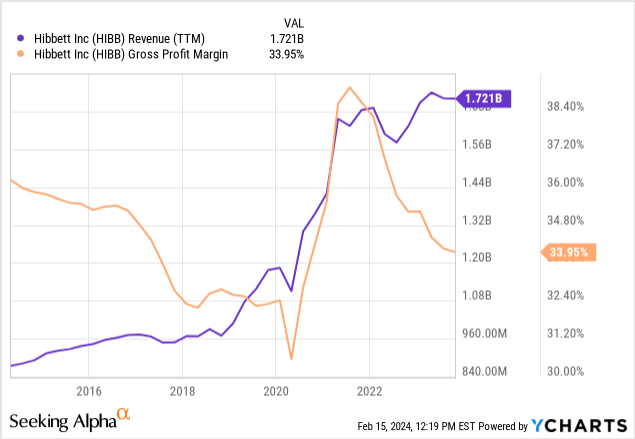

Hibbett’s fiscal 2023 showed a deceleration in revenue growth and decreased gross margins. On the revenue side, this is understandable, given the boom in consumption caused by the pandemic stimulus is no longer in force and that inflation and higher rates are affecting consumers. On the margin side, I believe the margin fall is also logical and was seen in different forms across many companies. Some companies saw an original margin decrease after the inflationary surge of 2022, to then increase prices and recover margins. Others, like Hibbett, saw prices increase faster than inflation, enlarging margins, and then suffered from higher input prices.

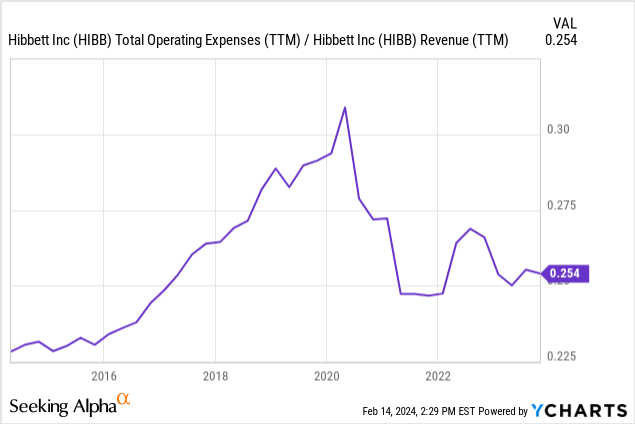

While the revenue deceleration and margin decrease are relatively normal, I commend the company’s control over SG&A expenses, especially with the previous trend as a comparison. During the pandemic surge in consumption, SG&A to revenues decreased (imagine a store employee that can now sell more shoes). However, the cost effect that decreased gross margins did not affect the company’s SG&A expenses (that same employee sells the same shoes but asks for a higher wage). The company says it could do so via personnel and advertising cost controls.

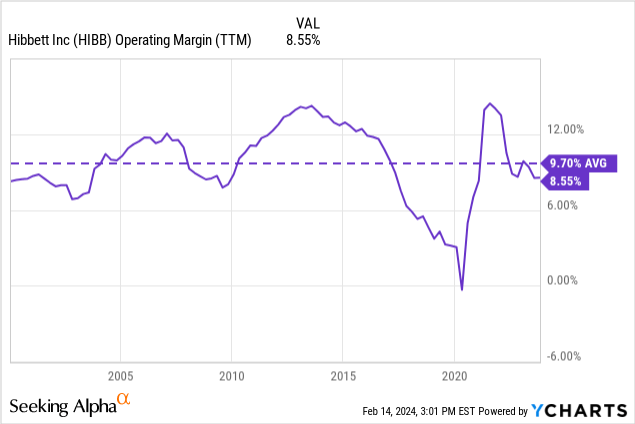

Controlling SG&A expenses is crucial for the company’s resilience via maintaining high operating margins and avoiding high operating leverage. For example, compare the damage caused to operating margins of the 2008 Great Financial Crisis (a few percentage points) with the enormous damage caused by the lack of SG&A controls between 2015 and 2019. The company suffered more from its own hand between 2015 and 2019 than because of the greatest crisis in the past 80 years.

Another source of resilience is the company’s relatively unlevered balance sheet. The company has about $30 million in cash and $400 million in inventories against total current liabilities of $316 million and long-term capital leases of $240 million. The company’s line of credit represents only 25% of inventories, at $95 million.

The e-commerce and DTC problems

A generally accepted view is that brick-and-mortar retailers are at significant risk of finding their markets stolen by e-commerce companies. This added to operational leverage, makes many retailers trade at low multiples of current earnings.

In the case of Hibbett, this fear is compounded by the challenging relationship with its leading supplier, Nike. The shoe company has been boasting a DTC strategy that has left its wholesale retailers with less space to breathe each year.

Being treated as a wholesale B&M retailer class member, the company is given a valuation that implies its business is at significant risk. However, I believe there are reasons to be more hopeful about Hibbett.

On the e-commerce side, retail thinking leaders like Dough Stephens or Steve Dennis agree that there are subclasses of retailers that can survive the attack of Amazon, and even more that of DTC vertically specialized brands (think Zappos).

According to these authors, the requirements are first for the competitive retailers to provide value and engagement with their customers that are so unique that DTC brands or e-commerce giants cannot replicate, and second, to offer an excellent digital-physical experience mix.

In the case of Hibbett, the company’s management has articulated its niche strategy as serving the fashion-obsessed young consumers of small southeastern towns. Hibbett’s unique value is access to difficult-to-find, trendy products (this is called the Gatekeeper or Tastemaker functions by Stephens). Some quotes that exemplify this from the company’s management:

- We do not service personas that are slower on the fashion adoption curve.

- We know that if we win with Gen Z, we win with everyone.

- Our brand partners recognize the importance of the small-town sneakerhead and our ability to serve them.

- This move allowed the company to enhance a selection of premium brands, for example, Nike, Jordan, Adidas, Puma, Levi, Grindhouse, and others, which meant that we moved into a space that allowed us to begin offering a hard-to-access compelling assortment of hard-to-get product.

In the case of Hibbett, sneakers are a sought-after product by their demographic and artificially rendered scarce by Nike. Some sneaker models are so scarce that Hibbett developed a proprietary raffle system because people complained that resellers hoard Nike’s supply.

The company’s digital channel is also vital, as exemplified by the raffle system above and the share of digital sales. Last quarter, digital sales were 17%, low compared to Nike’s 39% of direct sales done digitally, but still meaningful.

The Nike risk

Still, Hibbett’s value proposition depends on getting supplies from Nike. The company’s moat is gone if the shoemaker decides not to provide Hibbett with the latest trendy articles.

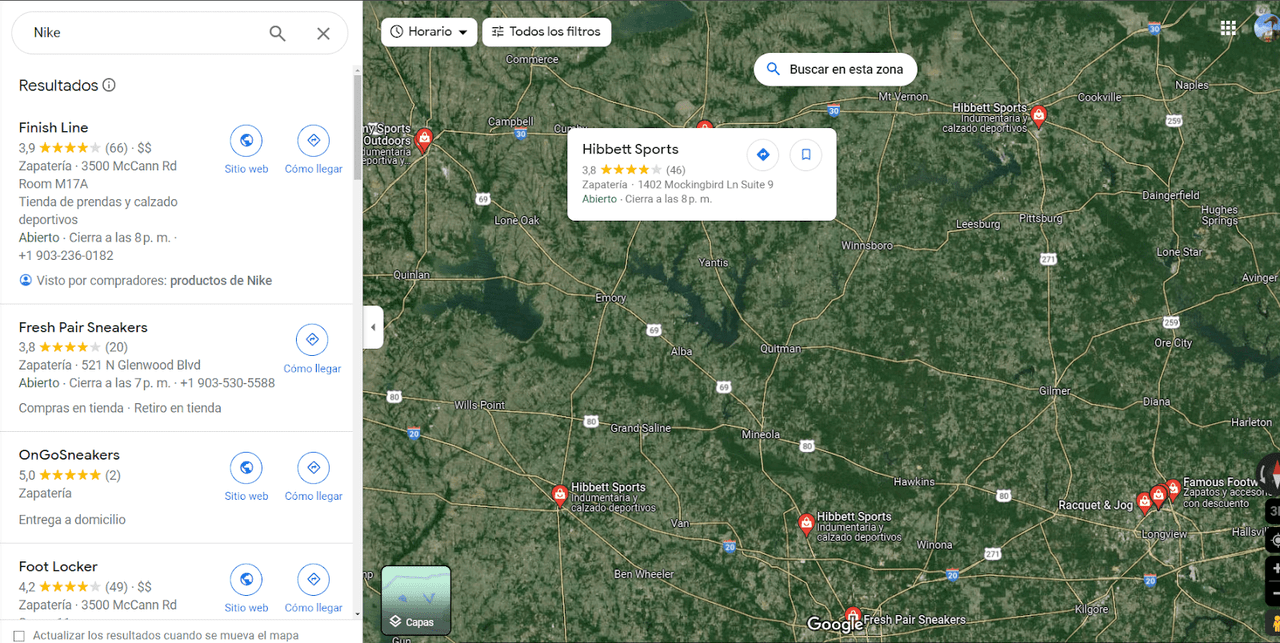

The bullish argument is that Hibbett is protected because it has stores in rural areas without direct competitors (in the young, fashionable demographic). The company has commented that 70% of its stores have fewer than two competing stores within a 3-mile radius carrying inventory from the same suppliers (i.e. Nike).

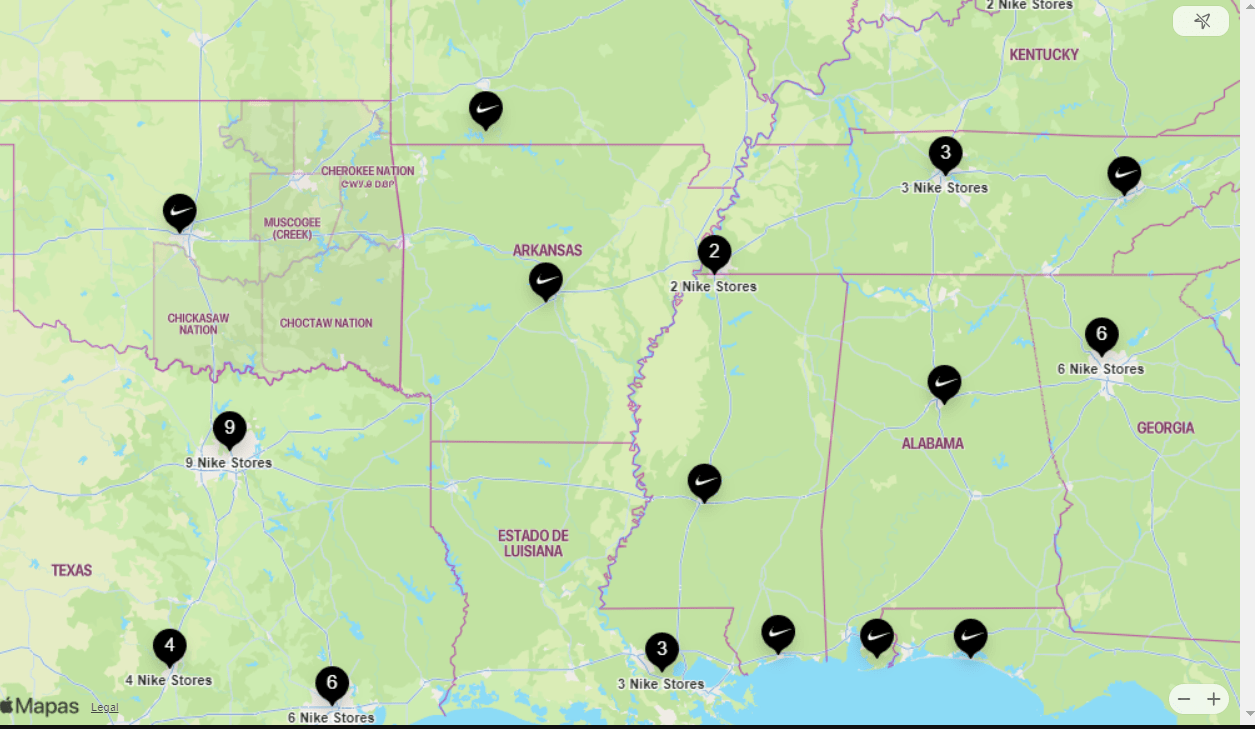

Indeed, a search for Nike in rural areas of the US Southeast reveals that Hibbett is the only provider in most towns. A search in Nike’s store locator also shows that the shoemaker only opens stores in the state’s main cities, often only one per state. This means that as long as brick-and-mortar drives traffic and sales, Nike benefits from having Hibbett as an ally because it is not competing with their stores or digital sales.

Still, I believe this risk is genuine and commands a discount to the company’s multiple to be compensated. Hibbett cannot escape Nike’s dominance because the shoemaker owns the sneaker market (it sold more sneakers than the five following competitors combined). A significant strategic challenge for Hibbett would be to differentiate into other trendy categories where Nike is not as strong.

Nike search west of Dallas, most results are Hibbett (Google Maps) Nike search south of Birmingham, AL (Google Maps)

Nike search south of Memphis (Google Maps)

Nike stores, US southeast (Nike store locator)

Valuation and conclusions

Hibbett currently trades at a market cap of $850 million. Against its TTM net income of $110 million, this represents a P/E ratio of 7.7x on a GAAP basis. I believe this is a decent return in exchange for the Nike risk.

Assuming the company can keep operating margins at historical average levels of 9% (maintained even during the GFC, as mentioned, except because of self-inflicted wounds in the 2015-2019 period), then it would still return a 10% earnings yield ($85 million in net income) if the company’s sales fell to $1.3 billion, or 25% from current levels.

Further, assuming the company’s SG&A expenses are fixed (a bearish assumption given that seasonal and extra-hour personnel can be adjusted), its sales should fall to $1.3 billion before breakeven (with current 33% gross margins).

As mentioned, the company’s balance sheet is strong. Its credit facility only finances 25% of the company’s inventories, the company has cash equivalent to 30% of the facility, and its equity almost doubles its total lease liabilities.

Finally, the company is currently opening stores, draining operational cash in working capital and CAPEX (fixtures and renovations for the stores mostly). I believe the CAPEX will continue, as stores require investments to keep being relevant. Still, in a more steady state, Hibbett should be able to match net income in terms of FCF at least (via lower investment in working capital), potentially opening the gate for more repurchases. Hibbett has been a cannibal in the past.

In the future, I will closely follow developments in specific areas: SG&A cost controls, diversification to product lines where Nike is not a leader, and share repurchases that are self-financed (not via credit facility). These would be interesting aspects to note in the next earnings release and call.

Read the full article here