")

Introduction and Background

I took advantage of the recent weakness in the market to add many high-quality dividend growers to my dividend growth portfolio. I don’t always time investments perfectly, but by maintaining a watchlist of around 100 of the highest quality companies that pay growing dividends, I am able to take advantage of times when the stocks of those companies trade below fair value, regardless of what the broader market is doing. Even though the market has strengthened relative to recent weakness, I believe there are still bargains to be had in this dividend growth portfolio journey.

One of my favorite ways of looking for value in this high-quality dividend growth space is to screen for those stocks trading near 52-week lows. For this exercise, I decided to filter my watchlist by companies that are trading at less than 30% of their 52-week range (52-week low being 0% and 52-week high being 100%).

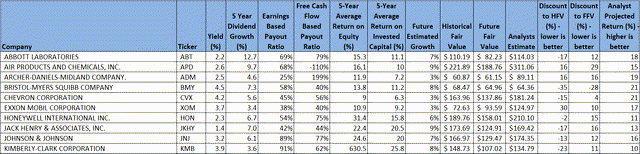

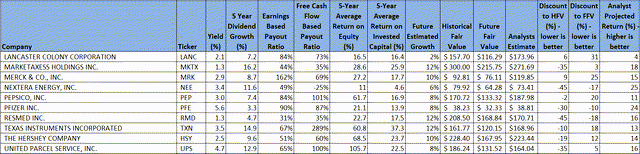

Using this first pass criteria, we will be looking at the following list of companies:

FinBox, Seeking Alpha, Author’s Analysis FinBox, Seeking Alpha, Author’s Analysis

Fair Value Estimation

As I’ve described in previous articles, I like to calculate a fair value in two ways, using a Historical fair value estimation, and a Future fair value estimation. The Historical Fair Value is simply based on historical valuations. I compare 5-year average: dividend yield, P/E ratio, Schiller P/E ratio, P/Book, and P/FCF to the current values and calculate a composite value based on the historical averages. This gives an estimate of the value assuming the stock continues to perform as it has historically. I also want to understand how the stock is likely to perform in the future so utilize the FinBox fair value calculated from their modeling, a Cap10 valuation model, FCF Payback Time valuation model, and 10-year earnings rate of return valuation model to determine a composite Future Fair Value estimate.

I also gather a composite target price from multiple analysts including Reuters, Morningstar, Value Line, FinBox, Morgan Stanley, and Argus. I like to see how the current price compares to analyst estimates as another data point, and as somewhat of a sanity check to my own estimates.

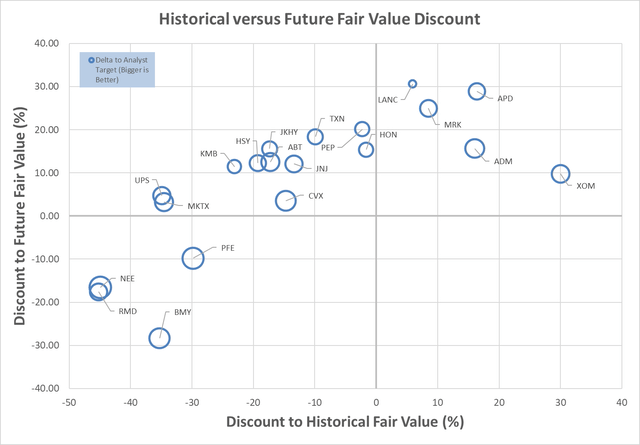

Plotting three variables on one plot is tricky but using a bubble plot allows us to visualize three variables by plotting the Historical fair value versus the Future Fair Value on a standard x-y chart, and then use bubbles to represent the size of discount relative to analyst estimates.

Author calculation of Historical and Future Fair Value, analyst estimates

This chart is insightful once you understand how to interpret it. What we are looking for are stocks that are trading at a discount to both the Historical Fair Value and the Future Fair Value. So, those stocks that are farther to the left, and farther to the bottom, are potentially the stocks trading at the largest discount to fair value. This would be the bottom left quadrant of the graph. Additionally, those stocks with the biggest bubbles are the stocks that are trading at the largest discount to analyst estimates, so in theory, stocks in the lower left quadrant that also have large bubbles, should be very decent candidates for investment.

The chart suggests that Pfizer (NYSE:PFE), Bristol-Myers Squibb (BMY), ResMed (RMD), and NextEra Energy (NEE) are attractively valued from a Historical and Future Fair Value perspective.

I currently own all these stocks and believe that each could be an excellent candidate for further investigation, and potential investment, especially for long-term investors.

I have recently published an article on BMY here, that I believe is still relevant to help with further investigation.

Of these four stocks, I have made recent investments in BMY, NEE, and RMD. I have been watching PFE to also add to my position. My average cost in PFE is a little over $35, so based on my valuation estimates, and the current price relative to my average cost, assuming nothing has changed in my estimation of the quality of PFE, this could be a good point for averaging down.

Pfizer Preliminary Analysis

I like to start simple when analyzing companies. PFE has a 5-year average Return on Equity of 21% and Return on Invested Capital of 14%. These are solid values and the RoE and RoIC numbers are reasonably close, suggesting that management is likely not using excessive debt to increase RoE. Additionally, the weighted average cost of capital for PFE is around 9%, suggesting opportunity for continued mid-single digit growth when compared to the RoIC. Probably nothing to get too excited about, but it should allow margin to comfortably sustain the business. Morningstar’s Wide Moat rating is excellent, and the Standard Capital Allocation rating doesn’t draw red flags. PFE is currently 5-star rated at Morningstar, suggesting it could be very attractively valued.

Now, looking at the dividend, PFE’s 90% Earnings-based payout ratio and 87% Free Cash Flow-based payout ratios do raise some questions. These don’t provide much margin for downturns without taking on more debt, which is more concerning in this period of higher interest rates. The 5-year dividend growth rate of around 3% is also not great, though the starting yield around 5.6% is very good, especially for a high-quality, relatively safe investment. My estimated future growth rate for PFE is above the dividend growth rate, so provides some comfort that the dividend should be sustainable, even given the high payout ratios.

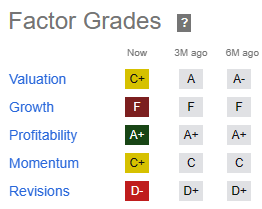

One more source I like to check are the Seeking Alpha Factor Grades. Though these tend to be more short-term in focus than my investment horizon, I consider the grades as a guide of what to look for in answering the question of whether the valuation may be due to shorter term issues, or more systemic.

Seeking Alpha

The factor grades don’t look great if you’re a 4.0 student, but digging a little deeper, as we’ll look at in more depth, the current valuation is not as attractive as it has been, even though the price is lower. The growth has been poor due to coming off the COVID vaccine windfall, though may be turning around in the future, but profitability still looks really good, which we need to confirm for the future. So, let’s get to it.

Pfizer Historical Valuation Analysis

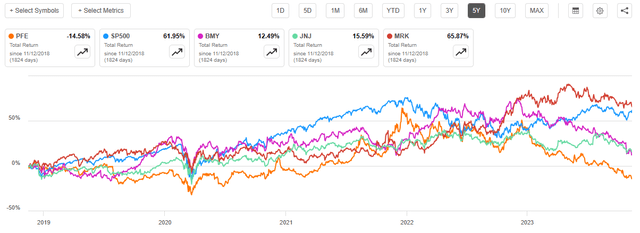

I always like to start my historical assessment of a stock with a look at performance compared to the S&P500 and relevant peers over the past. This isn’t particularly useful by itself, but can provide an indication of potential, as well as sentiment. I decided to throw BMY, JNJ, and MRK onto the chart for comparison, since they are similar companies, and part of the filters above.

Seeking Alpha

It is safe to say that most people aren’t likely to invest in PFE based on its 5-year historical performance. If you have invested 5 years ago, even with dividends, you’d be sitting on almost a 15% loss. It is also worth noting that PFE is trading only a couple of dollars per share above the low point hit during the COVID market downturn. Based on this, why would you invest in PFE? Well, obviously, we’re looking for signs that the stock is a true value, and that better days are ahead, leading to future appreciation potential.

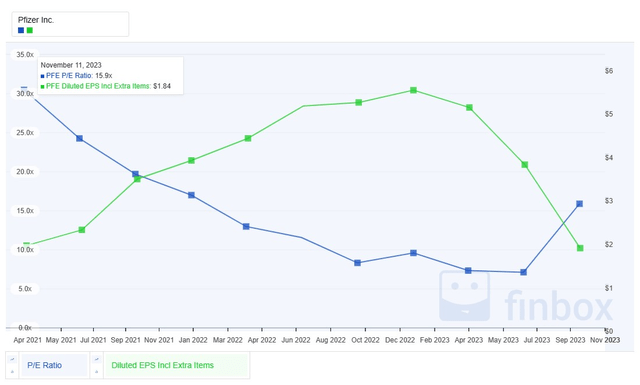

From a historical comparison perspective, two of the fundamentals I like to investigate are historic P/E and yield. Low P/Es relative to history, coupled with high yields compared to history can often indicate attractive valuation, assuming the underlying business is sound.

PFE’s average P/E chart shows that it may be highly valued relative to its 5-year average of around 13. It is also higher than recent lows that were achieved at higher stock prices, which obviously shows that the most recent results are lower from an earnings perspective than they have been, which is seen with the overplot of EPS.

FinBox

From a yield perspective, PFE is higher than the 5-year average of 4.3%. The 5.6% yield compared to the average of 4.3%, suggests it could be attractively valued on a yield basis, or in decline. If we can be confident the stock is not in decline, the yield compares favorably to many bonds, and with the added opportunity for capital appreciation, could suggest an attractive investment option. At a minimum, if the dividend is safe, the income derived could be a good option for those looking for dividend income, instead of growth.

FinBox

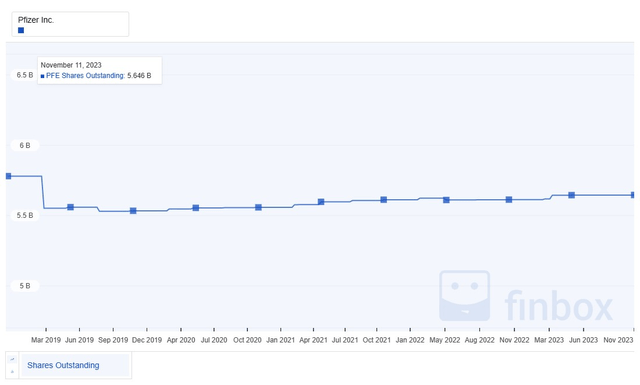

A key part of the Total Shareholder Return includes stock buybacks, which are also important to dividend growth sustainability. PFE has not been strong on share buybacks, with increasing shares outstanding over the past several years. This creates shareholder dilution but also makes it harder to pay an increasing dividend, since not only is the amount of the dividend increasing per share, but the number of shares is also increasing, creating a double whammy.

FinBox

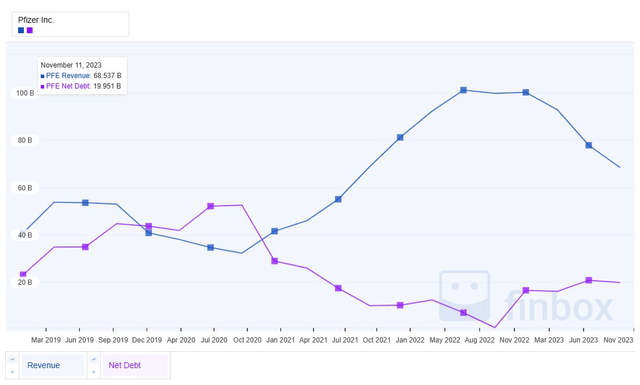

PFE has had a fairly high debt load historically, however, with the windfall COVID vaccine revenue, PFE was able to use that to pay down debt. Now that those revenues are waning, debt is coming back up, but so far, not to the levels of the past. This is a key measure to watch – will debt increase compared to revenue?

FinBox

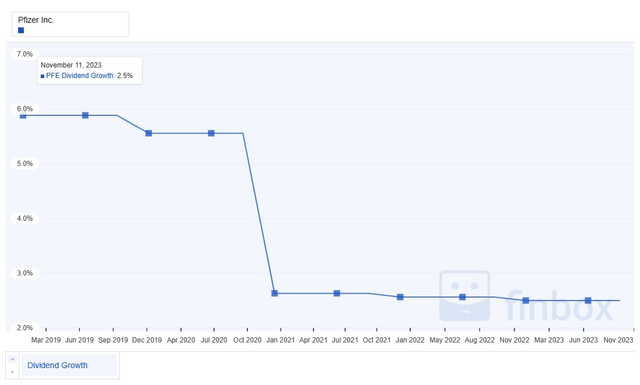

PFE has been paying a growing dividend for around 13 years after a cut. I don’t like to see companies that have cut their dividend in the past. The 5-year average growth is a rather anemic 3%. The story on this one is clearly initial yield, not growth, though if they could return to the growth of the past, which was around 6%, that would be more attractive.

FinBox

One question to ask is why, if PFE had such strong tailwinds with COVID, didn’t it raise the dividend higher? Is this a sign of a lack of confidence by management? Well, one reason is highlighted above, which is that debt has come down. Another interesting perspective is to look at R&D. There is a clear bubble in R&D expenses during the COVID timeframe. Obviously, some of this was directly related to the investments in the COVID vaccine, but it also appears that PFE has been investing the windfall in incremental R&D, which could benefit growth in new product revenue going forward.

FinBox

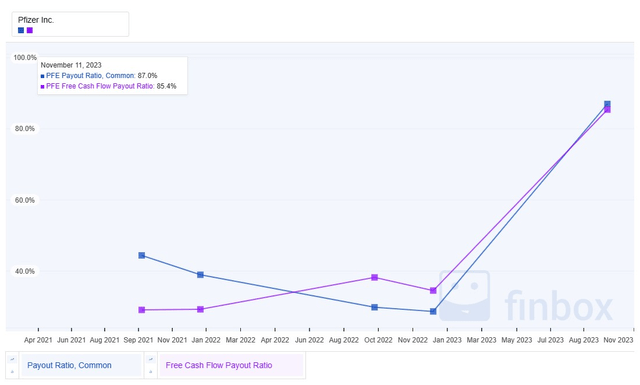

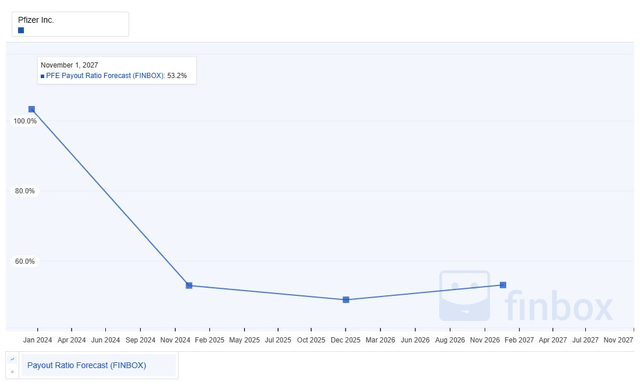

Dividend growth doesn’t do any good if the growth is not sustainable. In this case, PFE’s free cash flow-based payout ratios have grown considerably in the past few years. This is a warning sign, that unless abated by future growth, throws significant warning signs for future growth in the dividend, but also sustainability of the dividend.

FinBox

PFE Future Valuation Analysis

Because we want our dividends to grow in the future, not just the past, we need confidence that the results the company has already achieved will likely continue, or in PFE’s case, that what looks like warning signs of degradation are not going to come to pass. We are looking for evidence that the drop in pricing and valuations is temporary, not an indication of a change in fortune.

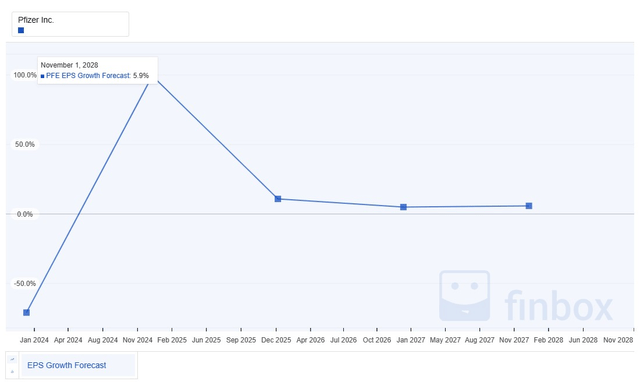

Looking at future Earnings Per Share projections, PFE is projected to have a bumpy ride, short term. A big downturn followed by a large upturn. Looking a little farther out to try to get a feel for the long-term growth, it seems like a mid-single digit estimate looks reasonable.

FinBox

Growth is one of the hardest things to predict in investing, otherwise, investing would be much simpler. Though we are thinking about the future in this section, I like to look at the history of growth forecasts to see how they align with the future predictions. The most recent predictions also show the bumpiness seen in the future, but zooming out, we get back to the mid-single digit growth that the future estimates predict.

FinBox

My own estimate for PFE’s forward growth is around 8%. I derive this from a combination of various growth projections and growth models. I personally feel like an average, mid-single digit growth expectation is reasonable for PFE.

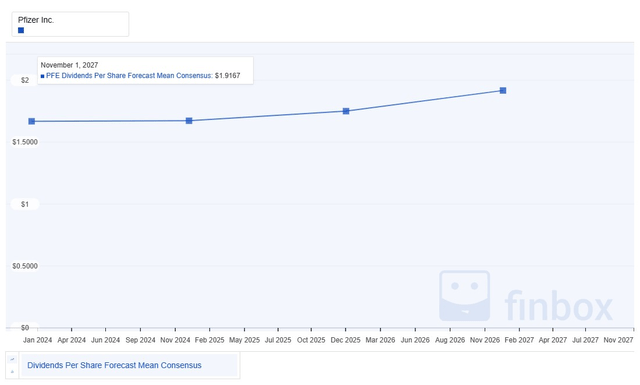

For a dividend growth investor, understanding future dividend growth potential is also important, especially in as much as it is sustainable. Here are the long-term dividend growth projections for PFE. It looks like the future growth is actually predicted to be higher than recent growth.

FinBox

To add to the comfort of the predicted future increases in dividends is the projected payout ratios, which do show PFE’s earnings-based payout ratios falling back to more comfortable, and historical levels. This adds credence to the idea that PFE may be valued more for the short-term than for the long-term, and could be an excellent dividend growth, and overall, investment at these levels.

FinBox

The projected growth in expected revenue is tied up in the above data, however, just to show it explicitly, the revenue growth projections for PFE do show consistent growth moving forward, and again, if accurate, suggest a sustainable, growing dividend with likely capital appreciation to boot.

FinBox

Pfizer Risk

Pfizer is a high-quality, company, which is coming off of COVID vaccine windfalls. As the discontinuity of that event fades away, the company that remains is still a very good one, maybe even better than before due to the debt improvements and R&D investments. The S&P credit rating of A+, Moody’s credit rating of A1, and A++ Value Line Financial Strength rating all attest to the quality of this company.

Just to state a few of the risks, Pfizer, like any biomedical company, has constant pressure on the pipeline, as well as the risks inherent to supplying new medicines to a patient population. One of the things that has attracted me to Pfizer is the risk and urgency that they showed in pursuing the initial COVID vaccines. Their CEO recognized the opportunity, and then pushed the company to do what many thought couldn’t be done. It’s one thing to talk about vision and strategy, and another to actually demonstrate success against significant challenge.

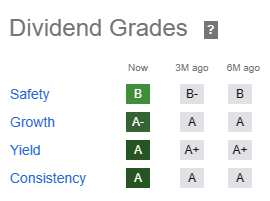

Obviously, with a dividend growth leaning personally, I also like further confirmation of what we’ve already established as far as dividend growth and sustainability are concerned, and Seeking Alpha’s Dividend Grades support solid dividend safety.

Seeking Alpha

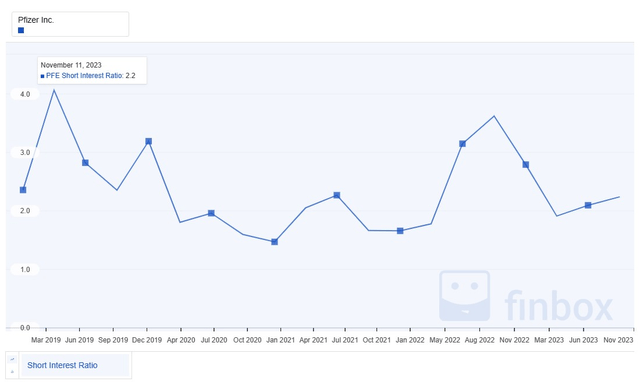

As a final check of risk, I like to look at short-term risk indicators for any new investments, with Short Interest being one key indicator for me that I might be missing something that others might know.

FinBox

Based on the low short interest, which is low compared to the 5-year average, I don’t see any short-term red flags that haven’t been discussed.

Summary

Pfizer feels a little more risky than some companies that appear to be trading at attractive valuations. On the one hand, the COVID vaccine windfall created some tremendous opportunities to reduce debt, and increase R&D, though the decreased growth in the dividend, and increasing number of shares outstanding begs the question of how much management believes in the sustainability of the benefits of this tailwind. Additionally, there is risk with some of the acquisitions and integration that Pfizer has in front of it. On the other hand, Pfizer did what many thought could not be done in bringing a new vaccine, and vaccine technology, to market in an amazingly short time.

Personally, I believe that at these levels, further investment in Pfizer makes sense. The initial dividend yield is high and appears to be sustainable. I like the risk / reward relative to bonds in this high interest rate environment. The dividend growth has been low, but it looks like there could be room to increase this in the future. The price is currently near COVID market downturn lows. Also, I want to believe that if management has proven capable of doing hard and novel things in the past, they have the capability to repeat the performance. Overall, from this analysis, I have convinced myself to put more of my money where my mouth is and add to my existing investments at these levels.

I appear to not be along in my assessment, as Seeking Alpha and Wallstreet also have Pfizer rated as a buy. As mentioned before, it is currently 5-star rated at Morningstar.

Seeking Alpha

As part of this analysis, we have also determined that Bristol-Myers Squibb, ResMed, and NextEra Energy are attractively valued from a Historical and Future Fair Value perspective. I have recently published an article on BMY here, that I believe is still relevant to help with further investigation.

Read the full article here