")

IBM’s AI Launch – CeBIT 2011 (yep 13 years back).

Face-to-Face with WATSON

Presenting an entirely new frontier in information science is IBM’s Watson advanced Q&A computing system, which recently proved its capabilities in understanding natural language in the US quiz show Jeopardy!. At CeBIT, visitors got a chance to challenge Watson in a demonstration game and learn more about the potential of the technology from the scientists involved. Watson’s ability to analyze the meaning and context of human language, and quickly process information to find precise answers can assist decision makers, such as physicians and nurses, to access important knowledge and facts buried within huge volumes of information, and offer answers they may not have considered to help validate their own ideas or hypotheses.

Source: IBM Research, Describing Watson’s AI abilities, From 2011

Guess we all missed that AI boom of 2011.

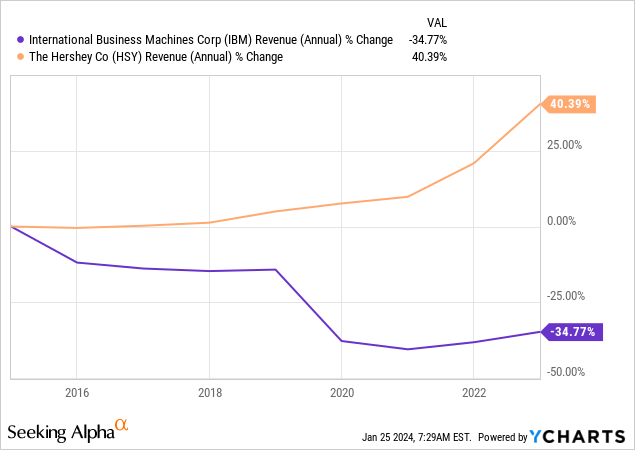

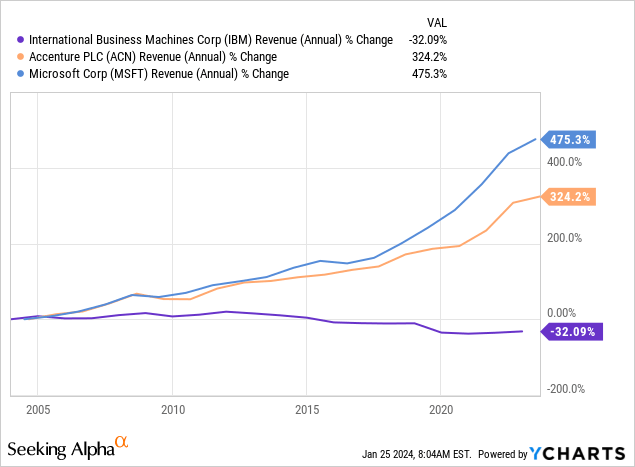

We have maintained a neutral view of International Business Machines Corporation (NYSE:IBM) (NEOE:IBM:CA) in the past. The stock had solid value characteristics, but those were offset by one of the most lackluster revenue trends for a technology company. If you did not know better, you might have confused which company was the one making chocolates and which one was the one in the sexy tech industry. At least if you looked at their revenues.

But this quarter gave the bulls some serious hope. We go over the results and tell you why this might be close to the top in this stock.

IBM Q4 2023 Results

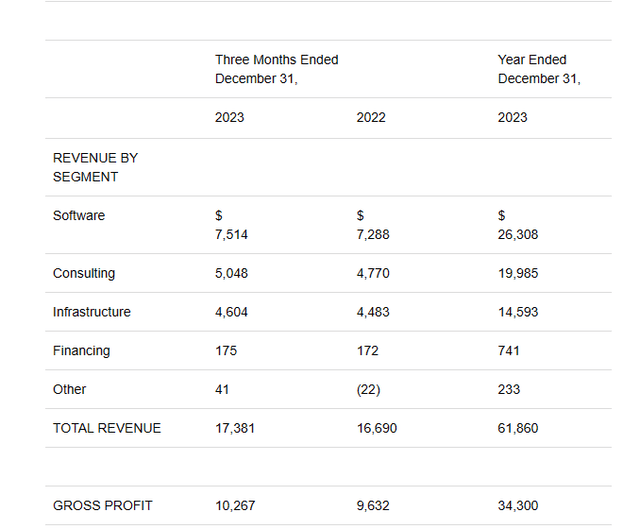

IBM’s Q4 2023 results were an impressive showing for the company, at least by its own standards. Sales were up to $17.4 billion, a 4% gain and 3% when adjusted for currency fluctuations. On a segment level breakdown, these were all trending in the same way.

Software revenue up 3 percent, up 2 percent at constant currency Consulting revenue up 6 percent, up 5 percent at constant currency Infrastructure revenue up 3 percent, up 2 percent at constant currency

Source: IBM Q4-2023 Press Release

With the AI boom firmly entrenched in every part of the economy, you would have expected overall revenues to at least move past the 12 months of CPI numbers. But they still came shy. Consulting is showing some life here but software at 2% (which as you can see, is the largest segment), is not very inspiring.

IBM Q4-2023 Press Release

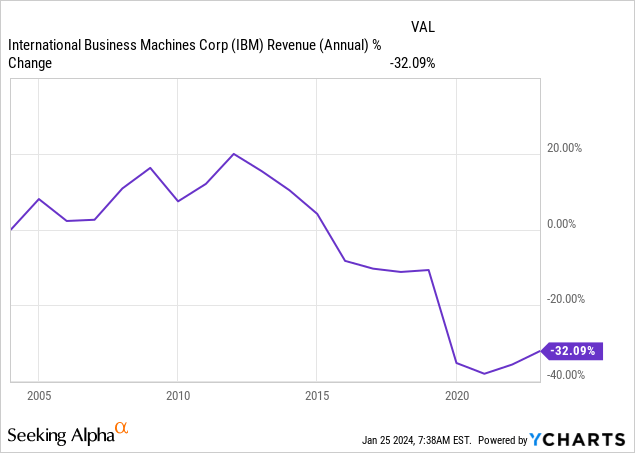

But there are some bright spots here for investors. The first being that IBM has successfully reduced the expectations for the company. If your two decade revenue trend looks like this, and that is after some heavy acquisitions, you should have the ability to beat expectations.

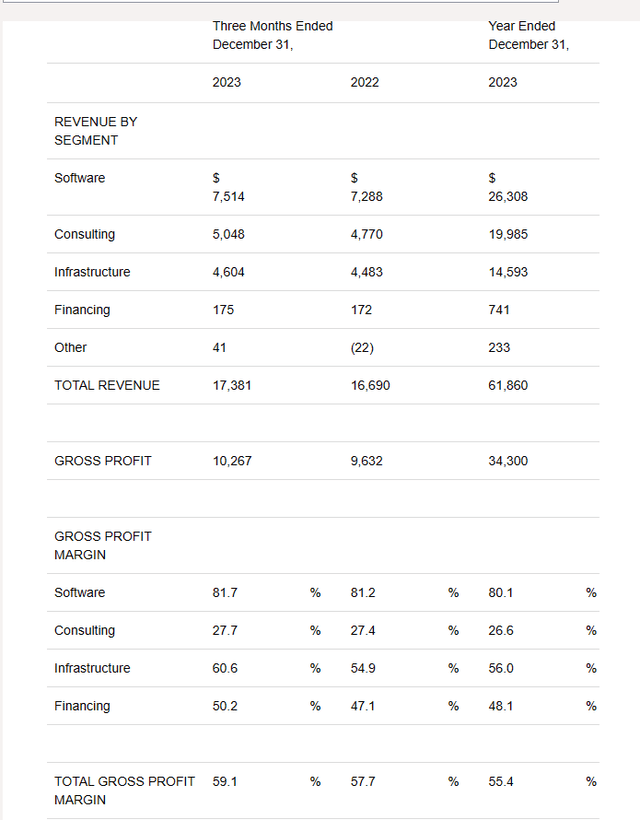

The company also did something rather remarkable, and that is expand its already large gross margins. Software margins, well yeah, those can expand easily with sales, but in consulting, it is tough to do so. Especially with high levels of competition for the right kind of workers.

IBM Q4-2023 Press Release

The same goes for infrastructure segment margins.

Free cash flow as also equally impressive, with a tally of $11.2 billion for the year.

Outlook

Just prior to the news release for IBM earnings, these were the earnings expectations for the company.

Seeking Alpha

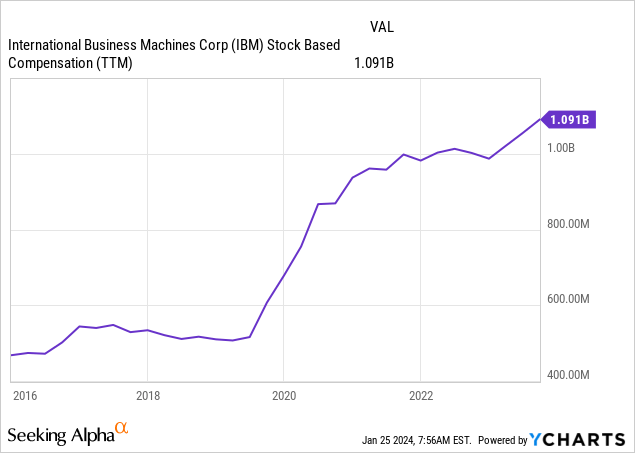

Modest would be the best way to describe it. IBM guided for mid-single digits revenue growth and a free cash flow of about $12.00 billion. Both those are modestly ahead of expectations and the stock is soaring as investors who missed the AI boom are trying to buy anything that’s already floating at 40,000 feet. But IBM is not really part of this boom. Sure, there is some general cyclical tailwinds here and revamping, redesigning or even installing new hardware, which likely brings IBM back into the equation. But it will be a tough landscape where cloud currently dominates and offerings are constantly being integrated into the primary product. IBM’s enterprise consulting will have it tough competing here and if the boom continues, retaining talent or at least retaining at current salaries will be hard. So far, stock based compensation has been modest, but it still bleeds at about 10% of free cash flow. It has been creeping up and likely accelerates even more in 2024.

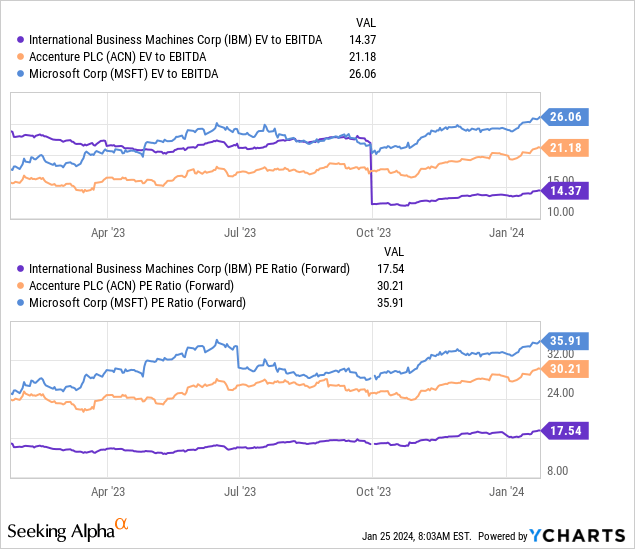

From a valuation standpoint, IBM is not particularly expensive, ringing in near 18X earnings when we discount the pre-market move. One other way to look at this is relative to the peer group. The problem is that there is no exact peer group as IBM’s business mix is unusual and also rather vulnerable compared to its peers. But let’s throw in a couple here to make the bulls happy.

Of course, there is a reason Microsoft (MSFT) and Accenture (ACN) have those multiples. See if you can get it from the next chart.

Perhaps the best argument you can make here is that IBM is fairly priced and the other stocks are vulnerable to any sort of slowdown.

Verdict

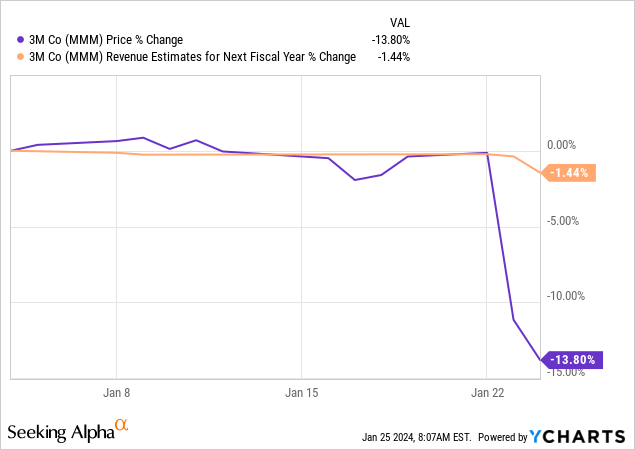

From a cyclical standpoint, you have to see the absolute bludgeoning we are seeing in some stocks. The lower guidance is coming on both the revenues and earnings. There is a strong argument to be made that the recession might be here already. Giant bellwethers like 3M Co (MMM) coming in even slightly lower on revenues are often indicative of GDP shortfalls.

Tesla Inc. (TSLA) another fan favorite, refused to provide guidance of how many cars it will actually sell in 2024. Management probably knows that a realistic number would create even more damage than the uncertainty. IBM’s great numbers are backward looking. The stock is now quite expensive on the metric that will matter most in the next 3 years, a price to sales figure.

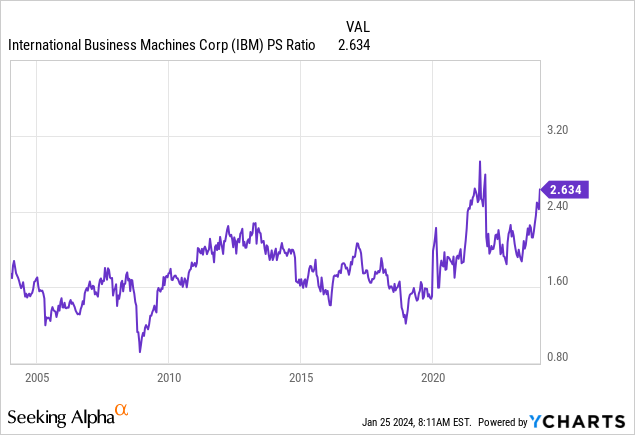

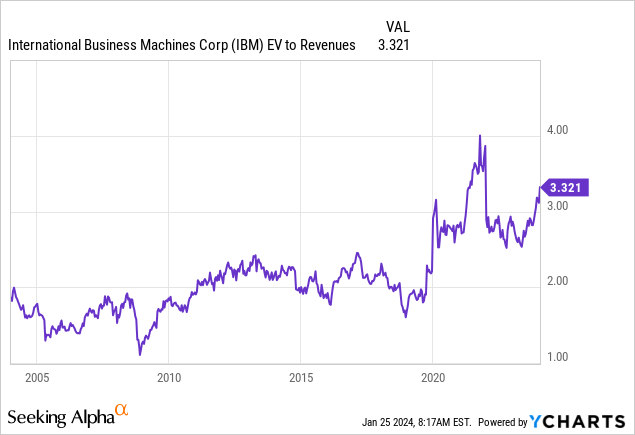

We will note that by this metric, IBM is more expensive than almost any other time in the last 20 years. On an enterprise value to sales basis (which adjusts for fluctuating debt loads), we see the same.

The only time when it was more expensive was when sales fell post COVID-19 and the stock rebounded back. At present, the odds of you making money here over the medium term look slim. The business is doing ok, but has long term structural headwinds. A push into the cloud will further challenge the stodgy business lines and AI will be margin compressing for IBM (and probably for MSFT and ACN) in the long term. With this euphoria in place on the results, we think the stock could run to the low $190’s and perhaps even eclipse $200. We would use the opportunity to sell.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Read the full article here