")

We believe the long-held status as a quasi-monopoly that helped Illumina have consistently high margins is about to end due to rising competition. There are several signs that the company will soon stop benefiting from the MOAT status it has benefited from, and the market is correctly pricing for this scenario.

On top of this, the company is currently being distracted by the recent governance turmoil and the GRAIL divestiture saga. This clearly leaves some dangerous room for newborn and existing competitors to take advantage of Illumina.

We think that a fair price should be in the $X-Y range and thus the current valuation is still too generous for a buying opportunity. For these reasons, our rating is a SELL.

Overview: Short v. long sequencing and where competition is coming from

Illumina (NASDAQ:ILMN) is the current global leader in DNA sequencing. They have developed a superb technology for Next-Generation Sequencing (NGS) that allowed them to quickly scale and gain significant market share. By 2014 they captured 70% of the total sequencing market and 90% of all genomics data. We believe this is still a factor behind their current generous valuation multiples of 42 times forward EBITDA and almost 4 times sales.

However, it is important to understand how the overall sequencing market is structured to spot the threats and understand Illumina’s position against them. The sequencing process can be divided into two main kinds: short and long. The former refers to the most common form of NGS that is now used and the most important for Illumina. It is called “short” because the line of genomic code is broken into smaller pieces of 50 to 300 bases before being sequenced. The former, on the other hand, is exactly the opposite. It is able to sequence the DNA or RNA in one go, without dividing it.

Let’s now visualize the competitors that Illumina is facing in these two segments:

-

MGI Tech competing in the short-sequencing

-

PacBio competing in the long-sequencing

MGI Tech is a Chinese firm with more than 2,000 employees that has been producing machines very similar to Illumina’s. The quality and the data formats are also compatible, making MGI a note-worthy competitor.

For a long time, Illumina was able to fend off competition by using its strong patents and the threat of lawsuits as a deterred. However, a recent loss in court against MGI itself may now pose a serious risk of competition. The Chinese competitor is now allowed to operate freely with no risk of lawsuits for 3 years, as per their settlement agreement with Illumina. But the patents in the case already expired, in December 2022 and January of this year, making any time limit effectively useless.

Let’s now look at the more interesting segment, long-read sequencing. Some of the most ambitious projects in the genome reading space are actually more focused on this approach. For example, the T2T project that aims to sequence all human chromosomes is using long-read sequencing. This means that the future fight for competition might take place in this segment rather than the already established short-reading one.

In this space we find PacBio. This is a very interesting competitor, and Illumina knows it too. Indeed, in 2018 they tried to buy them out in a $1.2 billion deal before the competition watchdog stepped in and blocked the transaction. This attempt is a good indicator that the technology behind PacBio is good and could pose a threat going forward. On top of this, given that the short-reading market was already dominated by Illumina, they decided to concentrate their efforts on building a new system that didn’t need to cut the DNA to read it, and works this way:

based on a very sophisticated optical system whose sensitivity allows the reading of a single molecule, and not of a mixture of short PCR (polymerase chain reaction)

All this seems quite scary considering that Illumina is already seeing some pressure on their margins and growth pace, but not everything is lost, of course. The company that long dominated the market has some cards to play left.

The strengths of Illumina’s MOAT: geopolitics and track record

There are two aspects that position Illumina with a strategic advantage against these two competitors: geopolitics and its reputation. Indeed, it is very easy to see the Chinese competitor being cut off from the US market in the foreseeable future. Genome reading is also about developing and deploying proprietary technology that covers a delicate field, and like TikTok and Huawei it can easily attract the suspicion of lawmakers. We believe that investors should be somewhat relieved by the fact that if MGI were to gain a substantial market share in the US market, authorities may step in a block any further expansion.

But there is also another important strength. Over the years Illumina built a great reputation as they invest a lot in post-sales services and consumables. This is clearly hard to replicate for any competitor as customers do not have a track record to rely on.

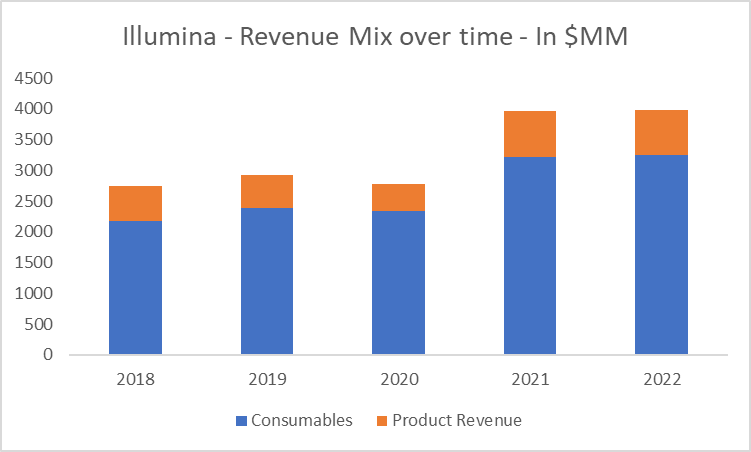

Revenue Mix (Seeking Alpha)

This chart perfectly shows Illumina’s revenue mix over the years. Consumables clearly represent the bulk of the company’s operations, while the sale of machines represents only a fraction. Past and future customers may feel more comfortable relying on Illumina’s consumables, meaning that a great percentage of the total market share is already “locked in” and will not go with competitors.

What everybody is focused on: internal turmoil and GRAIL

So, long story short, Illumina is definitely facing more competition now than in the past, but it has still a competitive advantage that could last years. However, the concerns are not limited to their business model. We believe that the ongoing governance turmoil and the GRAIL divestiture saga pose headwinds that take away much-needed attention from long-term planning.

Over the last year, the company clashed with the famous investor Carl Ichan over governance concerns. Eventually, the activist was able to change the CEO and is allegedly now suing the former executives and board members. Ichan sued under seal in Delaware, which means that proceedings are protected and cannot be accessed to protect confidential information. This adds unneeded layers of complexity to the governance turmoil, and investors lack visibility over the developments, which could include serious consequences if former managers were found to have acted improperly.

On top of this, there is the GRAIL divestiture. In October Illumina received the (expected) order from the European Union that ordered the divestiture of GRAIL. Illumina acquired the company in 2021 and closed the transaction without the pre-approval of anti-trust authorities. Now after two years, it is forced to divest its investment because it is against competition regulations. Luckily for them, the regulators gave much flexibility to close the transaction, with the following terms: (1) 12 months with a 3-month extension as the deadline, and (2) could be a sale to a third party or a capital markets transaction. This means it could also be resolved in a spin-off with Illumina distributing the shares to investors and allowing GRAIL to go on as an independent entity.

This poses two major downsides: (1) Illumina is forced to conclude this transaction in a very unfavorable valuation environment, and it may underestimate the fair value of GRAIL, and (2) it distracts the company from its core business activities and plans.

When evaluating a large company, it is essential for the market to have clear visibility of each segment, their contributions, and growth rates. It is hard for them now to put a value on the entire company without knowing what will be on the GRAIL activities 12 months from now. A spin-off or an M&A transaction would carry different multiples. So this also weighs on the current valuation and will continue to do so until it’s completely resolved.

Valuation: weighing concerns and strengths to find out Illumina’s fair price

It’s now time to put everything together, concerns and strengths, to come up with a fair value per share. It is a tough task, as the company itself is unique and it is hard to see into this peculiar market 10 years from now, but it’s essential to decide whether the current price is overvalued.

We will use a standard DCF model that goes as far as 10 years to better capture the competition concerns. We will also try to include the GRAIL’s valuation by forecasting revenues and contribution that stops at the end of the 10 years, with no terminal value associated with it. This is because the segment will soon not be part of Illumina anymore.

The assumptions of our model are the following:

-

Generous revenue growth rate of 10% per year for the entire reference period. This is to reflect a continued relevant position in a fast-growing market that is seeing significant interest.

-

EBITDA margins slowly normalize in the 30-32% range between 2023 and 2026, to later see a contraction back in the 29%-30% range to reflect competitive forces joining the market.

-

Capex is stable at roughly 4-5% of revenues over the years. This is well aligned with past investments and an overall stable yearly contribution to keep their infrastructure alive and well.

We believe these are more than fair and sound assumptions. Indeed, we think there is even some optimism embedded in the EBITDA margin forecasts that we made, and this provides an additional margin of safety to our thesis.

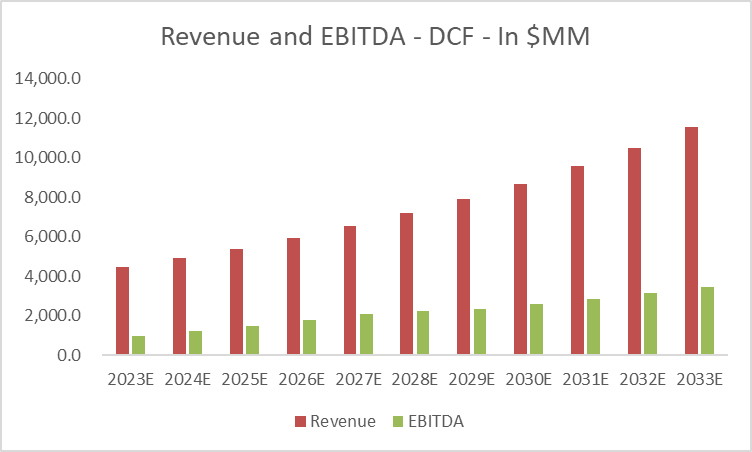

The outcome of our analysis is the following:

Revenue and EBITDA – DCF Model (Author’s DCF Model)

Forecasted revenues and EBITDA are growing very rapidly and quickly reach the $10 billion and $3 billion levels by 2032. This also translates into unlevered FCF consistently above $1 billion after 2026. However, the final outcome is a mere fair EV of around $14.5 billion, which after deducting the roughly $750 million in net debt becomes a fair value per share of around $85. This represents an overvaluation of around 23% from the current price of more than $110.

We believe that an investment in Illumina below this level would make little sense as the market is still struggling to fully price in lower terminal revenue growth and lower margin expansion for the longer term.

Conclusion

Illumina is a great company that was able to develop superb technology and quickly become a leader in a large and growing market. However, after years of unchallenged dominance and fast-growing revenues and profits, various issues seem to have recently lined up at Illumina. Competitors quickly entering the market, governance turmoils, and regulators forcing divestitures make the company a much less attractive investment. We believe that a fair price per share should be lower than $85, and thus the current market valuation is still too generous.

Read the full article here