")

2023 Recap

I’m going to broadly review what has happened to Stereotaxis (NYSE:STXS) since my last article in February.

The biggest news was in the summer when the EU regulators asked the company for a human trial before giving the Magic catheter a CE Mark. This was very disheartening for long term investors because there was a delay in getting to the submission in the first place. EU regulators changed what they were looking for at the last second.

It’s not frustrating that Stereotaxis has to do a human trial. It’s frustrating that this was determined 6 months after the completeness check. Regulators said the application was complete and then changed their mind. This is consistent with the broader trend of the EU’s MDR making the regulatory environment much tougher. Luckily, the exact opposite is happening in the US, which I will detail later in this article. This human trial requirement effectively caused a 1-year approval delay even though the actual trial will only take a few weeks. I’ll detail this process in the product timelines section.

Secondly, Stereotaxis announced a partnership with Abbott (ABT) where Stereotaxis’ robots would be compatible with Abbott’s Ensite X 3D cardiac mapping software. Since then, it has been used in the EU and the US. Stereotaxis’ ethos is about having the best tools available to electrophysiologists. They call it Open EP. There’s basically a duopoly in mapping software. The other is J&J’s (JNJ) CARTO. Abbott has slightly less share than J&J.

Abbott is deepening its strategic partnership with Stereotaxis, while J&J (Biosense Webster) is moving away from Stereotaxis. Abbott sponsored the SCRN conference, jointly announced the Ensite X integration with Stereotaxis at the HRS conference, and demonstrated the integration at the SCRN conference. J&J won’t be producing the current magnetic catheter in 2 years. This is fine because Magic will replace the old J&J catheter. I like mentioning trends because it helps predict the future. I expect the ties with Abbott to tighten and ties with J&J to weaken.

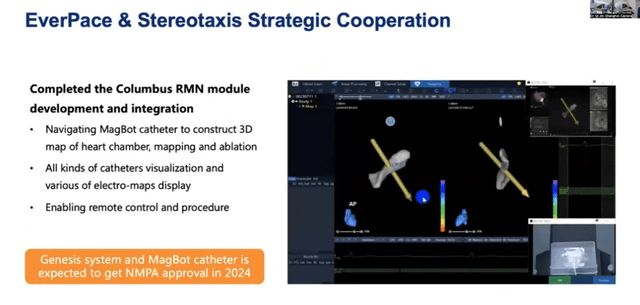

EverPace (OTCPK:MCRPF) (formerly MicroPort EP) in China is leaning heavily into robotics. EverPace is Stereotaxis’ partner in China. They have their own catheter that works with Genesis & Niobe. All of the robots in China are the original robot, Niobe, because Genesis hasn’t been approved. As you can see below, they call it MagBot. Stereotaxis will get a royalty on that catheter which should get NMPA approval in mid-2024. The EverPace Columbus 3D mapping software has been successfully integrated with Stereotaxis’ robots.

Source: EverPace Presentation

Acutus (AFIB) was one of Stereotaxis’ catheter partners. They did an animal study on a magnetic PFA catheter. Acutus had been leaning away from robotics, because of its financial issues. Now we have found out they are leaving EP entirely which is sad to see because their catheters were effective. It’s difficult to compete with bigger players. Stereotaxis’ Magic catheter will be successful because it will be sold to EPs who use Stereotaxis robots already.

Finally, during the March conference call, Stereotaxis pushed back the timelines for all new products by about 6 months. There have been modest slides in some product timelines since. I’ll get into the details of each timeline later in which I will include my current confidence level for each product getting done on time. I just wanted to take responsibility for having too much optimism on new product timelines in my February article.

Overall, Genesis installations have restarted in 2023 after almost nothing was getting done in 2022 due to construction delays. On the negative side, new robot orders have been disappointing because aging X-ray machines haven’t led to replacement cycle orders quickly enough (likely mid-single digit orders in 2023 | we want low double digits per year). X-ray machines being replaced catalyze a robot replacement since the X-ray is bundled with Genesis. However, instead of being replaced after 10 years, they are lasting 12-15 years without a change. On a positive note, I think Genesis orders will pick up in China once it’s approved there next early year.

I think Stereotaxis will do $30.5 million in 2023 sales which is 8.3% growth. That disappointment stems from the Magic catheter delay. That additional $3k of high margin revenue per procedure wasn’t there. Magic’s approval would have increased system demand in my opinion. Despite excitement from Chinese hospitals, an anti-corruption budget freeze starting in July pushed back system orders.

The firm expects to end 2023 with $22 million in cash. That’s plenty of cash if you assume the Magic catheter approval helps the company get to at least cash flow breakeven by Q4 2024. The firm has been burning about $1 million per quarter recently. Even if it burns $2 million per quarter in the first 3 quarters of next year, it’ll be fine.

7th SCRN Recap

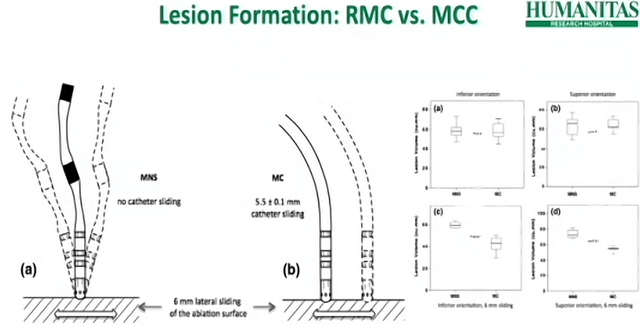

SCRN is the Society for Cardiac Robotic Navigation’s annual meeting. This conference in October was the 7th one. It’s a critical organization because this is EPs themselves presenting their findings, not Stereotaxis. It’s amazing to have because Stereotaxis needs champions to push demand for robotics forward. I spoke with an EP who uses Stereotaxis on Twitter (he wasn’t at SCRN). He said “if you want a tattoo, do you go to one that says “hey move all you want” or do you go to one that says you can move but I have a machine that moves with you.” I screenshot a slide from one of the SCRN presentations that illustrates the safety and precision of robotic magnetic navigation. The lesions are much cleaner and the risk of perforating the heart is eliminated because the catheter is soft like spaghetti.

Source: SCRN Presentation

This was my first SCRN, but I’m already very familiar with the main champions of robotics. Broadly speaking, we are going to need to grow this group considerably. That’s the goal of the semi-mobile robot which is much more affordable for hospitals. It will be installed in a weekend which is much better than Genesis which requires the EP lab to be shut down for 6 months and over $1 million in construction expenses. Furthermore, because the Genesis is a fixed device, hospitals need to pay for it up front. The semi-mobile robot will be leased.

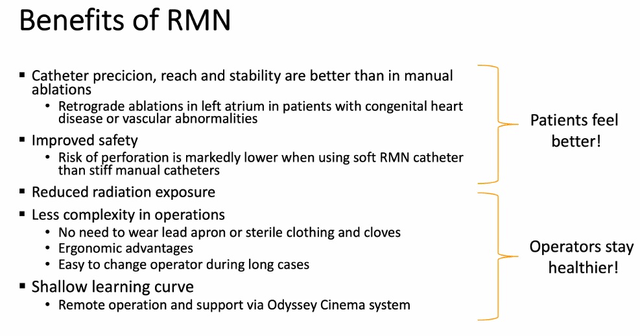

Clearly, EPs need to be convinced of the benefits of robotics too. However, the main case against robotics is cost. Without this issue, sentiment will be more positive. There are robot EP fellows who would be the first to ask for an accessible robot to start the semi-mobile sales cycle. Increased sales will snowball, changing EP’s minds. There were 2 debates at the conference over whether robotics should be used in all Pediatric/ACHD & left sided PVC patients. The slide below shows a summary of the benefits of robotics.

Source: SCRN Presentation

A randomized prospective study of ventricular tachycardia treated with robotics vs. manual with 180 patients is coming out early next year. One challenge with doing these studies is robot users don’t want to use manual devices. I’m interested in seeing future results of studies with the Magic catheter. We’ve seen enough data on robotics in my opinion. 150,000 procedures have been done with Niobe and Genesis. It’s time to see results with the Magic catheter instead of one that was designed about 2 decades ago. Remember, Magic is easier to control. Management said it’s like going from to manual to power steering.

I got the idea that the EU is becoming stricter via MDR and the FDA is getting more lenient when working with med tech firms from Myriam Curet’s SCRN presentation. Myriam Curet, a Stereotaxis board member and the Chief Medical Officer of Intuitive Surgical (ISRG), said when she joined the Stereotaxis board it had a great relationship with the FDA. These points about the FDA led to the fast-tracked Magic catheter FDA approval process that I will discuss in the next section.

Dimitri Sigounas is one of the neurosurgeons who went to Stereotaxis’ HQ late last year to test the magnetic guidewire. He presented his findings at SCRN. He said magnetic robots could be used for brain computer interface (BCI) because of the precision magnetics provide. He’s optimistic about the guidewire’s prospects in neuro. That’s probably the indication with the most near term promise because of the brain’s complex vasculature.

Updated New Product Timelines

Now I will review the updated timelines of each new product in each region. This is mostly about regulatory submissions and approvals.

The EU regulators decided the Magic catheter needed to go through a human trial after they asked all their questions and reviewed the submission. The human trial needs to be 20 patients and requires acute data which means it can be submitted right after the procedures are done. Stereotaxis got 3 hospitals on board to go through this process. They have experience with both the robot and human trials. The human trials will start sometime in the next few weeks (mid-November to mid-December).

Getting to 20 patients will only take 2-3 weeks. Stereotaxis can get data from up to 30 patients per hospital which is 60 in total. The firm can also do a follow-up study. Stereotaxis will then submit the data in Q1. I think the review process will be quick because regulators already reviewed the submission. They just need to review one study. I expect it to be approved in May and my range of expected outcomes is April to September. I’m hoping Stereotaxis does a press release after the study is completed successfully in December, but I have no idea if management will do that.

I’m confident the human study will go well because Magic worked in animal studies. Drugs tested on animals obviously can have different results on humans, but when it comes to a physical endovascular device what you see in animals is what you will get in humans. Both have veins/arteries and a beating heart. I specifically spoke with a medical officer in pediatric and congenital cardiac surgery about this, so I’m not talking off the cuff. Stereotaxis tried to perforate the pig heart in animal trials and couldn’t because the catheter is so soft. It’s extremely safe.

After Magic gets CE Mark, there needs to be a tender to get it approved in France and the Scandinavian countries. This is paperwork that will limit how much it can be used in those areas for 6-12 months. I think Magic will get approved in China about 6 months after the CE Mark. It’s a faster process when the CE Mark is in hand. It’s also notable that Genesis will finally be approved in China in Q1 2024. Genesis, Stereotaxis’ latest generation magnetic robot, has been in use in the US & the EU since late 2020, hitting 1,000 total procedures in April 2023.

The FDA approval of Magic will go through a fast-tracked PMA submission. Stereotaxis will submit the PMA in December. The EU human trial will add enhanced data to the submission. A decision will be made 180 days after the submission. This fast-tracked process is hugely positive because we thought a 2-year trial was necessary. After speaking with regulators, Stereotaxis decided a PMA was the best approach. The FDA has worked well with med tech firms in recent years. The EU regulatory framework used to be easier than America’s before MDR, but the positions have switched.

The guidewire will be submitted via a 510-K in America and a similar regulatory process in the EU in Q2. That’s a full 2 years after it was originally expected to be submitted. Obviously, that calls into question the current timeline. However, I’m confident this one will be hit because the technical challenges that caused inconsistent quality have been overcome finally.

On the call, David said,

“That development process has not been easy as our contract manufacturer faced various challenges in transitioning from building good prototypes to being able to actually build devices with a quality, consistency and scale that would be necessary for regulatory approval and commercialization. We seem to have overcome the last challenge in that manufacturing process and expect to spend the next few months building the over 1000 guide wires needed for formal regulatory testing.”

This reminds me of early 2022 when the final manufacturing hurdles were overcome for Magic following a year long delay. It ended up being submitted to regulators a few months later in the summer. I’m confident the same will happen with the guidewire next spring.

The regulatory process for the guidewire is less onerous than for Magic because it is a guidance device that isn’t delivering care like a catheter ablation. It should get approved within a few months of submission in both the US and the EU. After the guidewire is submitted to regulators, Stereotaxis will host an innovation day to show off the indications it can be used on. The event will probably be early next summer. In subsequent years, Stereotaxis will create a family of guidance devices that include guidewires, guidecatheters, and microcatheters.

The semi-mobile robot will be submitted to the FDA via a 510-K and EU regulators in a similar fashion in Q1. It will likely get approved within a couple months in the EU and 6 months in America if it goes by the same timeframe as Genesis in 2019/2020. David presented the semi-mobile robot for the first time at SCRN a few weeks ago.

The device has been ready for submission for a few months, but it has been held back by the company until either the guidewire or Magic are close to approval. It needs to launch with an interventional device because it can’t be used without them. Marketing 101 says don’t launch a product buyers can’t actually use. Since Magic should be approved in the EU and America by mid-2024, we are approaching the time for Stereotaxis to pull the trigger on the semi-mobile submission.

Synchrony is the display and computer system that can be sold with a robot and separately as capital equipment. This is the next generation after Odyssey. David highlighted how much thinner the fiber cables are in his SCRN presentation. The computer box looks like a desktop tower that fits under a desk. The Odyssey takes up an entire room and requires underfloor thick fiber cables. Synchrony can be plugged into a regular outlet.

Synchrony is the hardware part of David’s ‘digital surgery’ plan. Surgery data can be organized for better automation. Synchrony & Odyssey can also be used for telerobotic surgeries. I expect Synchrony to be ready around a few months after the semi-mobile robot is approved. No timeline was given on the Q3 call. I’ll say it’s coming in 2H 2024 based on previous guidance in relation to the semi-mobile submission.

Synx is the software part of David’s ‘digital surgery’ thesis. It is the mobile smartphone app Stereotaxis is working on that allows doctors to communicate. It will have a SAAS business model. It’s currently being tested in-house. No specific timeline was given on an official launch. It will probably launch once the semi-mobile robot starts to hits its stride with orders. Stereotaxis needs a large network of robotic users to make it work. Maybe the firm will start with outside beta testers in 1H 2024 and officially launch in 2H.

What About The Stock?

Sentiment on Stereotaxis is quite poor. Even investors are expecting more delays. Imagine what outsiders think. Sure, we’ve had insider buying in August/September from a director, but we need the first regulatory approval win for an uptrend to start. That’ll likely come late in the spring when Magic gets CE Mark. The mobile robot submission in Q1 also could help the stock since it’s very likely to get approved. A presser in late-December saying the Magic human trial went well would be nice.

I have a large position. My average price is $2.17. I’m hoping when I look at the stock on April 27th, 2024 (3 year anniversary of my first purchase) my position is in the black. I have a 5 year time horizon, but there are steps next year that need to be hit for me to remain bullish.

Risks

The entirety of Stereotaxis’ valuation is in the new products that either haven’t been approved or haven’t even been submitted to regulators. I say that because Genesis isn’t profitable without the Magic catheter. Plus, J&J won’t make its catheter after 2025. Stereotaxis could get acquired if the business can’t get over the final regulatory humps, but it won’t be for a large premium since the business will be losing money. The balance sheet would become a problem if Stereotaxis couldn’t get either the CE Mark or FDA approval of the Magic catheter within the next 2 years because it is burning about $1 million per quarter.

Conclusion

I’m bullish on Stereotaxis stock because I believe the firm will achieve accelerating revenue growth via its new high margin interventional devices (catheter, guidewire, guidecatheter, microcatheter) in the next few years. Furthermore, the financially accessible semi-mobile robot will expand the user base for interventional recurring sales to come from.

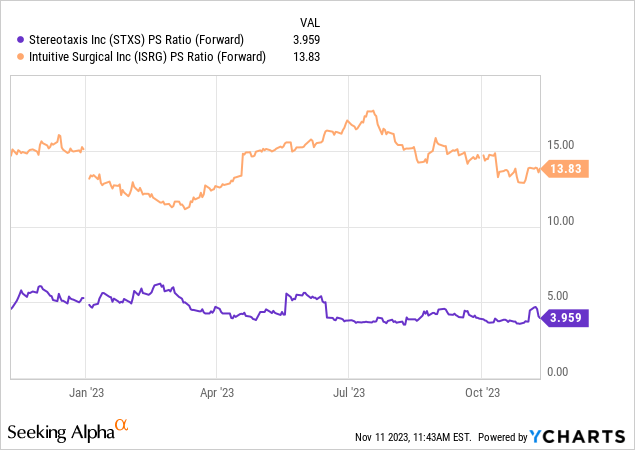

The approvals & launches of its new products in 2024 will catalyze multiple expansion. As you can see below, Stereotaxis only trades at 4x forward sales, compared to Intuitive Surgical’s 13.8x multiple. Stereotaxis has much higher growth potential, but investors won’t reward it with a premium multiple until their products launch. Since I’m confident they will, I’m long the stock.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here