")

IQVIA (NYSE:IQV) provides a broad range of services to biopharma customers, with the majority of the company’s revenue coming from outsourced R&D related to clinical trials. IQVIA has faced modest headwinds recently due to both spending caution by customers and the end of COVID related revenue. Given current financial conditions and the behavior of biopharma companies, it seems reasonable that soft conditions will persist for some time. It is also possible that the recent reduction in R&D will hit the number of drugs entering clinical trials at some point.

Looking further ahead, AI-enabled drug discovery programs are gaining pace and could lead to a revitalization of biopharma R&D in coming decades. While IQVIA is somewhat of a distant play on this theme, only modest growth is currently priced into the stock, meaning a significant growth acceleration could cause the stock to rerate substantially.

Market

IQVIA breaks its addressable market into several opportunities:

- Outsourced R&D – Biopharma drug development spending totaled roughly $184 billion in 2023, with clinical development spending amounting to $99 billion. Approximately $50 billion of this was outsourced.

- Real-World Evidence and Connected Health – Life sciences TAM of approximately $30 billion, including post-launch evidence generation, market access and medical affairs. Healthcare TAM of approximately $40 billion, including revenue cycle management, payer and provider analytics and clinical decision support services.

- Technology Enabled Commercial Operations – TAM of roughly $80 billion across IT and commercial services (salesforce recruitment and training, market access consulting, brand communication, etc.).

IQVIA’s business is likely to face a dynamic demand environment in coming years, in large part due to declining industry R&D efficiency and the rise of precision medicines. Biopharma companies need to find ways to bring drugs to market faster and at a lower cost, with AI potentially providing a solution. IQVIA’s business could also be supported by a growing need to understand epidemiological and physiological differences in different ethnic populations and increased demand for local clinical trials in some geographies.

The imminent pharmaceutical patent cliff has also been posited as a potential tailwind, although this is likely to be a fairly complex issue. Some top selling products will lose their protection by the end of the decade, with more than $200 billion in annual revenue at risk. Many of these are biologic products though and may not be easily substitutable. Larger biopharma companies have significant cash on hand which can be directed toward acquisitions and R&D, while other companies may come under financial strain.

The rapid rise in interest rates in 2022 caused many biopharma companies to cut back on spending. While this is having a direct negative impact on IQVIA’s business, there could also be secondary effects later on. A lack of pre-clinical research and a reluctance to take riskier assets into clinical trials could see fewer clinical trials and less new drugs entering the market in the future. IQVIA doesn’t seem to think that this will be the case though, with the IQVIA Institute estimating that around 350 new molecular entities will be approved between 2024 and 2028, a modest increase in approval rate compared to the past decade.

From a competition perspective, IQVIA appears to be operating in a fairly mature market with established competitive dynamics. IQVIA faces a broad range of competitors across its segments, including:

- Technology & Analytics Solutions – Accenture, Cognizant, Fortrea, Deloitte, Pharmaceutical Product Development, Infosys, McKinsey, NielsenIQ, Paraxel, ICON, Cegedim, Medidata and Veeva.

- Research & Development Solutions – ICON, Paraxel, Pharmaceutical Product Development, Syneos Health and Fortrea.

- Contract Sales & Medical Solutions – Syneos Health, Amplify Health, Eversana and Inizio.

IQVIA also faces competition from the in-house capabilities of customers, which could present an opportunity in the future. A number of factors are making it difficult for biopharma customers to be both vertically integrated and at the cutting edge of science and technology. This situation could eventually lead to fragmentation of the supply chain, with more services being outsourced so that biopharma companies can benefit from increased specialization and economies of scale.

IQVIA has suggested that the demand environment for its industry continues to be favorable, although strength varies across segments. Demand from IQVIA’s R&DS clients is solid, with the company’s backlog growing at a healthy pace. Quarterly RFP flow was up 6% YoY in the first quarter, and IQVIA’s qualified pipeline increased double digits versus the prior year.

While this is positive, financial conditions are tight and the macro environment remains uncertain, and customers are cautious as a result. This is negatively impacting Technology & Analytics Solutions, with many large pharma companies having introduced cost reduction programs.

IQVIA

IQVIA is a leading global provider of advanced analytics, technology solutions, and clinical research services to the life sciences industry. It is one of the largest players in its markets, generating approximately $15 billion revenue in 2023, with around 87,000 employees across more than 100 countries. Most of these employees fall under the company’s Research & Development Solutions segment, which is also the company’s primary source of revenue.

IQVIA segments its business into:

- Technology & Analytics Solutions – primarily services around data and IT

- Research & Development Solutions – CRO

- Contract Sales & Medical Solutions – sales and marketing support

Technology & Analytics Solutions include:

- Technology Platforms – SaaS solutions supporting a range of commercial and clinical processes (CRM, compliance and safety reporting, marketing, etc.). Technology platforms also includes IQVIA’s Global Market Insight offerings.

- Real World Solutions – help customers to generate and disseminate evidence related to safety, effectiveness and value. Privacy and data security are critical to this part of the business given its nature. IQVIA Health Data Catalog provides access to over 3,400 real world data assets.

- Analytics and Consulting Services – consulting services that assist the commercial operations of customers. IQVIA also helps R&D teams address challenges in the drug development process.

- Information Offerings – Data related to product sales, prescribing trends and medical treatments.

Research & Development Solutions include:

- Project Management and Clinical Monitoring – supports clinical trials (generally phase II-IV). Services include protocol design, site start up, patient recruitment and site monitoring.

- Clinical Trial Support Services – expertise to help customers collect, analyze and report data that supports regulatory approval.

- Laboratory Services – end-to-end clinical trial laboratory and research services.

- Strategic Planning and Design – consultation services leveraging data science capabilities.

- Patient and Site Centric Solutions – technology and support services that help to engage and retain patients.

Contract Sales & Medical Solutions:

- Health Care Provider Engagement Services – develop and deploy stakeholder engagement solutions which are focused on driving sales and brand value.

- Patient Engagement Services – Helps patients to improve their disease and medication understanding and navigate reimbursement coverage issues.

- Medical Affairs Services – Helps customers to plan and transition from clinical trials to commercialization.

The AI Opportunity

IQVIA has a number of AI related opportunities, both directly from AI increasing the value of data and indirectly from AI potentially increasing the flow of drug candidates entering clinical trials and ultimately the market.

While AI is an opportunity, IQVIA has suggested that it could be more limited in healthcare than many people expect as data is often scarce, particularly publicly available data. IQVIA has stated that the Quintiles and IMS merger was specifically to create large data sets that could be leveraged with analytics to accelerate clinical development times. This is particularly applicable to oncology, rare diseases and difficult to enroll patients. Related to this, Recursion has suggested that AI could make it feasible for companies to develop drugs for small patient populations. IQVIA would likely benefit as companies try to recruit and market to these patients.

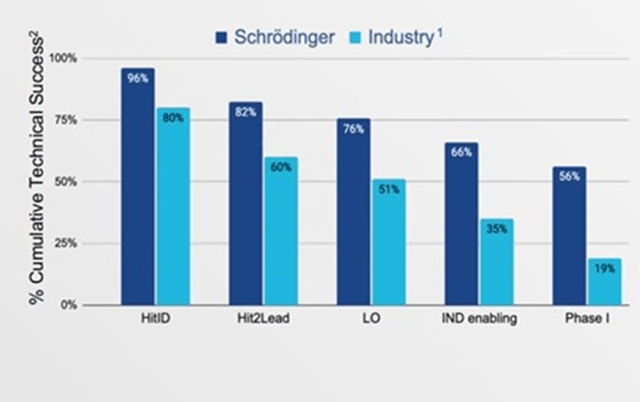

If initial data is indicative, AI driven drug discovery could lead to a substantial increase in the number of drugs entering phase II/III clinical trials, which could provide IQVIA’s business with an unanticipated boost. Analysis by BCG shows that AI-native companies have entered 75 molecules into clinical trials since 2015. At the end of 2023, 24 of these molecules had completed phase I trials with an 80-90% success rate, which is substantially higher than the industry average of 40-60%.

If nothing else, the number of AI-discovered drug candidates entering clinical trials is rapidly increasing. At this point AI-discovered molecules are not meaningful to total clinical trial numbers, but if the current trend continues, this will change in the next few years. For example, IQVIA has stated that at any given point in time, it is working on around 2,500 clinical trials.

The increase in drug candidates is likely to come about for a number of reasons, including:

- Increased R&D productivity

- Ability to explore greater molecular diversity

- Improved chances of clinical success

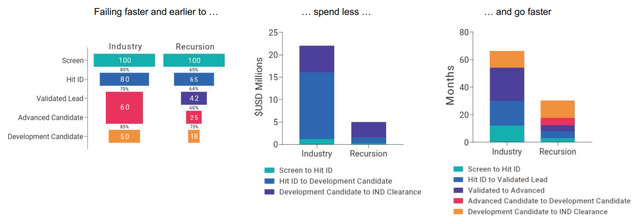

While it is too early to say definitively, most drug discovery companies leveraging AI believe that they are able to advance candidates to clinical trials faster and at a lower cost than the industry average. Exscientia believes that its efficiency increases the NPV of its projects 4x compared to the industry average. Absci is targeting two years to IND versus 4-6 year industry average and expects to spend $14-$16 million to reach IND versus the $30-$50 million industry average.

Figure 1: Schrodinger’s Cumulative Portfolio Success (source: Schrodinger)

Figure 2: Impact of Recursion’s Approach (source: Recursion)

Financial Analysis

IQVIA’s revenue increased 2.3% YoY in the first quarter of 2024 to $3.737 billion, or 6% adjusted for the impact of foreign exchange and COVID related work. Acquisitions contributed approximately 1% to growth.

Technology & Analytics Solutions revenue in Q1 totaled $1.453 billion, up 0.6% YoY. This part of the business continues to be negatively impacted by the demand environment. A modest increase in activity is expected later this year though, which should support growth. R&D Solutions first quarter revenue was $2.095 billion, an increase of 3.4% YoY. R&D Solutions backlog was up nearly 8% YoY $30.1 billion and next 12 months revenue from backlog grew 6.1% to $7.7 billion. IQVIA has also been hit by the cancellation of a large central nervous system trial. A typical cancellation would be in the $15-$20 million range, but this one was around $250 million. Contract Sales and Medical Solutions first quarter revenue increased 3.8% YoY to $189 million.

Table 1: IQVIA Q1 2024 Revenue by Segment (source: Created by author using data from IQVIA)

IQVIA is currently guiding to $3.740-$3.815 billion revenue in the second quarter. For the full year, IQVIA expects $15.325-$15.575 billion revenue, representing 2.3-3.9% YoY revenue growth. Revenue growth is expected to improve later in the year as the reduction in COVID related work is weighted towards the first half of 2024. IQVIA also expects TAS revenue growth to pick up in the second half of the year.

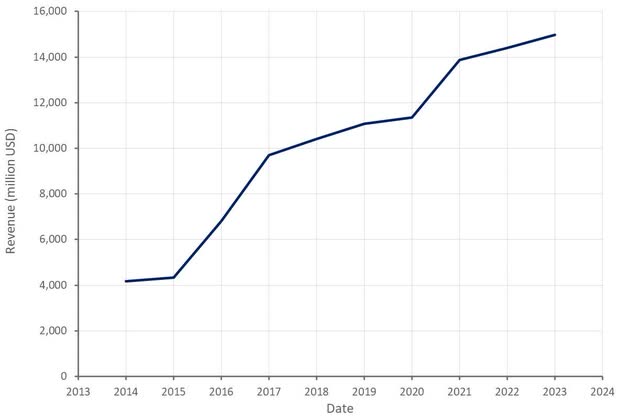

Figure 3: IQVIA Revenue (source: Created by author using data from IQVIA)

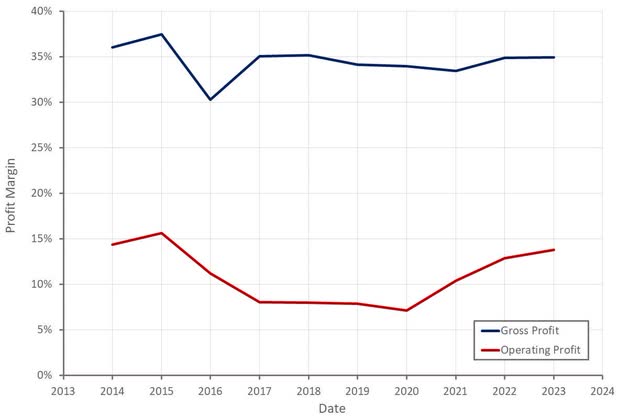

IQVIA’s profits were fairly flat YoY in Q1. Adjusted EBITDA increased 1.3% YoY to $862 million, while GAAP net income was down 0.3% to $288 million. The company’s profit margins have rebounded significantly over the past three years though and could move higher due to a combination of revenue mix, operating leverage and cost control.

Figure 4: IQVIA Profit Margins (source: Created by author using data from IQVIA)

It should be noted that IQVIA currently has a net debt position of approximately $12.1 billion, and its net leverage in Q1 was 3.38x TTM adjusted EBITDA. While this isn’t necessarily a problem, it probably limits IQVIA’s ability to engage in further large-scale M&A and means that interest expenses are currently consuming a substantial portion of profits.

Conclusion

IQVIA’s valuation is fairly modest, which reflects expectations of low single digit revenue growth and a modest improvement in profit margins. As a result, there could be meaningful upside if IQVIA’s growth is more robust than anticipated.

If the AI driven drug discovery lives up to expectations, the number of drug candidates entering clinical trials could accelerate in coming years, boosting IQVIA’s Research & Development Solutions business. While I think this could be an interesting AI theme at the right time, IQVIA probably won’t see any real benefit for several years, and in the meantime faces a sluggish demand environment.

Figure 5: IQVIA EV/S Ratio (source: Seeking Alpha)

Read the full article here