An Established, Old Firm with New CEO

Rounding out my series of articles this week on the financials sector, today I went diving into the waters of investment banking again in search of a stock for under $40 in this sector, and I came across a long-established firm called Lazard (NYSE:LAZ), which recently had its latest earnings results announced on Feb. 1st.

Some key points that set this firm apart, from its SA profile, are that it has been in business since 1848, is diversified across multiple business segments including financial advisory and asset management, as well as wealth management.

The major news they had in 2023 was naming new CEO Peter Orszag, who took the helm this fall, and had previously been head of the financial advisory practice.

So far today on Seeking Alpha, from the stock’s profile, the consensus on this stock is a hold consensus from SA analysts and the quant system, while the Wall Street consensus is a buy, a mixed bag.

Investment Thesis: Buy

My investment thesis today calls for a buy on this stock.

The supporting evidence why it presents a buy today is that the stock has a +5% dividend yield which is higher than several key peers, recent YoY revenue and earnings growth in Q4, has significant future EPS growth expected driven by investment banking and M&A surge, and a low risk profile in terms of company debt. I also consider it fairly valued at the current share price.

In addition, what gives this firm a competitive advantage in their space is that it is one of the firms who I would say pioneered the financial advisory model, and it seems to have suited them well, despite the growth of online self-guided trading/investing in the last decade. In other words, they provide a human value that technology alone cannot.

As their CEO said:

Our bankers provide differentiated insight, wise counsel, and discretion on the most challenging questions facing our clients.

The reason I don’t think it is a “sell” yet is because I expect share price appreciation to continue, so I’d hate to leave money on the table. It also could be a “hold,” however I usually call a hold on stocks I am more neutral about and this stock does present a stronger case for a long-term buy, so I am not neutral but bullish.

A Proven Revenue Grower in Difficult Year

To kick off this analysis, I wanted to focus on the most important metric I am considering, and that is whether this firm was able to grow revenue despite the challenging environment facing this sector last year.

Before talking about future performance expectations, here are recent past performance figures.

This firm saw revenue grow to $806MM in Q4, vs $720MM in Dec 2022, a 12% YoY growth.

From the income statement, although net interest income has actually been realizing a loss, apparently due to interest expense exceeding interest income, being a diversified firm, Lazard also has significant non-interest revenue and the growth trend has been coming from underwriting / investment banking fees, and asset management fees. I think this also sets it apart from the regional banks in this overall sector, who do not have such a large fee-driven business as Lazard.

Q4 company commentary indicates an uptick in business for the financial advisory division:

During and since the fourth quarter of 2023, Lazard has been engaged in significant and complex M&A transactions globally.

Its asset management division also saw growth in assets under management (AUM) which is a driver of fees income:

AUM as of December 31 was $247B, 14% higher than December 31, 2022, and 8% higher than September 30, 2023. The sequential change from September 30, 2023 was driven by market and foreign exchange appreciation of $16.9B and $5.0B, respectively, offset by net outflows of $3.6B.

My impression is that this strong performance across both of its key business segments sets the stage for confident entry into 2024, and indication that investment banking activity in particular is already on a rebound, which is a good thing for a firm experiencing a squeeze to its net interest margin, as it can rely on fees-driven business segments and not only interest-driven ones.

Some key wins from Q4 to mention, in the investment banking space:

Sanofi’s (SNY) $2.4B acquisition of Inhibrx (INBX), Lincoln Financial Group’s $28B reinsurance transaction with Fortitude Re, The Restaurant Group plc’s (OTCPK:RSTGF) £701 million acquisition by Apollo Global Management.

It is notable to mention that Lazard has significant geographic penetration outside its US base, according to its q4 presentation, and I think this is an added value as it indicates geographic diversification of the business.

Lazard – geographic reach (Lazard q4 presentation)

Earnings Rebound Late in Year

When it comes to the bottom line, earnings (net income) grew to $63.6MM in Q4, vs $42.4MM in Dec. 2022, for a 50% YoY growth.

This profitability growth was achieved despite increased expenses. For example, company Q4 comments indicate there has been a spike in both comp/benefits expenses as well as “increased occupancy costs and professional services expenses.”

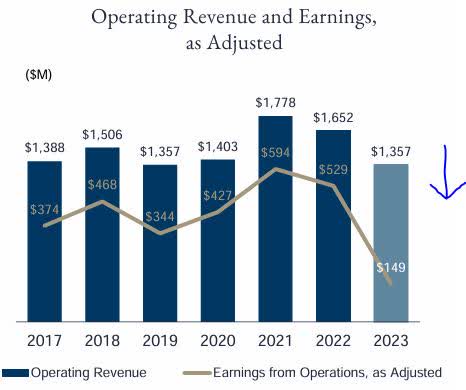

If I look at the following chart, it indicates a trend of declining earnings in 2023 in their advisory segment, for example, on a year-to-year comparison, indicating last year was overall a more challenging year.

Lazard – declining earnings (company q4 results)

A similar trend was seen in 2023 in their asset management segment, compared to prior years.

In terms of the overall sector they are in and the challenges it faced, it is known that the investment banking space faced headwinds last year. Consider the following data according to a Jan. 23rd study by PwC:

M&A volumes and values declined by 6% and 25% in 2023 compared to the prior year. Hopes for a rebound early in the year were dashed by rising interest rates and financing challenges.

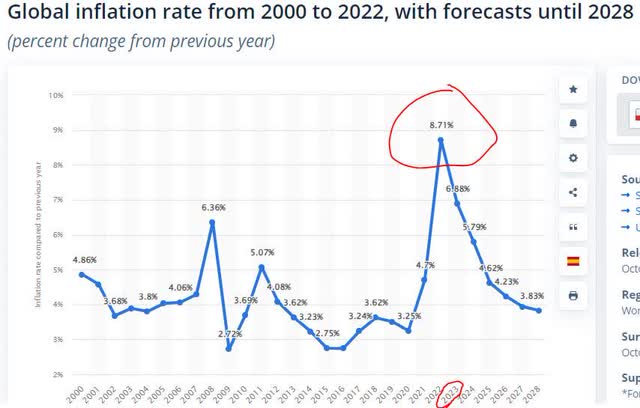

At the same time, while business slowed down in that regard, data also shows that 2023 saw increased inflation, which I believe can drive up costs for businesses. The following chart from data website Statista shows that 2023 was one of the worst years lately for inflation, so this is something this firm had to deal with in terms of managing business expenses, but so did all other firms:

Statista – inflation rates (Statista)

My overall impression is that overall the earnings struggle at Lazard last year was a combination of lower investment banking business combined with higher costs, a bad mix. At the same time, heading into the last quarter of the year, the firm was able to achieve earnings improvements, indicating a rebound, and I think inflation-driven business costs will come down going forward as the inflation chart above is predicting a steady decline in inflation heading into the next few years, which should help the bottom line improve.

Balance Sheet Strength Continues

In this category of past performance, I am looking for positive equity growth at this firm but also capital strength, since equity growth by itself is not an ideal indicator (example: dividend payouts or share buybacks can decrease equity).

The balance sheet indicates equity fell to $569.9MM in Q4, vs $1.25MM in Dec. 2022.

However, consider that in the context of the following from Q4 commentary:

In the fourth quarter of 2023, Lazard returned $44 million to shareholders, which included: $43.7 million in dividends and $0.6 million in satisfaction of employee tax obligations in lieu of share issuances upon vesting of equity grants.

Further, the firm boasted of a strong financial position, as “cash and cash equivalents were $971 million.”

The following graphic indicates this firm’s capital strategy, so the equity growth or decline should be viewed in the context of this as well.

Lazard – capital strategy (company results)

My impression is that although equity declined, at the same time the firm has been on a trajectory of returning capital back to shareholders but also reinvesting in its own growth, two positives in my book, as well as being a firm with a strong cash position and if you look at its long-term debt on the balance sheet you see that it has not gone up that much on a YoY basis, hovering around $1.69B.

Dividend Yield Beats Key Peers

If you are a dividend-income investor like I am, you may be interested in this firm’s dividend yield vs some key peers/competitors, to get the best yield on capital invested at current share price.

The below chart uses dividend data from Seeking Alpha and its comparison tool.

Lazard – dividend yield vs peers (Seeking Alpha)

In a basket of comparable firms, Lazard comes ahead with a trailing yield of 5.37%.

Others I compared against included Piper Sandler (PIPR) at 1.96%, Stifel Financial (SF) at 1.91%, Morgan Stanley (MS) at 3.96%, and Goldman Sachs (GS) at 2.78%.

So, my impression is that if dividend yield alone were a factor and nothing else, the obvious choice from these peers would be Lazard with its +5% yield.

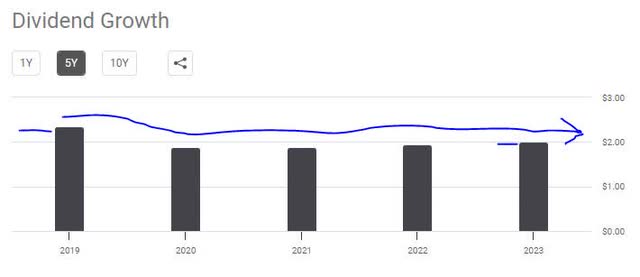

Dividend Growth Struggling to Take Off

Although dividend yield is impressive, I also care about whether this firm has proven itself as a dividend grower in the last 5 years. Though this does not guarantee future dividends, it does tell me something about the recent history of a firm and whether it has a proven track record in growing its dividend.

At Lazard, dividend growth data up until now indicates a declining trend in dividend growth:

Lazard – dividend growth 5 yrs (Seeking Alpha)

For example, it went from $2.35/share/annual in 2019 to $2/share/annual in 2023, a nearly 15% decline over 5 years. This tells me the firm has decided to retain more of its cash in that period, either due to mediocre earnings or expected business headwinds up ahead.

And, according to dividend history, although the dividend has grown since 2020 levels, the last time it saw a hike was August 2022.

So, if I was a dividend investor buying into this stock in 2019, I actually would have seen declining dividend income in an overall sense in this 5-year period.

My impression is that so far this stock has not been a strong dividend grower, and understandably the earnings headwinds in 2023 likely prevented further dividend hikes, while future hikes in 2024 and beyond will likely also depend on strong earnings, I think. At the same time, the history shows dividend quarterly payouts were stable and were not suspended at any point, which is a plus.

EPS Growth Expected for 2024

Now that I have talked about past performance up until now, it is time to dive into some forward projections, since my readers who are longer-term investors will care about future performance estimates.

I can see from the analyst consensus estimates that a +305% YoY growth in the EPS is expected by Dec. 2024, and another +34% growth by Dec. 2025.

In addition, there have been 4 upward revisions to EPS vs just 2 downward revisions.

Returning to the study I mentioned earlier from PwC, it is very bullish on the potential this year in the investment banking space, which I think will benefit Lazard as well:

We are hearing the starting bell sounding for an upswing in M&A activity, signaling an end to one of the worst bear markets for M&A in a decade. Whilst the strength and speed of the recovery remain uncertain due to lingering macroeconomic and geopolitical challenges, we believe we have reached a tipping point.

Besides investment banking, since Lazard also has an asset management business and increasing portfolio values can mean increasing fees for the firm, what could favor future earnings at Lazard in that segment would be a rise in equity markets, potentially driving the values of equities in those portfolios upward.

Seeking Alpha’s article last week said that so far, “2024 has experienced a succession of new highs for the S&P 500.”

In addition, back in January an article in Forbes said the following which supports a bull case for equity markets this year:

Analysts project 11.5% earnings growth and 5.5% revenue growth for S&P 500 companies in 2024.

Fortunately, analysts see positive earnings and revenue growth for all eleven market sectors this year.

Earlier I mentioned that the firm has faced a squeeze to its net interest income. However, I expect this trend to alleviate later this year. In terms of interest rates, I use the CME FedWatch tool, which indicates a 52% probability the Fed will lower rates after its June meeting.

This ought to ease the rising interest expenses the firm has been facing. In fact, interest expenses in Q4 have already eased slightly compared to June 2022 when they were near their peak:

Lazard – interest expenses (Seeking Alpha)

My own overall impression is in agreement with the analyst consensus of future EPS growth and I believe it will be driven by what I mentioned: lower interest rates later this year reducing the squeeze on interest margins, increased investment banking activity and M&A, and improving equity markets driving higher fees on equity portfolios managed by Lazard in their asset management segment. So, all of their segments will be benefiting from the environment in 2024.

Unimpressive Revenue Growth vs Peers with Larger Wealth Advisory Shops

Now that we covered profitability (earnings) growth, let’s take a moment to talk about top-line growth potential vs peers. Using the SA comparison tool, l am comparing expected (forward) revenue growth of Lazard vs the four peers I mentioned earlier: Morgan Stanley, Piper Sandler, Goldman Sachs, and Stifel.

Lazard – rev growth vs peers (Seeking Alpha)

What this table tells me is that Lazard, with a forward revenue growth of +4.53%, is somewhere around 3rd place in this peer group, which is led by Piper Sandler at +7.74% forward revenue growth expected.

My impression is that the evidence I already presented supports revenue growth projections for this entire subsector of financials, due to the expected increase in dealmaking, and improvements to equity markets driving asset management businesses, which all of these firms are involved in.

However, it also means that Lazard has stiff competition in this space. In addition, where Lazard lacks vs Morgan Stanley, for example, is market dominance in private wealth management, which I think is a huge business. We already know Lazard’s asset management segment includes wealth advisory for family offices, however, how does its wealth practice compare to Morgan?

An April 2023 list by Forbes, for example, shows that Morgan Stanley has 5 of the top 20 wealth advisors in America, whereas Lazard is not even in the top 20 at all. I think in this regard Lazard trails behind some peers as wealth advisory can mean significant fees revenue.

Fair Buying Price Based on Future EPS Estimates

At this point, I know that this firm is likely to see earnings growth looking ahead, and I described why, and also we talked about where it lacks vs its peers, but is the current price and valuation mix supportive of buying this stock today at the current price?

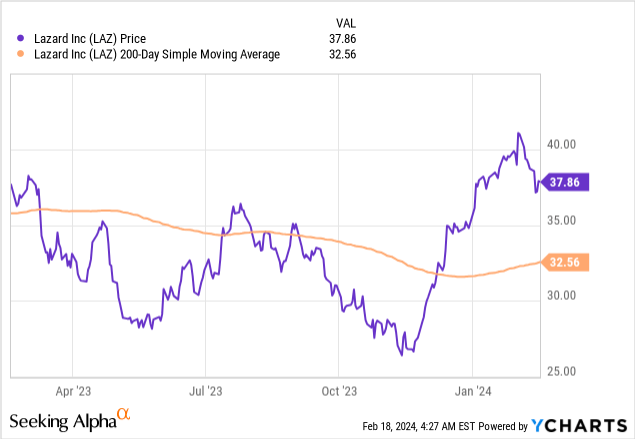

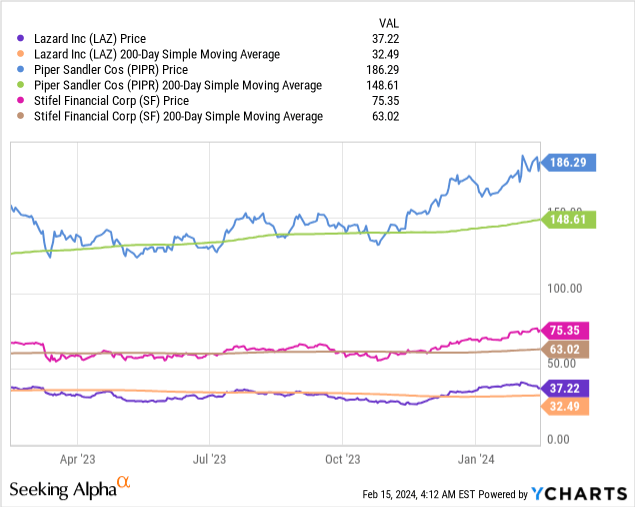

For this part, let’s look at the YChart showing the price vs the 200-day SMA, over a period of 1 year, pulled from Friday’s closing data:

The chart tells me this stock has rebounded meteorically since its low this fall, now trading around $37.86, around +16% above its moving average.

Comparing with two peers mentioned already, Stifel and Piper Sandler, they too have seen their price rise well above its moving average, indicating to me that the market is bullish on investment banks, likely for the reasons I mentioned earlier:

In terms of valuations, Lazard has a forward P/E ratio of 16.02, which is actually significantly higher than its sector average of 10.74.

However, if the sector being used is “financials”, then that also would include regional banks and other financial firms. Because the forward P/E is also elevated above the sector average at Stifel, and Goldman Sachs too, as two examples, this tells me the market is bullish on future earnings prospects for firms in this sector that are predominantly investment banks. If you look at the P/E ratio of Regions Financial (RF), by comparison, a regional bank, it is valued below the sector average, at just 9.4x forward earnings.

In terms of price to book value, Lazard’s forward P/B ratio is 5.60, also significantly above the sector average, indicating to me that the market is bullish on forward equity growth potential at this firm as well.

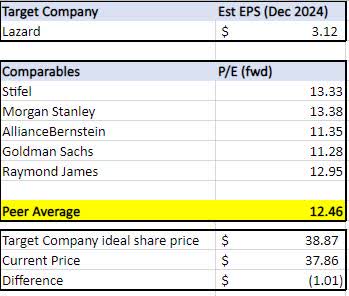

Here is what I think personally as to whether the current valuation on Lazard justifies buying it at this share price, and to come to that business decision I used a variation of the comparable companies analysis method, which is a standard practice.

Lazard – comps table (author)

In this example, I am multiplying the peer average of forward price-to-earnings multiples (P/E) by my target company’s estimated future EPS, to get to an ideal share price if I was buying today.

This table determined that an ideal share price today is $38.87, and since the stock is most recently trading under that number, I’d consider it a fair buying price.

A Low Risk Profile and Strong Liquidity

The macro trend of a high interest rate environment making debt more costly is certainly a risk to consider for firms that have a significant corporate debt.

On a micro level, corporate debt can impact a firm’s equity but also can impact profits due to interest expenses.

A firm engulfed in debt also can see an impact to its credit score, which can make it more costly to borrow and also less attractive to investors, impacting the share price. This could be a potential downside risk.

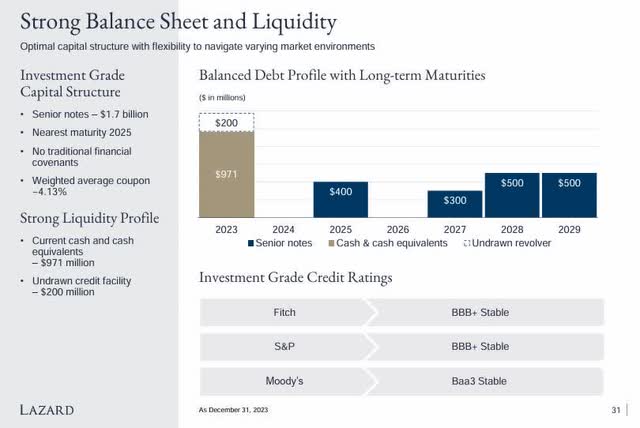

So, I wanted to take a look at the following graphic from this firm’s Q4 presentation:

Lazard – debt structure (company q4 results)

On the bright side, there are no major note payments in 2024, the next one not until 2025. Further, all three credit rating agencies have rated this firm as “stable.”

The firm also can tap into $200MM of undrawn credit, and boasts +$970MM in cash going into 2024.

My impression is that this firm has a low risk profile in this category, as the evidence supports it. Also, unlike some traditional “banks” I wrote about lately or mentioned, especially some regional ones, it does not mention having any exposure to commercial real estate loans on office property.

I think that is another reason the buyers are flocking to this subsector of financials, as it does not present the same type of risk profile as regional banks may have.

However, I should also mention that in this subsector of financials, particularly asset managers, I look at trends like net inflows/outflows of client monies being managed. A significant trend showing continual net outflows from a firm would be a potential downside risk to investing in Lazard. As of the latest data showing end-of-January AUM, the firm’s AUM of $243.8B was down 1.1% month-over-month. Part of this was driven, it seems, by net outflows of $2.1B.

While the news of net outflows is not great, I don’t think a 1.1% drop in AUM vs the prior month, for a firm of this size and AUM level, is overly concerning. However, it could be something to keep track of over the course of two or three quarters to see if it is a growing trend, as declining AUM can impact fee revenue, just like rising AUM can improve fee revenue.

Conclusion: A Strong Dividend Yield Play at a Fairly Valued Price

I am long on Lazard stock as it is a long-established investment bank and asset manager among the leading brands in that space, and will be in a unique position to take advantage of the expected growth in M&A and dealmaking activity as well as the rise in equity markets which will help its asset management business.

On the flip side, it is not a major player in the wealth management space when comparing to some larger peers like Morgan Stanley, so that is something to consider, since wealth advisory is a huge industry.

For dividend investors, a +5% dividend yield is something to take advantage of certainly, and the most recent share price still presents a fair valuation in my opinion.

So, to summarize in a sentence, I would buy it because I’m getting an established business with future growth prospects and an attractive yield, still at a fairly valued share price, before it soon becomes too expensive to be a buy any longer, and it is approaching that point as I have shown.

Read the full article here