Welcome to the December 2023 edition of the lithium miner news.

The past month saw lithium prices fall below the marginal cost of production and therefore should be approaching a bottom very soon; assuming EV sales hold up in 2024. China December NEV sales are on track for a very strong end to 2023, CPCA ‘forecasts’ are for a record 940,000 sales, up 46.6% YoY.

Lithium price news

Asian Metal reported during the past 30 days, the 99.5% China delivered lithium carbonate (99.5% min.) spot price was down 10.35% and the China lithium hydroxide (56.5% min.) price was down 8.68%. The Lithium Iron Phosphate (3.9% min) price was down 5.29%. The Spodumene (6% min) price was down 6.5% over the past 30 days.

Metal.com reported lithium spodumene concentrate Index (Li2O 5.5%-6.2%, excluding tax/insurance/freight) spot price of USD 1,380/t, as of Dec. 22, 2023.

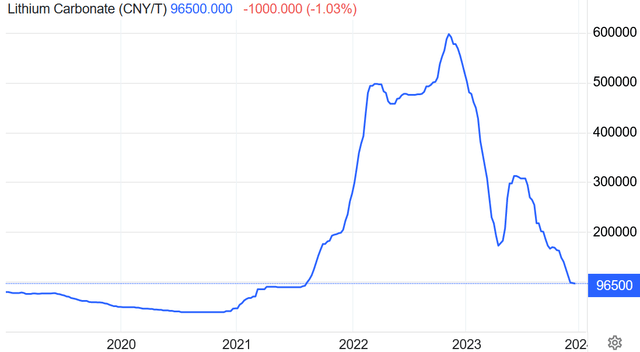

China lithium carbonate spot price 5 year chart – CNY 96,500 (~USD 13,528) (source)

Trading Economics

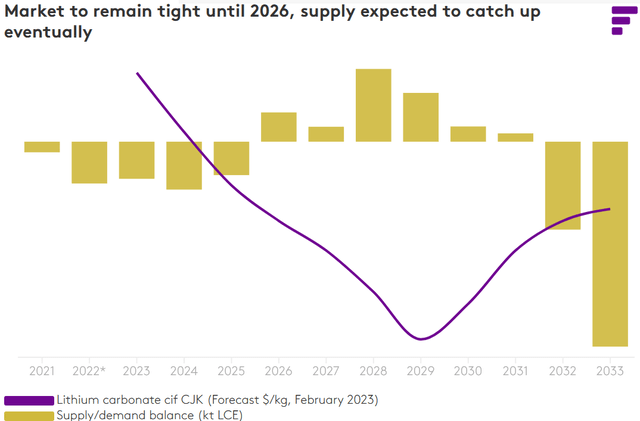

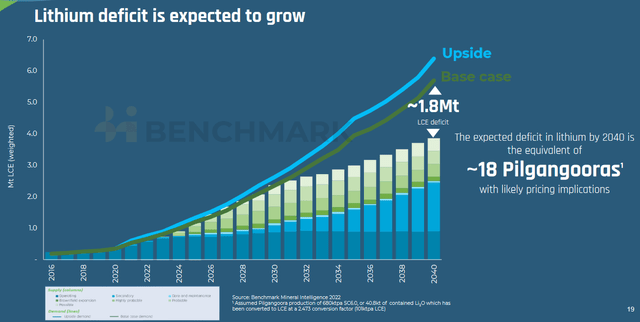

Lithium demand versus supply outlook

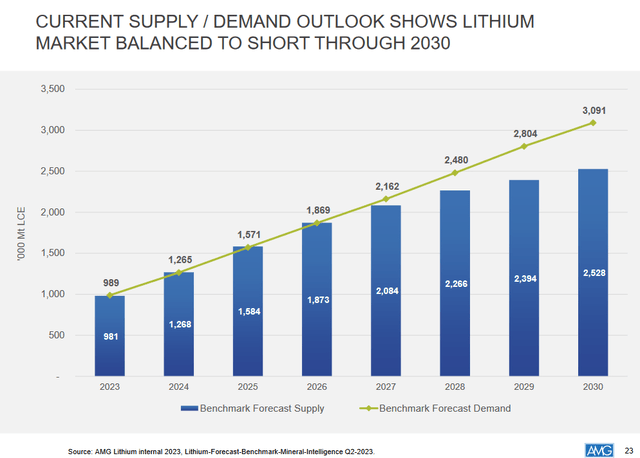

BMI (Q2, 2023 forecast) – Lithium market balanced to short through 2030 (source)

BMI

2022 – UBS lithium demand v supply forecast to 2030

UBS

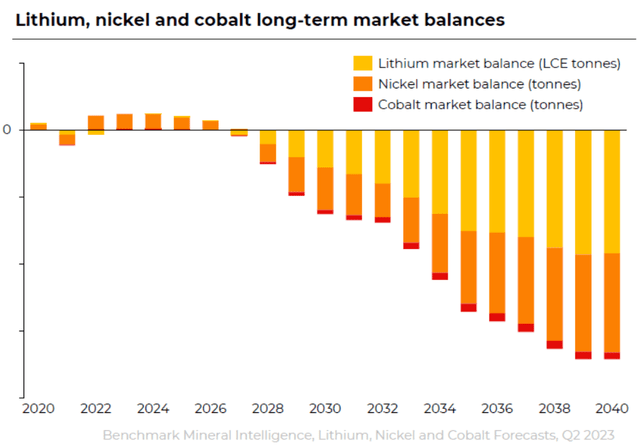

Benchmark Mineral Intelligence forecasts small lithium surpluses then deficits for lithium, nickel & cobalt to increase from 2027 onwards (source)

BMI

Fastmarkets forecasting mostly lithium deficits ahead to 2025 (as of March 2023) (Source)

Fastmarkets

Lithium demand v supply forecast by Benchmark Mineral Intelligence (mid 2022 forecast)

BMI

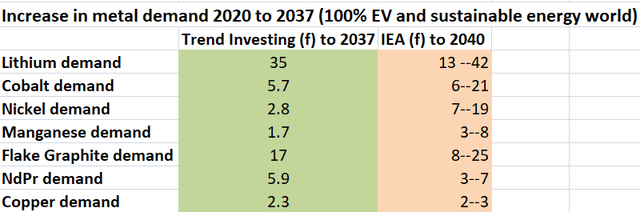

Trend Investing v IEA demand forecast for EV metals (IEA)

Trend Investing & the IEA

Lithium market and battery news

On November 27, the Financial Times reported:

Mining tycoons battle over lithium’s ‘corridor of power’ in Australia… Rinehart and Ellison have become increasingly active investors in a host of small lithium projects in both parts of the state, where foreign companies including Albemarle, SQM and China’s Tianqi Lithium have previously been among the biggest investors.

On November 27, Fastmarkets reported:

Four key talking points ahead of the Fastmarkets China Battery Raw Materials Conference 2023….Fastmarkets analysts forecast an oversupply in the global lithium market in 2023, with a surplus of 25,400 tonnes of lithium carbonate equivalent (LCE). The surplus will shrink to 5,150 tonnes of LCE in 2024…

On November 30, GS Publishing reported:

Lithium: The short trade must go on…the softening in the lithium market has become incrementally apparent with the slowdown in demand growth now in direct contrast with growing global lithium supply…The rise in chemical output has overtaken the growth in China battery output and China’s imports of spodumene concentrate (+60% y/y YTD) – particularly from Australia and Zimbabwe – have continued to grow sharply. However, with the market largely balanced YTD, the full extent of supply led surplus is yet to be realised with prices still 33% above the top-end of the integrated cost curve. We expect the lithium market to be in a 202kt surplus next year – which represents 17% of global demand – and continue to expect prices to trade deeply into the cost curve to balance the market. In this context, we maintain our bearish view on the lithium market and lower our 12m target for China Lithium Carbonate (excluding VAT) to $11,000/t and CME Asia CIF Lithium Hydroxide to $12,000/t (from $15,000/t and $16,500/t respectively previously)…Even with a sharp correction in prices, Chinese battery grade lithium carbonate price is still ~$4k/t LCE (or 33%) above the top-end of integrated cash cost curve, but ~60kty of non-integrated production using purchased spodumene is in loss-making. Our China equities team estimates the cash cost of production for integrated Chinese lepidolite is between $8k-12k/t LCE with key cost inflation risk from higher tailings management cost (additional $2k/t LCE). The integrated production using African concentrates (Zimbabwe and Mali) is estimated to range from $7k-$13k/t LCE…The global hardrock supply – mostly concentrated in Australia – is set to increase by 280kt LCE over 2024 to represent ~80% of global supply growth…In a highly constrained scenario, we estimate the market would still be in a substantial surplus (155kt vs 202kt surplus in base case for 2024).

On December 1, NASDAQ reported:

South Korea’s Ecopro BM wins $34 bln order from Samsung SDI…to supply cathode materials to Samsung SDI from 2024 to 2028. Samsung SDI supplies electric vehicle batteries to BMW BMWG.DE, General Motors GM.N, Hyundai Motor 005380.KS and others.

On December 1, Energy.gov announced: “Department of Energy releases proposed interpretive guidance on Foreign Entity of Concern for public comment.”

On December 5 Fastmarkets reported:

A Foreign Entity of Concern (FEOC) includes any foreign entity that is “owned by, controlled by or subject to the jurisdiction or direction of a government of a covered nation”. Those countries that currently fall into this “covered nation” category are China, Russia, North Korea and Iran…Starting from next year, with a period of transition, companies that have a more than 25% ownership or control by a FEOC – including board seats, voting rights or equity – will not be eligible for tax credits available under the Inflation Reduction Act (IRA). “To strengthen the security of America’s supply chains, beginning in 2024, an eligible clean vehicle may not contain any battery components that are manufactured or assembled by a FEOC, and, beginning in 2025, an eligible clean vehicle may not contain any critical minerals that were extracted, processed or recycled by a FEOC,” the Department stated…

On December 6, BNN Bloomberg reported:

Surge in lithium stocks raise hope rout in EV metal almost done. Tianqi Lithium Corp. and Ganfeng Lithium Group Co. — closed up 6.5% and 7%, respectively, in Hong Kong on Wednesday. The sharp gains suggest investors may be positioning themselves for a recovery in prices. Lithium carbonate futures for January delivery on the Guangzhou Futures Exchange traded at 92,450 yuan ($12,915) a ton on Wednesday, down from more than 200,000 yuan when the bourse debuted the contracts in July. The downward trend for lithium is “already nearing an end,” said Zhang Weixin, an analyst at China Futures Co. It’s likely to bottom out between 80,000 and 90,000 yuan a ton, he said. Spot prices of lithium carbonate, a partially processed form of the metal, are down more than 80% from a peak last November to 98,500 yuan ($13,761) a ton…In the longer term, the question is whether the current cycle of lower prices sees companies canceling or delaying plans for new mines or refineries, absent policy support from governments that are aiming to build out their own supply chains. Albemarle Corp., the world’s largest lithium producer, said last month that this is already starting to happen. The plunge in lithium prices has almost reached a bottom, but an extended period of weakness is still likely, Wei Xiong, an advisor at raw materials trader Traxys, said at the conference in Shanghai. A turning point to monitor is “whether high-cost mines will exit,” he said.

Note: Bold emphasis by the author.

On December 7, Reuters reported:

Allkem sees low lithium prices extending over near term – chair…Lithium prices overshot last year driven by China but this year fresh supply, including from Africa, has led to a collapse in prices, Coleman said at an event in Melbourne.

On December 11, Fastmarkets reported:

Spodumene prices continue to fall amid weaker demand for lithium. Spodumene concentrate prices have collapsed amid downstream pressure on lithium chemicals prices and weak physical demand for material on a spot basis ahead of the year-end…Fastmarkets assessed spodumene min 6% Li2O, spot price, cif China at $1,000-1,200 per tonne on Friday December 8, down $200-300 from $1,200-1,500 per tonne in the previous session…Fastmarkets assessed the lithium hydroxide monohydrate LiOH.H2O 56.5% LiOH min, battery grade, spot price cif China, Japan & Korea at $16-17.50 per kg on Monday, narrowing downward from $16-18 per kg the previous day. The assessment of lithium carbonate 99.5% Li2CO3 min, battery grade, spot prices cif China, Japan & Korea fell to $15.50-16.50 per kg on Monday, down 50 cents from $16-17 per kg on Friday.

On December 11, S&P Global reported:

New lithium mining, refining projects set to strengthen Europe’s battery supply chains. Annual lithium processing capacity to reach 650,000 mt/year by 2028. OEMs adopting local-for-local approach to their supply chains. CRMA to accelerate project permitting process. Several European lithium mining and refining projects are poised to launch commercial operations next year.

On December 12, Sprott ETFs reported: “Lithium-ion technology solidifies lead in EV battery stakes.

- Lithium-ion batteries (LIBs) have entrenched their lead as the technology of choice for EVs because of their superior technical properties and decades of investment in development and infrastructure.

- The rise of LIBs in energy storage echoes the rise of photovoltaic (PV) panels in solar electricity. Both technologies have gained dominance due to their cost-effectiveness and rapid rate of technological improvement.

- Competing technologies like solid-state and sodium-ion batteries show promise, but we do not see an imminent threat to LIBs due to their technical and economic advantages….”

On December 21, Seeking Alpha reported: “Tesla supplier Panasonic shelves plan to build EV battery plant in Oklahoma.”

On December 21, Mining.com reported:

Milei looks to cut costs for Argentina’s miners in broader deregulation push. President Javier Milei wants to turn Argentina’s lithium and copper rush into an investment bonanza — starting with cutting red-tape…Milei plans to do that by revoking two laws enacted in the 1990s — the National System for Mining Trade and the National Mining Data Bank. Both require firms to provide reams of data to the government. He’s also planning to do away with customs restrictions… “From today on, it’s prohibited to prohibit exports,” Milei said.

Lithium miner news

Albemarle (ALB)

No news for the month.

Sociedad Quimica y Minera S.A. (SQM), Wesfarmers [ASX:WES] (OTCPK:WFAFY), Covalent Lithium (SQM/WES JV

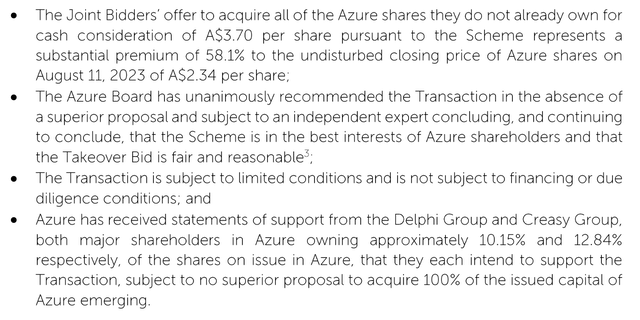

On December 18, SQM announced: “SQM and Hancock enter into implementation deed with Azure Minerals.” Highlights include:

SQM

Upcoming catalysts:

Q4, 2023 – Mt Holland spodumene production targeted to begin (SQM/Wesfarmers JV).

H1, 2025 – Production to start and then ramp to 50ktpa Lithium hydroxide [LiOH] at the Kwinana refinery in WA (SQM/Wesfarmers JV).

Jiangxi Ganfeng Lithium [SHE:002460] [HK: 1772] (OTCPK:GNENY)

On December 12, Ganfeng Lithium announced:

Enhancing the share of green power, Ganfeng Lithium completes the first unsubsidized green certificate transaction in Jiangxi Province…

On December 12, Ganfeng Lithium announced:

PPG Project Pilot Plant in Argentina successfully started production… Currently, the planned annual production capacity of the PPG project is 50,000 tons of lithium carbonate, with salt field construction scheduled to commence at the end of 2023 and production expected to start in 2026. Due to the excellent salt lake endowment, the project will use solar evaporation to extract lithium and collect it at a central processing location through pipeline transportation. The first phase of the project is expected to create more than 1,000 job positions locally…

Note: PPG stands for Pozuelos and Pastos Grands.

On December 12, Ganfeng Lithium announced:

Ganfeng Lithium won the 2023 Fortune China ESG Impact List and Wall Street Journal’s “ESG Innovation Experiment of the Year”.

On December 12, Ganfeng Lithium announced: “Cauchari-Olaroz Project in Argentina officially commences production…”

(Chengdu) Tianqi Lithium Industries Inc. [SHE:002466], Tianqi Lithium Energy Australia (TLEA) is a JV with Tianqi Lithium (51%) and IGO Limited (49%). TLEA owns the Kwinana lithium hydroxide facility in WA

On December 11 IGO Limited announced: “IVAN VELLA COMMENCES ASCHIEF EXECUTIVE OFFICER & MANAGING DIRECTOR.”

Pilbara Minerals [ASX:PLS] (OTC:PILBF)

On November 30, Pilbara Minerals announced:

POSCO Pilbara Minerals JV opens South Korean Lithium Hydroxide Facility…The Chemical Facility is owned and operated by the POSCO Pilbara Lithium Solution Co Ltd (PPLS) joint venture (JV) with POSCO Holdings owning 82% and Pilbara Minerals owning 18%. Pilbara Minerals has the option to increase its equity interest to 30% at any time up to 18 months after successful ramp of the Chemical Facility to 90% of nameplate capacity. Train 1 of the Chemical Facility is designed to produce 21.5 thousand tonnes per annum (ktpa) of lithium hydroxide when at nameplate capacity with commissioning to commence shortly.

On December 21, Pilbara Minerals announced: “Pilbara Minerals’ power strategy to reduce emissions intensity and costs.” Highlights include:

- “The Power Strategy involves a three-staged approach. Stage 1 transitions thermal generation from predominantly diesel to natural gas and BESS. Stage 2 aims to increase existing solar generation at site, and Stage 3 plans the addition of emerging wind power generation should it become available via grid connection by 2030…”

Upcoming catalysts:

- End Q2, FY 2024 – P680 Expansion Project set to reach full capacity.

- Q3 FY, 2025 – P1000 Expansion Project set to begin production.

Mineral Resources [ASX:MIN] (OTCPK:MALRF)

Mineral Resources lithium assets include Mt Marion Mine (50% MIN: 50% Ganfeng). Wodgina Lithium Mine (50% ALB: 50% MIN).

On December 1, Mineral Resources announced:

Develop awarded Mt Marion Lithium underground development contract. Develop Global Limited (ASX: DVP) is pleased to announce that it has been awarded a A$46 million underground development contract to establish and develop an exploration decline at the Mt Marion lithium mine in WA. Mt Marion, which is a joint venture between Mineral Resources Limited (ASX: MIN) and Ganfeng Lithium Co. Ltd, is located 40km south-west of Kalgoorlie. It is also 95km from Develop’s Pioneer Dome Lithium Project. The contract has a term of 18 months and is expected to start in early 2024.

Livent Corp. (LTHM) [GR:8LV] (NB: Alkem and Livent plan to merge on January 4, 2024) – new company to be called ‘Arcadium Lithium’

On December 14, Livent Corporation announced:

Livent invests in ILiAD Technologies to strengthen leadership in direct lithium extraction production processes…”The ILiAD platform is a next generation, best-in-class technology that we expect will enhance and complement Livent’s existing proprietary processes, helping us build upon our decades-long record of successfully using DLE-based production processes at commercial scale.”

On December 19, Livent Corporation announced:

Livent and Allkem shareholders approve merger of equals…”The strong support of Livent and Allkem shareholders for this transformational merger is a testament to the compelling value proposition of Arcadium Lithium,” said Paul Graves, President and CEO of Livent and future Chief Executive Officer of Arcadium Lithium. “We look forward to closing the merger and pursuing the opportunities to create greater long-term, sustainable value for all of our stakeholders.”

Allkem [ASX:AKE] [TSX:AKE] (OTCPK:OROCF)(NB: Alkem and Livent plan to merge on January 4, 2024) – new company to be called ‘Arcadium Lithium’

On December 15, Allkem announced: Sal de Vida Project financing increases to US$180M.” Highlights include:

- “In July 2023, IFC project financing for the development of SdV Stage 1 was signed for up to US$130M.

- IDB Invest has agreed to provide additional long term financing of US$50M on terms materially consistent with the IFC and will support sustainable development in line with internationally recognised environmental and social standards.

- The increased project financing of US$180M remains structured as green and sustainability-linked loans. IFC and IDB Invest’s environmental and social performance requirements are globally recognised and the awarding of sustainability-linked, green loans to the facility is recognition and validation of the high ESG standards already adopted at Sal de Vida by Allkem.”

AMG Critical Materials N.V. [NA:AMG] [GR:ADG] (OTCPK:AMVMF) (Formerly AMG Advanced Metallurgical Group NV)

No news for the month.

Upcoming catalysts:

- H1, 2024 – Stage 2 production at Mibra Lithium-Tantalum mine (additional 40ktpa) forecast to begin, bringing total production capacity to 130ktpa. The lithium concentrate plant shutdown to facilitate the expansion from 90,000 tons to 130,000 tons will take place in the first quarter of 2024.

- 2025-2028 – German LiOH facility expansion plan with Modules 2-5 (100,00tpa LiOH).

Sayona Mining [ASX:SYA] (OTCQB:SYAXF)

On December 6, Sayona Mining announced: “Drilling underway at Tabba Tabba Lithium Project.” Highlights include:

- “Maiden drilling commences at Sayona’s 100% owned Tabba Tabba Lithium Project, Western Australia.

- 76 aircore drill program planned over extensions to historic Tabba Tabba tantalum mine (owned by Wildcat Resources) and at Roadside Prospect located in southern tenement area.

- Site works for follow up deeper drilling completed, with 7.5km prospective corridor identified for 2024 drill testing.”

Upcoming catalysts include:

- 2023 – Spodumene production ramp up at NAL operations (owned SYA 75%: PLL 25%).

Piedmont Lithium (PLL)[ASX:PLL]

Piedmont Lithium 100% own the Carolina Lithium spodumene project in North Carolina, USA; as well as 25% of the North American Lithium [NAL] Project in Canada and up to 40.5% of the Ewoyaa Lithium Project in Ghana (JV with Atlantic Lithium and Ghana Gov + Ghana MIIF).

On November 28, Atlantic Lithium announced:

106m continuous pegmatite interval reported broad intervals of visible spodumene observed in multiple drill holes outside of the current Mineral Resource Estimate. Longest continuous pegmatite interval reported from the ongoing, recently-enhanced 2023 drilling programme.

On December 12, Atlantic Lithium announced:

Maiden Feldspar Mineral Resource Estimate 15.7Mt at 40.2% Feldspar Ewoyaa Lithium Project, Ghana. Maiden MRE reported for feldspar at Ewoyaa, intended to be supplied to the local Ghanaian ceramics industry and expected to further enhance the Project’s economics.

Upcoming catalysts include:

- Early 2025 – Ewoyaa Project in Ghana (40.5% PLL) targeted to begin.

- 2026 – Tennessee Lithium hydroxide project targeted to begin.

- 2023-25 – Carolina Lithium (100%) – Permitting, off-take or project funding announcements.

Core Lithium Ltd. [ASX:CXO] [GR:7CX] (OTCPK:CXOXF) (OTC:CORX)

Core 100% owns the Finniss Lithium Project (Grants Resource) in Northern Territory Australia. Significantly they already have an off-take partner with China’s Yahua (large market cap, large lithium producer), who has signed a supply deal with Tesla (TSLA). The Company states they have a “high potential for additional resources from 500km2 covering 100s of pegmatites.”

On December 22, Core Lithium Ltd. announced:

Strategic review of operations underway. Core Lithium Ltd (ASX:CXO) (Core or the Company) has been undertaking a strategic review of operations to address the deterioration in lithium market conditions. The price of spodumene concentrate has declined more than 80% year to date, including by more than 40% since the end of October 2023. As noted at the Company’s recent Annual General Meeting, Core continues to focus on factors within its control, including reducing costs, enhancing the mine plan, timing growth projects, and optimising our assets…Options being considered include changes to the mining strategy and plan, such as prioritising ore mining and possible temporary curtailment of mining operations, commercial solutions and reductions in exploration and other discretionary expenditures. Over recent months, the Company has built a significant ROM (run-of-mine) stockpile and will continue processing ore and making spodumene concentrate during the wet season. The review will prioritise preserving business value and future options. Given the difficulties associated with mining and construction in the wet season and the focus on reducing expenditure, BP33 early works have been suspended.

Catalysts include:

- 2024 – Results of the strategic review of operations at Finniss.

Sigma Lithium Resources [TSXV:SGML] (SGMLF) (SGML)

Sigma is developing a world class lithium hard rock deposit with exceptional mineralogy at its Grota do Cirilo Project in Brazil.

On November 27, Sigma Lithium Resources announced: “Sigma Lithium loads 22,000 tonne shipment of triple zero green lithium concentrate to Glencore at a premium price.” Highlights include:

- “Sigma Lithium announces that it will commence loading 22,000 tonnes of Triple Zero Green Lithium to Glencore at the Port of Vitoria during the week of November 27.

- Glencore will prepay 50% for the shipment of Sigma’s unique Triple Zero Green Lithium concentrate at a provisional “premium” price of 9% of the quoted LME lithium hydroxide price (average China, Japan, South Korea)…

- Demonstrates the consistent performance of Sigma Lithium’s Greentech Plant in ramp to achieve annual nameplate capacity of 270,000 tonnes of “Triple Zero Green Lithium”.”

On December 18, Sigma Lithium Resources announced:

Sigma Lithium provides update on final stage of strategic review: Initiates primary listing of Sigma Brazil on Nasdaq and Singapore…In connection with its Strategic Review Process, Sigma Lithium has entered contractual and detailed structural negotiations with finalists, which shall continue into the new year.

Upcoming catalysts:

- 2023 – Ramp up of spodumene production from Grota do Cirilo.

Lithium Americas Argentina [TSX:LAAC](LAAC)

Lithium Americas Argentina owns the Argentina assets (Cauchari Olaroz JV, Pastos Grandes, Sal de la Puna) from the LAC split.

No news for the month.

Upcoming catalysts:

- By mid 2024 – Cauchari-Olaroz lithium production ramp to 40ktpa. From 2025+ a Stage 2 20ktpa+ expansion is planned.

NB: Ganfeng Lithium (51%) and Lithium Americas Argentina (49%) own the JV company Minera Exar S.A., which owns 91.5% interest and is entitled to 100% of the production from the Cauchari-Olaroz Project. The 8.5% interest is owned by Jujuy Energia y Mineria Sociedad del Estado (“JEMSE”) (a company owned by the Government of Jujuy province).

Argosy Minerals [ASX:AGY][GR:AM1] (OTCPK:ARYMF)

Argosy has an interest in the Rincon Lithium Mine in Argentina, targeting a fast-track development strategy. Argosy initially plans to ramp to 2,000tpa lithium carbonate starting mid-2023.

On December 11, Argosy Minerals announced: “Rincon Lithium Project – progress update.” Highlights include:

- “2,000tpa operation works progressing; Comprehensive test works being conducted to determine optimum operational parameters and improve filtration rates. Planned critical works schedule to improve operational performance and increase production operations.

- EIA approval for 10,000tpa operation expansion awaited.

- Resource expansion upgrade being finalised.”

Upcoming catalysts:

- 2023/24 – Rincon Lithium full ramp-up toward steady-state production targeted, 2,000tpa operation.

Lithium miner ETFs

- Sprott Lithium Miners ETF (LITP) – A pure play lithium ETF

- Global X Lithium & Battery Tech ETF (LIT)

- ProShares S&P Global Core Battery Metals ETF (ION)

- The Amplify Lithium & Battery Technology ETF (BATT)

Global X Lithium & Battery Tech ETF (LIT) 10 year price chart (source)

Seeking Alpha

Trend Investing lithium demand v supply model forecasts

Our recently updated model forecast is for lithium demand to increase 4.9x between end 2020 and end 2025 to ~1.75m tpa, and 11.7x this decade to reach ~4.2 m tpa by end 2029 (assumes electric car market share of 27% by end 2025 and 51% by end 2029). These figures may be a bit lower if sodium-ion batteries take significant market share in stationary energy storage or low end vehicles.

Note: A Nov. 2020 UBS forecast is for “lithium demand to lift 11-fold from ~400kt in 2021 through to 2030.”

Conclusion

December lithium prices were lower again falling below the marginal cost of production.

Highlights for the month were:

- Australian mining tycoons Rinehart and Ellison have become increasingly active investors in a host of small lithium projects in WA.

- Fastmarkets forecast a surplus of 25,400 tonnes of LCE in 2023. The surplus will shrink to 5,150 tonnes of LCE in 2024.

- Goldman Sachs sees large lithium surplus in 2024 – Maintains bearish view and lowers 12m target for China Lithium Carbonate (excluding VAT) to $11,000/t (~CNY 78,500).

- Ecopro BM wins $34 bln order from Samsung SDI…to supply cathode materials to Samsung SDI.

- The U.S DoE releases proposed interpretive guidance on Foreign Entity of Concern (“FOEC”) rules. FOEC’s include China, Russia, North Korea and Iran. Starting 2024 companies that >25% ownership or control by a FEOC will not be eligible for tax credits available under the Inflation Reduction Act (IRA). Beginning in 2024, an eligible clean vehicle (for IRA credits) may not contain any battery components that are manufactured or assembled by a FEOC, and, beginning in 2025, an eligible clean vehicle may not contain any critical minerals that were extracted, processed or recycled by a FEOC.

- Surge in lithium stocks raise hope rout in EV metal almost done. China Futures Co. analyst, Zhang Weixin, forecasts lithium carbonate to bottom out between 80,000 and 90,000 yuan a ton.

- Allkem sees low lithium prices extending over near term.

- Fastmarkets: Spodumene prices continue to fall amid weaker demand for lithium.

- New lithium mining, refining projects set to strengthen Europe’s battery supply chains. Processing capacity to reach 650,000 mt/year by 2028.

- Lithium-ion technology solidifies lead in EV battery stakes.

- Milei looks to cut costs for Argentina’s miners in broader deregulation push.

- SQM and Hancock enter into implementation deed with Azure Minerals.

- POSCO Pilbara Minerals JV opens South Korean Lithium Hydroxide Facility.

- Livent and Allkem shareholders approve merger of equals. New company name to be Arcadium Lithium.

- Atlantic Lithium/Piedmont Lithium Ewoyaa JV Project in Ghana reports 106m continuous pegmatite with broad intervals of visible spodumene.

- Sigma Lithium has entered contractual and detailed structural negotiations with finalists.

- Argosy Minerals – Planned critical works schedule to improve operational performance and increase production operations at Rincon.

As usual all comments are welcome.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here