")

Investment overview

I see Marqeta (NASDAQ:MQ) stock as a compelling long-term investment opportunity over the medium term, hence, I am recommending a buy rating. There are strong secular tailwinds in play there that I believe will continue to drive long-term growth for MQ. Its product moat should enable it to continue capturing share from legacy providers and position itself as the go-to solution provider for businesses. As MQ reaccelerates its growth post-FY24, I expect valuation to rerate accordingly, driving the stock upwards.

Business description

MQ is a cloud-based, open-API platform for modern card issuing and payment processing. Simply put, MQ’s APIs enable businesses to take advantage of MQ’s connections with financial institutions and card networks when developing both digital and physical card programs. As an example, DoorDash (DASH) can use MQ to make unique payment cards that give customers a new way to pay. You may find more of MQ solutions here. The value that MQ brings to the table is well evident in its financial performance, where revenue has grown 5x since FY19 from $143 million to $761 million in LTM2023. MQ also has a very strong balance sheet with net cash of $1.29 billion as of 3Q23.

Long growth runway

I think the biggest bullish point for MQ is that there is an extremely long growth runway ahead. With its transition from a traditional card-issuing firm to a cloud-native, open-AI platform that supports a wide range of embedded finance use cases, I believe MQ is well-positioned to grow in the long term. The reason is that I believe the transition has greatly broadened MQ TAM to appeal to more conventional and large-scale clients, such as Walmart (WMT), who were seeking to provide their customers with more cutting-edge financial services. As such, I continue to see a long runway for TAM expansion and volume growth given MQ’s strong product moat and the trend to shift away from traditional financial institutions.

On the product moat, this is an inherent competitive advantage that MQ has over legacy providers as MQ’s platform is cloud-native. This means that it is a lot easier for customers to access the MQ platform via MQ’s APIs. This makes it easy for developers to write powerful code in short periods of time. In other words, this significantly reduces the time-to-market for developers, allowing them to roll out the product within a short period of time and giving them more time to reiterate the product based on real-world feedback. This is a strong advantage, as the world we live in today is going to get a lot more competitive in terms of product development, especially with the advent of AI. In my opinion, the first one to have his or her product on the market will have a significant first-mover advantage. On the contrary, legacy issuer processors will not be able to match MQ because their entire system is built on legacy infrastructure. As such, I expect players like MQ to continue capturing share from legacy issuer processors.

One more push-demand factor is that customers in today’s fast-paced digital world want their financial products and services integrated into everything they do. Therefore, more and more marketplaces (Uber, Grab, Shopify, etc.) are looking to provide banking, insurance, and payment services to their users. In the long run, I think more businesses will start offering customers modern fintech solutions like BNPL, digital wallet capabilities, and other payment services, and the increasing adoption of embedded finance by market big players like Shopify and Amazon will drive this trend. As one can imagine, the potential TAM is extremely huge. Based on Grandview Research, the global embedded finance market is valued at $65 billion in 2022 and is expected to grow by 32% from 2023 to 2030.

During the quarter, we signed a deal with a marketplace offering financial management tools. The customer approached Marqeta about launching a demand deposit account tied to their debit card for their user base offering cashback to help repay student debt. Company 3Q23 earnings

A structural tailwind that will help MQ in the long run is the increasing demand from consumers for fintech solutions. In my view, service providers like MQ should be well-positioned to profit as customers increasingly turn away from conventional banks and embrace fintech solutions. I believe the pandemic significantly raised the appeal of fintech solutions, as almost everything banking needs can be done via the phone. Long gone were the days where consumers needed to queue up at the bank to open an account or receive payments. This ties back to my point above regarding MQ’s platform. Fintech solution providers and banks that are looking to address these trends will need platforms like MQ.

Two examples of embedded finance deals, we signed in the quarter our company is looking to use embedded finance to create a better customer experience and keep funds within the ecosystem. Company 3Q23 earnings

Profitable growth is possible

A major concern regarding MQ is when it will turn profitable. As of 3Q23, the business has not generated any profits yet. I think there are multiple drivers in place that will turn margins profitable eventually (management is targeting an adj EBITDA margin of >20% in FY28). To start, current cohorts should keep growing as clients add more features, like credit, to their programs. Since credit programs typically have higher gross profit take rates than debit programs, this has a positive mix-shift impact. Second, in response to the increasing demand for embedded finance solutions, MQ has revised its go-to-market strategy. With the new strategy’s emphasis on selling multiple products with a more generalist approach, I anticipate significantly improved unit economics as a result of these changes. In comparison to the previous strategy of focusing on a single product with multiple specialists, this one requires a much smaller sales force because each salesperson can sell any product. Large enterprises typically use a broader suite of products when looking for embedded finance solutions, so the new strategy should also improve sales conversion.

Relationship with Block stays in tact

One of the business risks with MQ is that the relationship with Block might not get renewed. In a positive development, MQ extended the previous Cash App agreement, which was announced last quarter, for another year and renewed its agreement with Block’s Square debit card program until June 2028. The new agreements also establish MQ as Block’s default provider for issuing processing in all existing and future markets, which is a huge deal that should deepen the ties between the two companies.

Valuation

May Investing Ideas

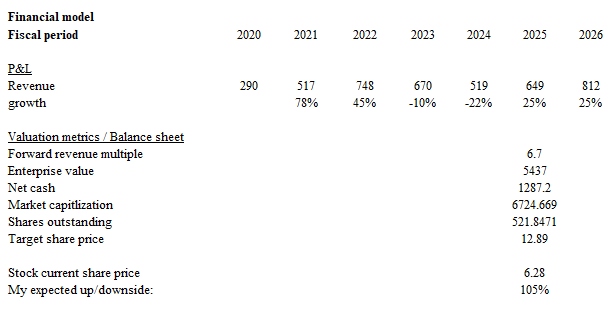

I believe the upside is attractive here if one can hold on to the stock over the medium term. The current valuation is likely depressed because of the weak near-term guidance in FY23 and FY24. But I believe growth is set to accelerate post-FY24 as management guides due to the strong secular tailwind. My model’s assumptions are based on management’s guidance. The reason I am using a forward revenue multiple is because meaningful profits will only be generated in FY28 (>20% adj EBITDA margin, as management guided). As MQ re-accelerates growth, I believe the market will value MQ using its historical average forward revenue multiple. Moreover, by FY26, MQ should have turned profitable (management guided FY26 adj EBIDA margin of mid-single to low-double digits percentage). That should drive a re-rating in multiples as well, now that the concern regarding profitability is out of the way.

Risk

SQ is a large portion of MQ’s revenue, and if the business relationship between the two turns sour for whatever reasons, it will significantly impact MQ’s growth runway and its business size. In addition, although demand for MQ’s suite of digital issuing and process solutions has grown rapidly, demand and growth rates could slow if the macro situation turns for the worse.

Conclusion

I believe MQ presents a compelling investment opportunity due to the strong secular tailwinds, hence, I am recommending a buy rating. With a cloud-native platform and a wide-reaching product moat, I believe MQ is well-positioned to capture market share from legacy providers. Regarding profitability, I expect drivers like credit program expansion and a revised go-to-market strategy will drive margins upwards eventually.

Read the full article here