")

Meta Platforms (NASDAQ:META) recently released Q4 earnings, and the results were excellent. Meta’s revenues surpassed estimates by nearly $1B, surging by roughly 25% YoY. Meta also announced robust guidance, its first quarterly dividend, and increased its buyback program by $50 billion. There is little not to like about Meta’s earnings report, and its stock surged by 15% after hours to over $450. It’s difficult to imagine, but Meta’s stock hit a low of $88 just fourteen months ago. So, what do you do with a stock up by 400% (fivefold) in a little more than a year?

Get Ready To Buy The Dip

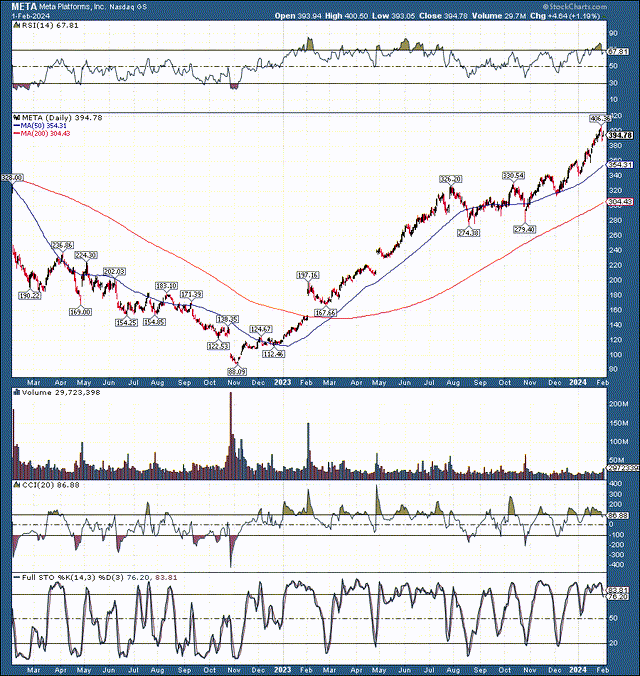

META (StockCharts.com )

I pounded the table on Meta’s stock around the lows in 2022, saying it was one of the best buys of the decade. However, I did not expect its share price to quintuple in about a year. I sold Meta too early after “only” about a 100% gain. While I rotated into other high-quality stocks that have appreciated considerably, in hindsight, I should have kept my Meta shares.

The run-up in Meta’s stock has been spectacular, and the company has the numbers to back it up. Still, with the RSI surging above 70 again, Meta is technically overbought, and we may get a pullback to take some of the froth out of its stock price soon. I will re-enter Meta’s stock if I have an opportunity in the $380-$420 buy-in range.

The Options Plan

- If long here, we can implement the covered call strategy, selling the 3/15/24 $460-$500 call options for solid premiums as we advance.

- If we don’t have shares but want to get long, we can implement the wheel option strategy, selling the 3/15/24 $380-$420 cash-covered puts for healthy premiums in the coming sessions.

Meta Earnings – Nothing Short of Spectacular

Meta reported Q4 revenues of $40.11 billion, a beat of $940 million, and a 24.77% YoY increase. Meta reported $134.9 billion for the year, a 16% YoY rise. Family daily active people (“DAP”) was 3.19 billion for December 2023, an 8% YoY increase. Family monthly active users (“MAP”) was 3.98 billion, a 6% YoY increase. Facebook’s daily active users (“DAUs”) were 2.11 billion, a 6% YoY increase.

Meta also provided outstanding guidance of $34.5-$37 billion for Q1 2024 vs. the $33.87 billion consensus estimate. Meta’s board also approved a $0.50 quarterly dividend and a $50 billion increase in its buyback program.

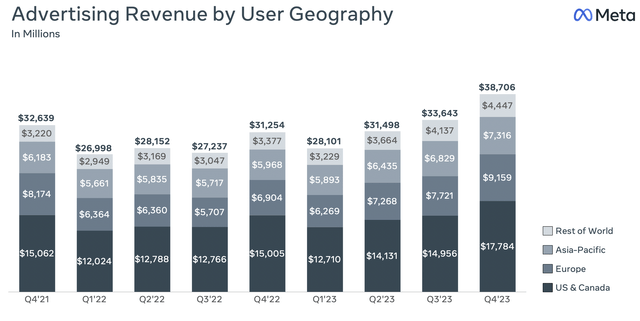

ad revenues (static.seekingalpha.com )

Meta’s ad revenue surged to a new record of about $38.7 billion, a 24% YoY increase. We see record revenues in all geographic areas, especially in the U.S. and Canada. Ad revenue should continue strengthening as the global economy improves and interest rates decline throughout 2024 and next year.

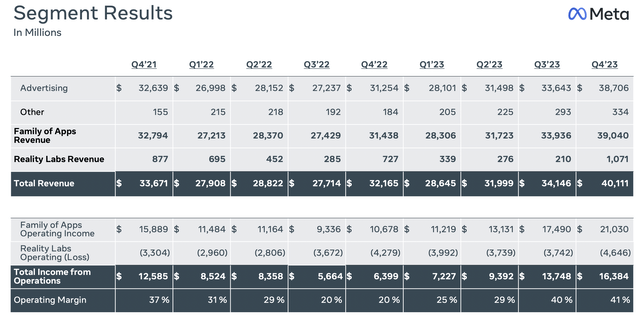

Segment revenues (static.seekingalpha.com )

Meta’s profitability has increased considerably over the last year. Meta’s family of apps operating income nearly doubled from the same quarter one year ago. Reality Labs revenues have spiked to over $1 billion for the first time. Meta’s operating income came in at 41% vs. just 20% a year ago, even bettering its high profitability phase of 37% in Q4 2021. This dynamic illustrates that Meta has done an excellent job cutting costs and focusing on profitability, a constructive trend moving forward.

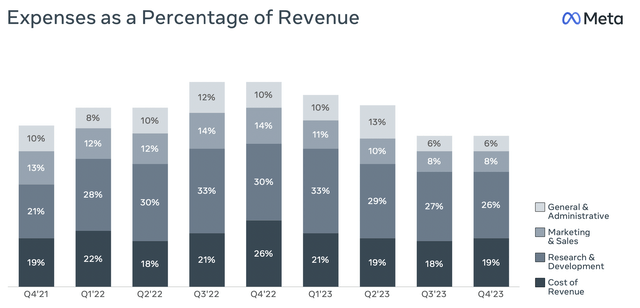

Expenses (static.seekingalpha.com )

Expenses as a percentage of revenues look excellent. The cost of revenues is back down to about 19%, much lower than the 26% in the same quarter a year ago. Also, we see a record low (for the recent period) of 6% and 8% general, administrative, and marketing and sales expenses. This dynamic illustrates that Meta can become more efficient and profitable with scale.

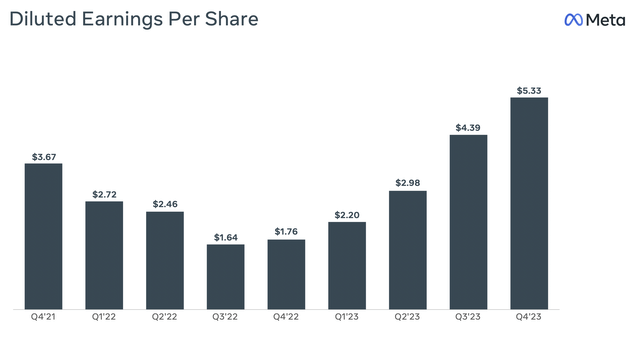

EPS (static.seekingalpha.com )

As a result of effective cost cutting, increasing ad revenues, and other constructive factors, EPS is surging to new records. This positive trend should continue in future quarters and years due to Meta’s dominant, market-leading social media position and massive potential in the Metaverse and AI.

EPS Outperformance Should Continue

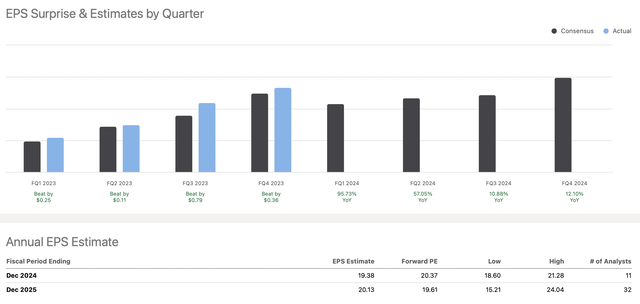

EPS vs. estimates (SeekingAlpha.com )

Consensus estimates were for $13.39 in EPS for 2023. Yet, Meta reported $14.90 instead. This dynamic represents an outperformance rate of about 11%. 2024 consensus estimates are for $19.38. However, if Meta beats census figures by a similar margin, it can earn approximately $21.15 instead. Also, 2025 consensus EPS figures are for $20.13. If we apply a similar 11% beat rate, Meta could earn about $22.35 in 2025.

Also, in a more bullish case scenario, Meta’s EPS could be in the $23-$24 range next year. Therefore, even with its stock price around $450, Meta may only be trading around an 18-20 forward P/E ratio now. This valuation is relatively inexpensive for a company in Meta’s dominant, market-leading position, capable of producing significant growth and improving profitability in the future.

Where Meta’s stock could be in future years:

| Year | 2024 | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 |

| Revenue Bs | $160 | $177 | $202 | $226 | $253 | $281 | $309 |

| Revenue growth | 18.5% | 11% | 14% | 12% | 12% | 11% | 10% |

| EPS | $21 | $23 | $26 | $31 | $36 | $41 | $47 |

| EPS growth | 40% | 10% | 13% | 19% | 16% | 15% | 14% |

| Forward P/E | 21 | 22 | 23 | 23 | 22 | 21 | 20 |

| Stock price | $483 | $572 | $713 | $828 | $902 | $987 | $1,070 |

Source: The Financial Prophet

I’m projecting modest revenue growth in future years. Meta’s sales could expand more than expected due to advancements in the Metaverse, AI, and other capabilities. Meta’s core ad business could also grow more than expected due to an improving economy, lower interest rates, and other favorable variables in future quarters. Therefore, we may see higher sales and EPS growth, enabling multiple expansions to 20-25 or higher as market conditions improve in the coming years. Therefore, Meta’s stock could hit $1,000 or more by 2030 or sooner, making it a solid long-term buy, especially on a pullback to the $380-$420 level.

Risks To Meta

Despite my bullish projections, Meta faces risks. Bearish macroeconomic factors could cause Meta’s growth to slow down, and a recession would be highly damaging to Meta’s earnings. Also, there are higher cost risks due to reality labs and other costly research projects. There is also the risk of Facebook or other family platforms losing users or experiencing lower-than-expected/stagnant growth. Regulatory concerns may also materialize, weighing on the share price. Investors should examine these risks and others before investing in Meta stock.

Read the full article here