")

I discussed my bullish view on MongoDB (NASDAQ:MDB) stock in my initiation article, highlighting their strengths in the document-based database market. They released their Q4 FY24 result on March 7th, delivering 27% revenue growth and 86.1% adjusted operating profit growth. I am still confident that MongoDB will deliver above 20% revenue growth over the next few years. I reiterate the ‘Strong Buy’ rating with a fair value of $475 per share.

Healthy Atlas Consumption Growth

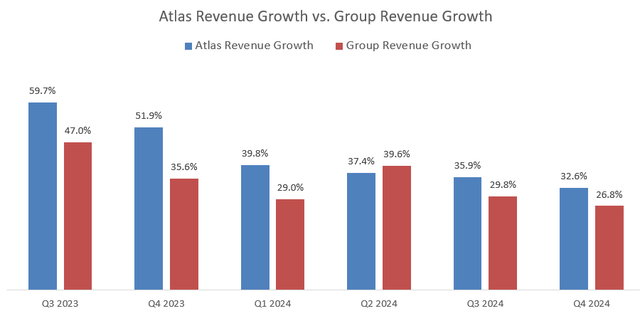

As highlighted in my initiation report, MongoDB Atlas provides cloud-based database services, with a consumption-based pricing model. In Q4 FY24, Atlas accounted for 68% of group revenue, with revenue increasing by 32.6% year-over-year, surpassing the group revenue growth. Clearly, MongoDB Atlas has becoming a significant growth driver for MongoDB.

MongoDB Quarterly Results

The strong Atlas growth is contributed by the following factors:

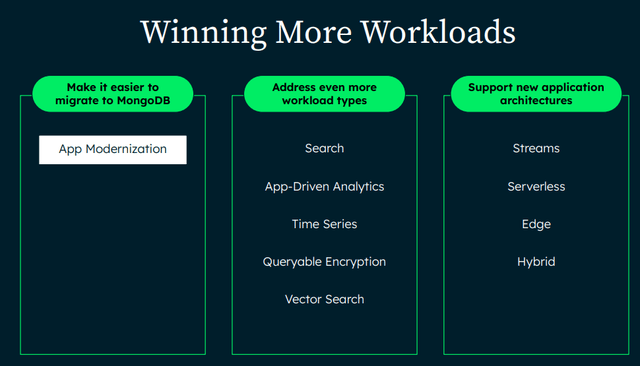

Atlas’s growth is primarily tied to data consumptions, meaning its expansion depends on the number of workloads running on the Atlas database. MongoDB has excelled in winning more workloads in the public cloud market. As illustrated in the slide below, MongoDB has developed App Modernization tool that enables developers to seamlessly migrate data from legacy database to cloud-based ones. Additionally, MongoDB has been expanding search engines, data analytics, and AI-based vector search, which will support a wide range of workloads.

MongoDB Investor Presentation

Maximize Market Research forecasts that the cloud database market will grow at a CAGR of 24.85% from 2023-2029, driven by cloud computing and AI workloads. To perform AI machine learnings, workloads have to be mitigated to cloud, and the legacy on-premises databases have to be converted into cloud database like MongoDB. The fast growth in the cloud database market will support MongoDB’s expansion of their Atlas database over the next few years, in my view.

Lastly, MongoDB supports both structured data and unstructured data, and the database platform can be running on both on-premises and in the cloud. The unified platform simplifies data management for enterprises, providing a significant technology advantage over legacy database services.

In short, I anticipate MongoDB Atlas will sustain their growth momentum in the near future.

$80 Million Growth Headwinds in FY25; Mid-Teen Growth in Headcount

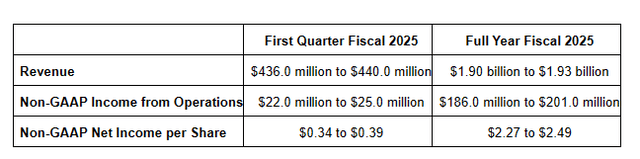

The company guides around 20% revenue growth in FY25 and approximately 25% decline in non-GAAP income from operations, as shown in the table below.

MongoDB Q4 FY24 Earnings

For topline growth, MongoDB is going to encounter $80 million in growth headwinds. As disclosed over the earnings call, MongoDB generated $40 million in revenue in FY24 from unused Atlas commitments; however this revenue stream will diminish in FY25, due to changes in the incentive structure, resulting in reduced commission payments for upfront commitments. Consequently, there will not be any upfront commitment revenue in the future in my view.

In addition, MongoDB’s non-Atlas business recognized $40 million from multi-year license deals in FY24, and their management anticipates non-Atlas revenue growth moderating in FY25. As such, there are a total of $80 million in growth headwinds in FY25, resulting in 4.7% of year-over-year revenue growth headwind.

The $80 million in revenues represent high-margin businesses as disclosed by their management; therefore, it creates additional margin headwinds for the company.

On the cost side, MongoDB’s headcount grew by 9% in FY24, and the company anticipates mid-teen growth in FY25. The new hirings are primarily for their Atlas business and salesforce expansion. The rising headcount poses another challenge for their operating margin in FY25.

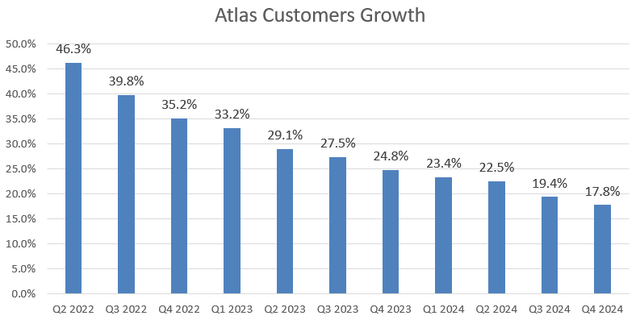

I believe the $80 million revenue headwind will be one-time issue and it won’t occur again in FY26. I anticipate their Atlas business will grow by around 35% in FY25, supported by the growing number of Atlas customers, increasing workloads in the Atlas cloud, stable database consumption patterns, and expanding salesforce capabilities.

MongoDB Quarterly Results

As such, Atlas is expected to attribute 23.8% to the topline growth in FY25, as per my calculation. Taking into account the $80 million revenue headwinds, the non-Atlas revenue is forecasted to decline by 10% year-over-year and the group revenue is predicted to grow by 20% in FY25, as per my estimates.

Redburn Atlantic downgraded MongoDB’s stock due to concerns about rising storage costs for enterprises. Their thesis does not make too much sense to me. It is true that with the rising demand of cloud computing, data analytics and AI workloads, enterprises are facing rising storage costs. However, compared to legacy proprietary database vendors like Oracle (ORCL), MongoDB’s consumption-based pricing model enables enterprises to gradually scale up their database architecture. In addition, enterprises do not need to purchase expensive proprietary hardware to run these traditional database systems; instead, MongoDB’s cloud database doesn’t require enterprises to have huge initial capital expenditures.

Valuation Update

I assume 20% revenue growth in FY25 as discussed above. As the $80 million revenue headwind will be gone in FY26, I anticipate the company returning to a 25% growth. The normalized growth rate aligns with the market growth forecasted by Maximize Market Research.

I anticipate their non-Atlas revenue as a percentage of group revenue will gradually decline over the next decade, as more workloads will be migrated to the cloud, and MongoDB has allocated more resources towards Atlas related businesses.

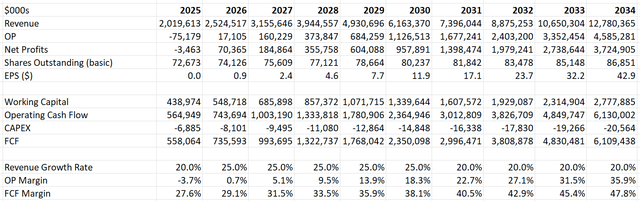

For a mature database company, it is quite realistic to achieve more than 35% of operating margin, as demonstrated by Oracle before FY20. I estimate MongoDB will grow their operating expenses by 18% year-over-year, and their operating margin will be expanded to 35.9% by FY34.

MongoDB DCF – Author’s Calculation

MongoDB’s beta is 2.09 according to SA, a pretty high level. The WACC is calculated to be 12% with the following assumptions:

-Risk free rate: 4.26%. 10-Year U.S. Treasury Yield

-Market risk premium: 7%; cost of debt: 7%

-Debt: $1.14 billon; Equity: $1 billion

With these assumptions, the enterprise value is calculated to be $33 billion in the model. Adjusting the cash and debt balances, the fair value is estimated to be $475 per share.

Key Risks

Although cloud database is poised for grow rapidly in the near future, there are many competitors in the new market, such as major Hyperscalers, Oracle, MariaDB, MemSQL, DataStax, Couchbase etc. Similar to other fast-growing technologies, many existing companies are likely to go out-of-business in the future, leaving only a few key players to dominate the cloud database market. MongoDB has the first move advantage over other small players; however, it is important for investors to monitor Oracle and IBM’s initiatives in their cloud-based database business.

Furthermore, MongoDB allocated 28.7% of total revenue towards their SBC in FY24, slightly lower than 29.7% in FY23. The high SBC payout is typical for high-growth tech companies; however, the company does need to reduce the SBC ratio over time in order to satisfy investors and improve their operating margins.

Conclusion

I view the $80 million revenue headwind as a one-time issue for MongoDB, and I am quite optimistic about their future growth in cloud-based database market. MongoDB is a high growth company with a quite high beta, and the stock is suitable for growth portfolios. I reiterate the ‘Strong Buy’ rating with a fair value of $475 per share.

Read the full article here