")

Covering the aerospace and defense industry as well as related industries, I don’t just focus on the industry giants but also pay close attention to smaller companies as well as companies that might be successfully executing a turnaround to uncover value. Sometimes, there indeed is value and sometimes it turns out the risk-reward profile is not attractive for investment. In this report, I will be adding Mynaric (NASDAQ:MYNA) to my coverage to assess whether the company provides any value for shareholders. I will do so by discussing the company’s activities, end market, enabling technology, and applications as well as a more fundamental look at the company including a risk assessment.

Mynaric: A Laser Communications Specialist

Based in Germany, Mynaric develops laser communication technology, which is primarily used in the aerospace and defense industries. Currently, demand for laser communication and satellite service primarily comes from government agencies seeking to establish space-based communication networks. With that in mind, keeping an eye on the US Space Force and Space Development Agency budgets is important. Combined, the Space Force and SDA have a $26.3 billion budget which was 7% higher than requested, and with increasing demand for space-based solutions including high-speed secure military communications, we could see budgets increase even more. Mynaric, although small in terms of revenues, could also benefit from increasing defense budgets and technological advancement in other geographical markets such as Europe and increased demand for space-based communication solutions for commercial purposes.

What Are The Advantages Of Laser Communications?

Laser communications allow for higher transfer speeds of data and are over 300 times faster than fast Radio Frequency or RF wave communications. The technology has a smaller beam compared to RF, which makes intercepting signals difficult and perhaps even impossible with current technology allowing for secure data transfer and communications making it extremely suitable for military communications. On the commercial end, laser communications contrary to RF beams license free meaning that unlike RF beams no separate license for each beaming location needs to be purchased.

All in all, the technology behind laser communications would allow for high speed and secure communications which could enable new technological applications such as predictive management for commercial airplanes, laser fast exchange of data and communication for military and commercial purposes, earth observation and connecting remote areas. I would also with the current development of advanced hypersonics, faster communications for hypersonic weapon systems and hypersonic defense becomes more of a necessity than “nice to have”. The next-generation fighter jet will likely also be more equipped even better with battlefield integration systems and be paired with drones for which laser communications could also prove to be essential.

Who Are The Customers Of Mynaric?

Mynaric AG

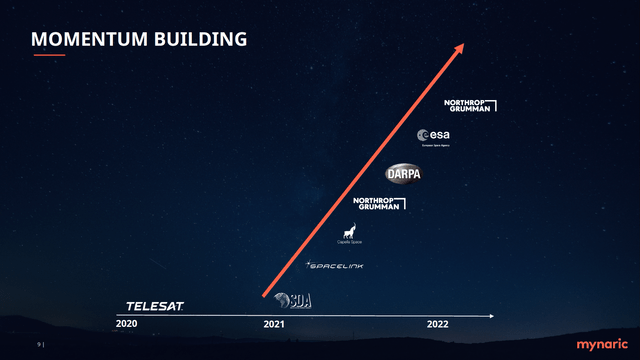

The customer base for Mynaric potentially is a mix of commercial and government customers with an addressable market of $20 billion, but for now is mostly focused on government customers. Northrop Grumman (NOC), which I analyzed in a separate report, is among the customers of Mynaric and recently placed an order valued $25 million supporting the SDA’s Tranche 2 Transport Layer-Beta program. In November, the company announced a $6 million contract with an unidentified customer for the CONDOR Mk3 terminals for which verification was completed in September this year. Other customers include DARPA, SDA and ESA from which it received funds to investigate terabit speed connectivity. Commercial customers include Northrop Grumman and Capella Space both of which provide products and services to the government or government agencies. SpaceLink also signed with Mynaric in 2021 and L3Harris (LHX) made a strategic investment in the company last year. So, we see a lot of high profile customers and also note the real-life examples of high speed communications enabled by StarLink used in the military operations of Ukraine in the Russo-Ukrainian War.

Revenues Are Not Immediate For Mynaric

Mynaric AG

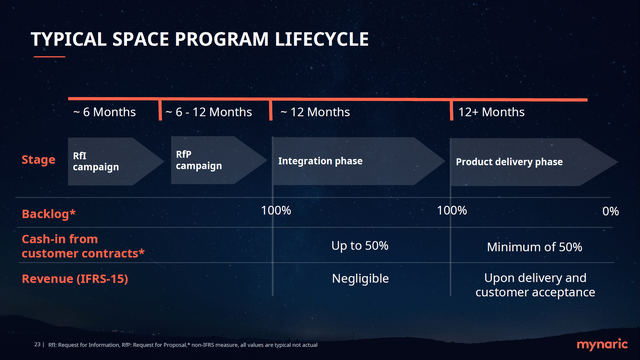

Mynaric has a lot of potential if we see the use cases and enabling nature in end markets. The reality, however, is that the translation to revenues can be rather slow. In the initial phase which can be up to 18 months the request for information and request for proposal are issued followed by an award at which stage an order can be added to the backlog. After the award, there is an integration phase in which phase Mynaric can receive up to 50% of customers’ pre-delivery payments which is not recognized as revenue or in the best case a small portion. The balance of the cash is due on delivery and customer sign-off at which case an order is removed from the backlog and recognized as revenue. The entire process from Request for Information to revenue recognition realistically could take years similar to what we see for defense and commercial airplane programs.

Mynaric AG

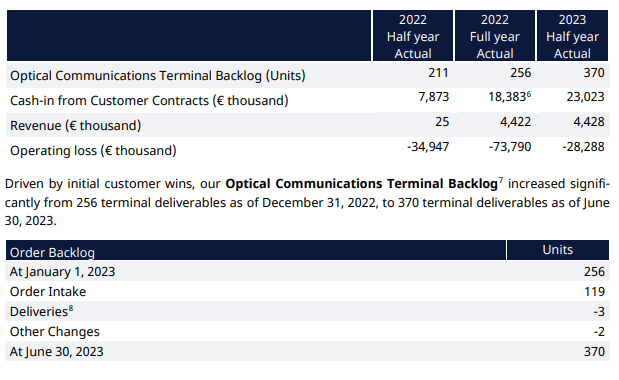

Mynaric currently is working on securing contracts and ramping production, which allows better cost amortization and also includes typical learning curve effects improving the unit costs for production of its communication terminals. Continued additions to the backlog allow for higher production rates allowing significant reduction in unit costs driven by better cost amortization and scale advantages. So, the backlog is key for the company right now. In the first half of 2023, backlog grew to 370 units up almost 50% from the start of the year and cash-in from customers increased by slightly less than $5 million and by more than $15 million year-over-year. Important to note is that the H1 2023 revenues already exceeded FY2022 revenues.

Mynaric Could Be An Attractive Take Over Candidate

Depending on whether regulatory approval can be obtained I view Mynaric as a valuable acquisition target for Northrop Grumman and L3Harris Technologies. Northrop Grumman is already a customer of Mynaric, so they know the value the business adds to theirs. With activities in hypersonics, hypersonics defense and the battlefield airborne communications node or BACN, I could see why Northrop Grumman at some point would be interested in acquiring the entire business. L3Harris Technologies could also be interested in the company as it is also active in missile defense solutions as well as critical communications for which laser communications could provide value. What should be kept in mind is that Mynaric operates under a license from the German Aerospace Center or DLR to commercialize the high speed connectivity effort.

In the aerospace communication segment, we do see that ViaSat completed the acquisition of Inmarsat earlier this year and CACI completed the acquisition of SA Photonics in 2021 and Eutelsat and Oneweb agreed to combine last year. So, there is a lot of M&A activity in the communication space.

Risks for Mynaric: Competition And Dilution

Mynaric AG

While it might seem like Mynaric operates a high burden market with an exceptional product, to me it seems like the technological concept is not ultracomplex. I have studied aerospace engineering and in second year courses, you are already being trained in sizing satellites including commercial equipment sizing and budgeting, so I have little doubt that aerospace giants do possess the knowledge to provide air and space-based laser communications. The list of companies that Mynaric identifies as potential or existing competitors is long. Companies such as Amazon and SpaceX could opt to develop their own laser communications solution and in the aerospace sector, the list of competitors is long with names such as Airbus (OTCPK:EADSF), Thales (OTCPK:THLEF), Ball Aerospace, General Atomics and Honeywell (HON). Furthermore, QinetiQ (OTCPK:QNTQF) and Hensoldt (OTCPK:HAGHY) already market laser communication solutions while the company has already identified that established aerospace giants could enter the market and compete with Mynaric more successfully due to their existing and longstanding relationship with customers. So, Mynaric can hardly be called unique in that sense or uniquely equipped. With a lower burden than some might expect, potentially acquiring the company will also be a function of timeline and development costs of in-house built laser communication technology and equipment compared to acquiring Mynaric.

Another risk I see for shareholders is shareholder dilution. Since 2017, the share count of Mynaric has doubled and in September 2023 the company filled a prospectus allowing the company to sell American Depositary Shares representing 5 million ordinary shares. So, the dilution risk is real.

Furthermore, the company could be subject to risks that render the company unable to manufacture communication terminals at a low enough cost to turn a profit or provide a cost competitive product. These risks include the current challenges in the aerospace supply chain and higher labor and material costs. From demand side, although not expected, demand could be insufficient to support higher production rates which would allow faster learning and stronger cost reduction and better cost amortization. All of these elements could eventually force the company to issue even more stock.

Is Mynaric Stock Worth Your Consideration?

The Aerospace Forum

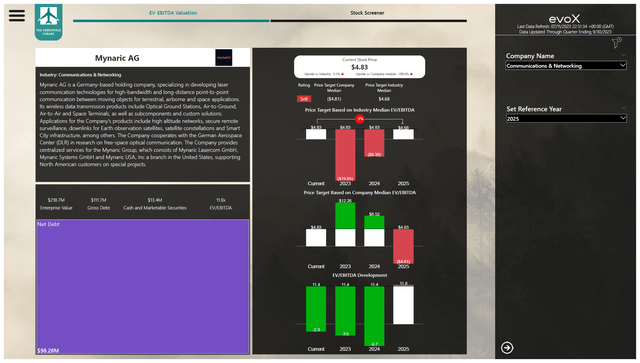

Mynaric stock is one that is hard to judge. There are two reasons for that. The first is that the company has been working on maturing its technology. It was spun off from the German Aerospace Center to commercialize and in that process IPO’d in Germany in 2017 but has not been profitable since. Consequently, the company’s EV/EBITDA has been negative for some years now and the company EV/EBITDA as a result is not an extremely useful way to value the business and you could even say that EV/EBITDA assessments are not the right way to do it either. Disregarding the company median EV/EBITDA and the Sell score which is also partially driven by company EV/EBITDA valuation, the industry EV/EBITDA would suggest that Mynaric stock is more or less fairly valued incorporating shareholder dilution this year including the sale of 20 million ADS and a combination of debt and further dilution in the years to come.

So, we do see fair value for the stock but not a strong buy case driven by attractive risk-reward mechanisms.

Conclusion: Mynaric Attractive Business, Unattractive Value For Shareholders

I have little doubt that Mynaric will at some point be profitable, the real question is how much shareholders will be diluted in the process and what the competitive landscape will look like by that time. So, it is hardly an attractive buy as there are just too many uncertainties. However, we do see Mynaric gaining traction which is a big positive and there is a reason why the company can count on interest in its products from high-profile customers. So, I would mark the stock as a hold or potentially a very speculative buy as the upside could potentially over the longer term be more rewarding than the downside risk.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here