The Tortoise Midstream Energy Fund (NYSE:NTG) is a closed-end fund aka CEF that specializes in investing in midstream energy partnerships and corporations. This is an attractive position for anyone who wants to include a midstream energy company in a tax-deferred retirement account or some similar tax-advantaged vehicle because it overcomes all of the tax problems that can accompany including these companies in such an account. That is nice because midstream partnerships typically enjoy remarkably stable cash flows in any economic climate and boast very high yields, which is attractive for anyone seeking to earn income in their retirement. Midstream partnerships cannot usually be added to a retirement account without risking tax problems, but this fund gets around that problem by dealing with the tax issues on the fund level. It can easily be purchased in any account that you desire just like a corporation.

As regular readers are no doubt well aware, we last discussed this fund back around the end of August. Its performance since that date has been relatively decent as the fund’s share price is up 0.37%:

Seeking Alpha

Admittedly, that share price performance is not going to turn anyone’s head, but it is still much better than a loss. The fund did not make a distribution payment during the time period in question, so the chart above reflects the actual performance that the shareholders experienced.

With that said though, the fund does naturally pay a very high yield to its shareholders. This is to be expected considering the high yields possessed by the assets that it invests in. As of the time of writing, the fund boasts an 8.80% yield, which compares pretty well to some of the other midstream funds on the market:

|

Fund |

Current Distribution Yield |

|

Tortoise Midstream Energy Fund |

8.80% |

|

First Trust Energy Income and Growth Fund (FEN) |

8.33% |

|

First Trust MLP and Energy Income Fund (FEI) |

8.10% |

|

Kayne Anderson Energy Infrastructure Fund (KYN) |

10.32% |

|

ClearBridge MLP and Midstream Fund (CEM) |

8.57% |

|

ClearBridge Energy Midstream Opportunity Fund (EMO) |

8.13% |

Thus, investors are clearly not sacrificing yield by purchasing this fund relative to some of its peers. However, a solid yield alone does not make a fund a good investment so let us investigate further and see if it makes sense to purchase this fund today.

About The Fund

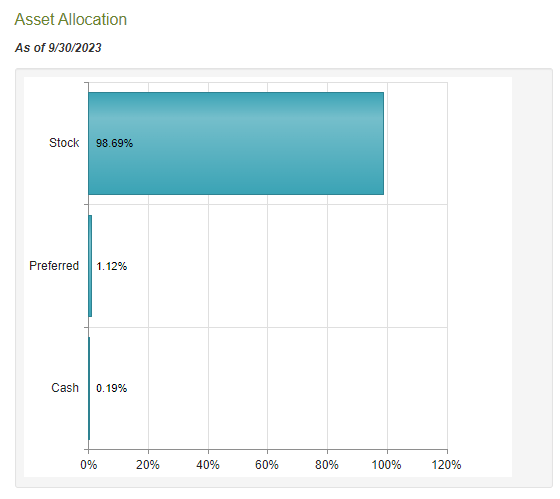

According to the fund’s website, the Tortoise Midstream Energy Fund has the primary objective of providing its investors with a very high level of total return. This makes a great deal of sense considering what this fund is investing in. As we can see here, currently 98.69% of the fund’s assets are invested in common equities:

CEF Connect

As I pointed out numerous times in the past, common equities are by their very nature total return vehicles because investors purchase them both for the income that they provide through distributions and dividends as well as the capital gains that should accompany the growth and prosperity of the issuing company. However, midstream companies are unlike most common stocks in the fact that they deliver most of their returns via direct payments to the shareholders.

For example, let us consider the Alerian MLP Index (AMLP), which tracks an index of midstream partnerships. Over the past five years, the index is down 14.11% but anyone that bought the index five years ago and simply held it is actually up 31.32%:

Seeking Alpha

This is because the distributions that were paid by the companies in the index were more than sufficient to offset the price decline. Admittedly, some people may not want to invest in something that has experienced a price decline over the past five years, but ultimately it is the total return that matters, not simply what the price of an asset does.

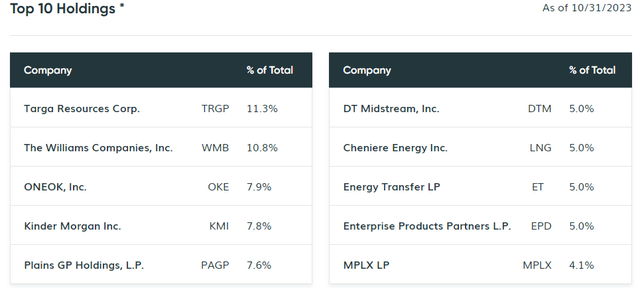

The Tortoise Midstream Energy Fund includes a number of companies that the index does not, however. This is because the Alerian MLP Index only includes those companies that are specifically structured as master limited partnerships, but this fund can also include midstream corporations. We can see this quite clearly by looking at the largest positions in the fund. Here they are:

Tortoise Ecofin

Targa Resources Corp. (TRGP), The Williams Companies (WMB), ONEOK (OKE), Kinder Morgan (KMI), DT Midstream (DTM), and Cheniere Energy (LNG) are all structured as corporations, not partnerships. As such, none of these companies will be included in the Alerian MLP Index. Many of them still act somewhat like master limited partnerships, however, but they have lower yields in general. The remainder of the companies in this list are master-limited partnerships, and all of them are included in the Alerian MLP Index.

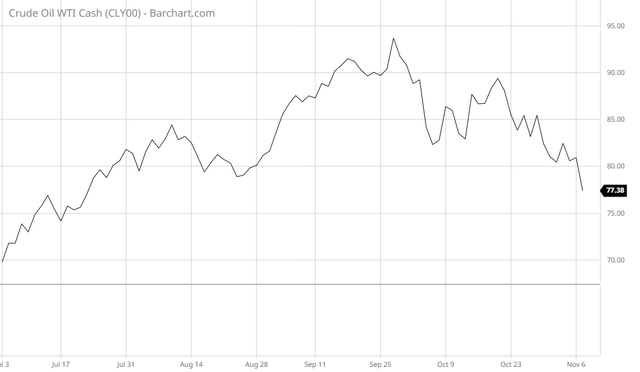

As everyone reading this is no doubt well aware, energy prices started to rise in mid-July, although they have moderated in the past few weeks. However, as we can see here, West Texas Intermediate crude oil is still up since July 1:

Barchart

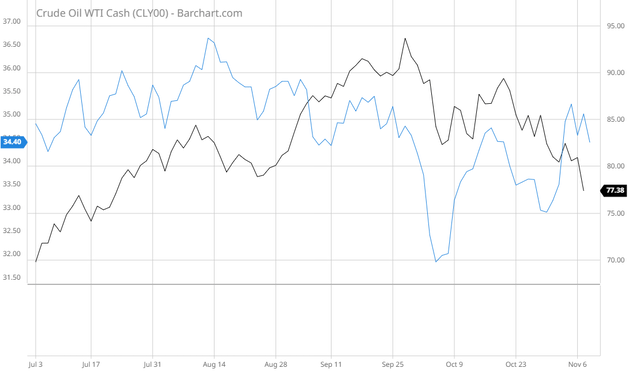

This fund’s price performance has somewhat correlated with crude oil, but the correlation is fairly weak:

Barchart

This is a departure from what we have seen in the past, as midstream companies frequently exhibit a certain degree of correlation to energy prices. However, the cash flows of these companies are not really affected by such price fluctuations. In a previous article, I provided a brief summary of the business model employed by most midstream companies:

Basically, the company enters into long-term contracts with its customers. Under these contracts, the company provides transportation for the customer’s crude oil, natural gas, and other hydrocarbon products. In exchange, the customer compensates the midstream company based on the value of resources that are transported, not on the value of them.

The midstream companies that comprise the bulk of this fund’s portfolio operate more like toll roads than energy producers. Their cash flows do not typically vary much based on energy prices. In fact, as I pointed out in a few articles published to Energy Profits in Dividends back in 2020, the pandemic had virtually no impact at all on the cash flow of most midstream partnerships. The market price of many of these companies certainly fell during 2020 but the actual financial performance of the companies was virtually unaffected. In fact, the only real impact that energy prices would have on the cash flows of a typical midstream company is that it could affect the production plans of the upstream customers, which could ultimately have a negative impact on volumes. That is a very long-term scenario though, since midstream contracts typically last for many years and include minimum volume commitments.

There have been relatively few changes since the last time that we discussed this fund. In fact, the only significant change was that Magellan Midstream Partners was removed and replaced with MPLX. This is quite obviously because Magellan Midstream Partners merged with ONEOK and no longer operates as an independent company. It is also almost certainly one of the biggest reasons why ONEOK’s shares represent a substantially greater percentage of the fund than they did back in August. Other than that, there have been relatively few changes to the fund’s portfolio, other than the weightings of several stocks changing over the period. This could be explained simply by one company outperforming another in the market and does not necessarily mean that the fund is actively trading its assets. With that said though, the fund’s annual turnover is 72.67%, so clearly it is engaging in active trading. That is a higher turnover than many other common equity funds too, which could be pushing up the fund’s trading costs.

Leverage

As is the case with many closed-end funds, the Tortoise Midstream Energy Fund employs leverage as a method of boosting its returns beyond that of any of the assets in the portfolio. I explained how this works in my last article on this fund:

In short, the fund borrows money and then uses this money to purchase the common equity of master limited partnerships and midstream corporations. As long as the purchased assets have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As the fund is capable of borrowing at institutional rates, which are considerably lower than retail rates, this will usually be the case. It is important to note though that this strategy is somewhat less effective today with rates at 6% than it was two years ago when rates were basically 0%. This is because the difference between the borrowing rate and the yield that the fund can obtain from the purchased asset is a lot narrower than it once was.

However, the use of debt in this fashion is a double-edged sword. This is because equity boosts both gains and losses. This could, therefore, be one reason why the Tortoise Midstream Energy Fund tends to decline much more than the index during periods of market weakness. As such, we want to ensure that the fund is not employing too much leverage because that would expose us to too much risk. I usually like to see a fund’s leverage remain under a third as a percentage of its assets for this reason.

As of the time of writing, the Tortoise Midstream Energy Fund has levered assets comprising 22.02% of its portfolio. This is actually an increase from the 21.68% leverage that it had the last time that we discussed it. This is confusing, because if the fund’s price went up then its leverage should have gone down unless it borrowed more money.

We can quickly explain this by having a look at the fund’s portfolio performance. While the fund’s share price went up since August 23, 2023, the fund’s net asset value actually went down:

Seeking Alpha

Thus, the fund’s share price has outperformed the portfolio itself since the publication of my prior article on this fund. This explains why the fund’s leverage went up, as leverage is a function of net asset value and is independent of the share price.

With that said though, this fund’s leverage is in line with most other midstream funds and is significantly lower than the leverage ratio that we see in funds in other sectors, so we probably do not need to worry about it too much. The trade-off between the risk and reward appears to be acceptable at the present time.

Distribution Analysis

One of the biggest reasons why investors purchase shares of midstream companies is because these companies tend to have very high yields. As we saw earlier in this article, these companies deliver most of their total investment returns in this fashion. The Tortoise Midstream Energy Fund collects the dividend and distribution payments made by these companies and combines it with any capital gains that it manages to realize from the appreciation of their equity securities. The fund even applies a layer of leverage to boost the effective portfolio yield beyond that of the underlying assets in the portfolio. It then pays out the profits from these investment activities to its shareholders, net of the fund’s own expenses. As such, we might expect that this fund will have a very high yield itself.

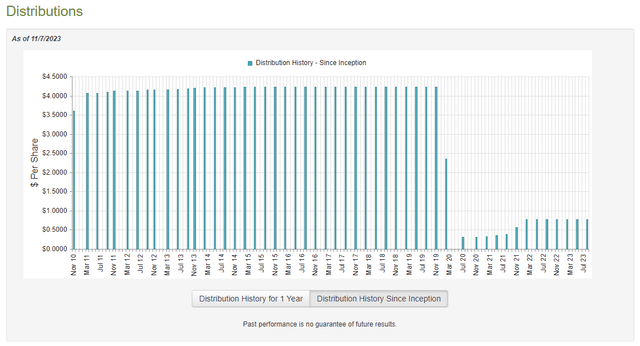

That is certainly the case. The Tortoise Midstream Energy Fund pays a quarterly distribution of $0.77 per share ($3.08 per share annually), which gives the fund a reasonably attractive 8.80% yield at the current price. Unfortunately, this fund has not been especially consistent with respect to its distribution over the years, as we can see here:

CEF Connect

As we can see, the fund cut its distribution substantially back in 2020, but it had a pretty good track record prior to that year. This is something that could prove to be a turn-off to those investors who are seeking a safe and secure source of income to use to pay their bills. However, it is understandable considering that the losses that the fund took that year reduced its ability to sustain its distribution at the prior level. Indeed, the losses incurred by just about anything invested in the traditional energy level were very severe that year and both the fund and most midstream companies went into capital preservation mode to keep their balance sheets intact. Fortunately, we can see that the fund has made some efforts to raise its distribution now that the sector has recovered.

The fund’s past is not necessarily the most important thing for anyone who is purchasing the fund today. After all, anyone who buys the fund right now will receive the current distribution and will not be affected by anything that happened in the past. As such, we should have a look at the fund’s finances and see how sustainable the current distribution is. That is the most important thing for our purposes today.

Fortunately, we do have a relatively recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund’s most recent financial report corresponds to the six-month period that ended on May 31, 2023. As such, it will not include any information about the fund’s performance over the past five months or so. This is a bit disappointing because the energy sector in general performed better during the past five months than it did during the first half of the year, but at the same time this report will give us a decent idea of how well the fund handles somewhat challenging environments. That is a better indicator of the quality of a fund’s management team than how well it performed in a relatively friendly market.

During the six-month period, the Tortoise Midstream Energy Fund received $8,006,707 in dividends and distributions from the assets in its portfolio. The fund also reported $176,544 in interest from its investments. However, some of this money came from master limited partnerships, so it is not considered to be investment income for tax purposes. As such, the fund only reported a total investment income of $4,251,225 during the period. The fund paid its expenses out of this amount, which left it with $1,043,923 available for shareholders. As might be expected, this was nowhere close to enough to cover the distributions that the fund paid out, which totaled $8,255,696 during the period. At first glance, this may be concerning as the fund clearly did not have enough net investment income to cover its distributions.

However, the fund has other methods through which it can obtain the money that it needs to cover the distribution. For example, it might be able to realize some capital gains through the sale of appreciated securities. In addition, it received some money from the master limited partnerships in its portfolio that are not considered investment income for tax purposes but still clearly represents money that can be paid out to the shareholders. Unfortunately, the fund generally failed at this task during the period. It reported net realized gains of $9,419,378 but these were offset by $39,183,425 net unrealized losses during the period. Overall, the fund’s net assets declined by $36,975,820 after accounting for all inflows and outflows during the period. This is certainly not what we really want to see in terms of distribution sustainability.

With that said, the fund’s net investment income and net realized gains were more than sufficient to cover the distributions. This is important because the only reason that the fund’s net assets declined during the period was because of the unrealized losses. Unrealized losses can quickly be erased the moment that the market turns bullish, so they are not necessarily a big deal. Overall, this fund does appear to be okay and can afford the distribution.

Valuation

As of November 7, 2023 (the most recent date for which data is currently available), the Tortoise Midstream Energy Fund has a net asset value of $41.15 per share but the shares currently trade for $34.40 each. This gives the fund’s shares a 16.40% discount at the current price. That is an incredibly large discount and certainly represents a reasonable price to pay for any fund. However, the shares have had a 17.17% discount on average over the past month. As such, it might be possible to obtain a better price by waiting, but realistically the current price represents a very reasonable entry point for this fund.

Conclusion

In conclusion, the Tortoise Midstream Energy Fund is one way that midstream partnerships can be added to a retirement or other tax-advantaged account without dealing with tax problems. The fund appears to do a reasonable job at what it does, as its performance is acceptable and its yield competitive with most of its peers. It also has an attractive valuation and appears capable of covering the distribution.

Read the full article here