")

Introduction

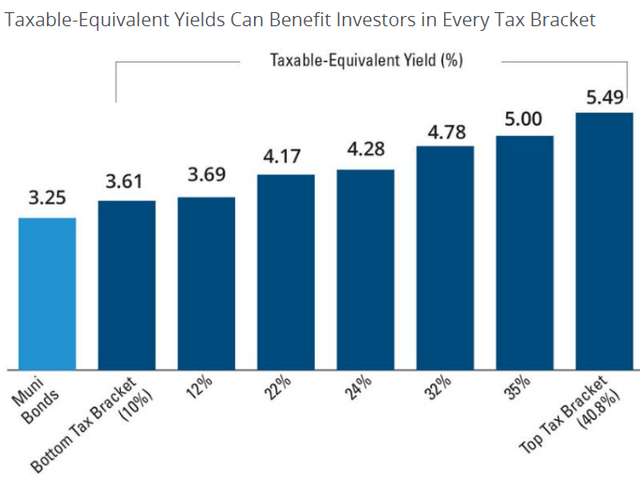

All experienced investors know owning a municipal bond avoids federal income taxes and potentially both state and local income taxes too. This is how the after-tax rate correlates to the current Federal tax rates.

hartfordfunds.com

The above chart shows what a 3.25% coupon needs to be from a taxable bond to net the same income post-federal taxes.

There are a few other benefits investors should be aware of, such as:

- Municipal bonds have a lower default rate than similarly rated corporate bonds, which increases in importance of the “Soft landing” happening.

- Municipal bonds are domestically focused, while many stocks have global exposure and are more sensitive to macroeconomic factors.

- Municipal bonds add portfolio diversification as they have a .23 correlation to US stocks and .17 to International stocks.

Municipal bond market review

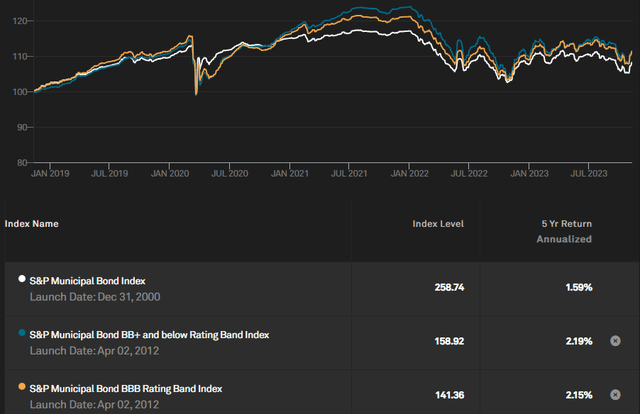

I found some indices that show how different sub-markets have done over the past five years.

spglobal.com municipal-bond-index

Investing below investment grade provided a slightly higher return over the last five years. Over the last one- and three-year periods, the BBB index turned in the best results.

This article reviews the Nuveen Municipal Value Fund (NYSE:NUV) to which I give a Hold rating p, mainly due to my concern the FOMC has more work to be done fighting inflation.

Nuveen Municipal Value Fund review

Seeking Alpha describes this ETF as:

The Fund seeks to provide current income exempt from regular federal income tax by investing in an actively managed portfolio tax-exempt municipal securities. At least 80% of its managed assets are rated investment grade; up to 10% may be rated below B-/B3 (rated at the time of purchase by a nationally statistical ratings organization (S&P, Moody’s, Fitch] or, if unrated, judged to be of comparable quality by the Fund’s portfolio team. NUV started in 1987 and benchmarks against the S&P Municipal Bond index.

Source: seekingalpha.com NUV

NUV has $1.87b AUM and has a Forward yield of 4.18%. Fees are 50bps and the CEF employs just over 1% leverage.

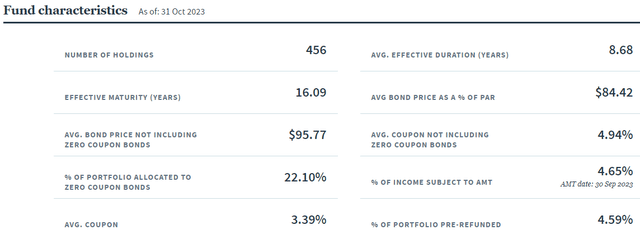

Holdings review

nuveen.com NUV

Even though this is not an AMT-free fund, very little (4.65%) of the income is subjected to that tax process. With a duration of over 16 years, one can understand the hit this CEF has taken since interest rates started climbing. That will be a big positive once the trend reverses.

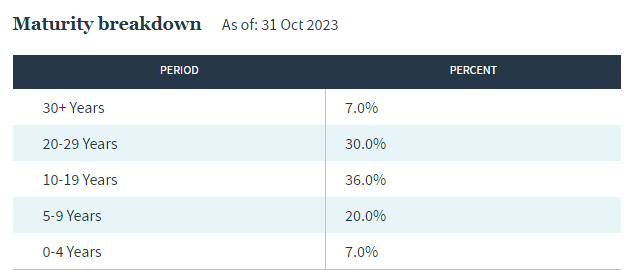

CEFConnect.com maturity schedule

While light in 30+ year maturities, NUV is well balanced across the yield curve based on its maturity allocations. With only 4% maturity over the next four years, NUV does not have much in terms of old cash to reinvest in today’s higher yields. While another 8% is Callable over the next year, that fact diminishes the odds a Call will be executed.

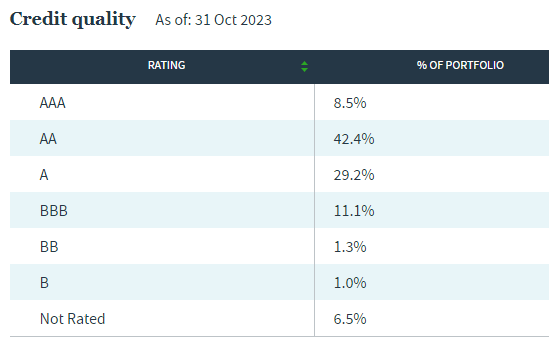

Looking at the credit ratings allocations, glad to see no bonds rated below B, but the CEF does hold just over 2% below their investment-grade mandate.

nuveen.com ratings

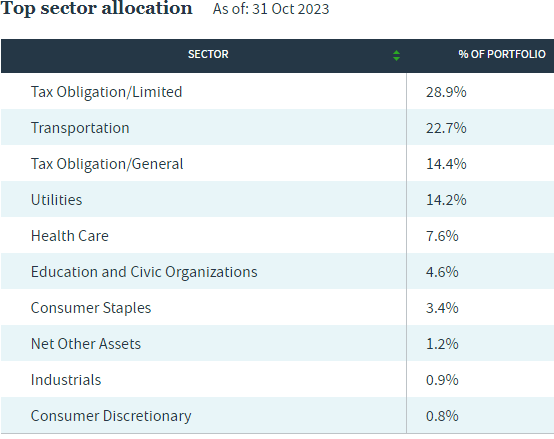

Morningstar gives NUV an “A+” average credit rating score. The types of tax-free bonds held are as follows, with over 42% dependent on tax obligations. A stable to growing economy in those states will help there.

nuveen.com sectors

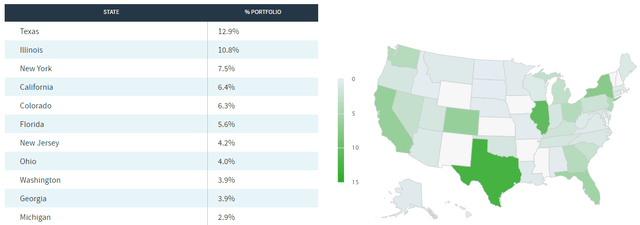

The second largest allocation, Transportation, is also tied to people moving about so a strong economy plays a part here too, thus the importance of the next table and map that shows which states have the largest allocations.

nuveen.comn states

It is important to remember the state itself is not the backer of all the allocations listed for that state, counties and cities are included in those percentages.

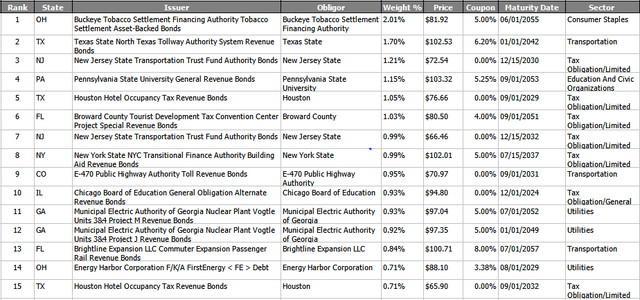

Top holdings

nuveen.com; compiled by Author

With over 450 positions, the CEF is not concentrated, with the largest single allocation of just over 2%. Unlike some data sets, Nuveen does not appear to provide Issuer-level exposure, which is great to have.

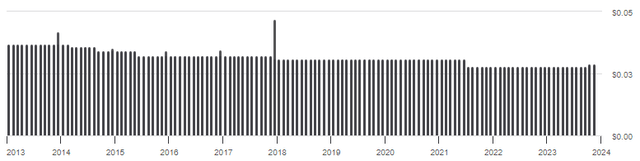

Distribution review

seekingalpha.com DVDs

After several payout cuts over the past decade, NUV recently increased the payout from a monthly rate of $.28 to $.29. A good indicator of payout stability is the CEF’s UNII coverage ratio. As of the end of September, NUV had a 99.1% coverage ratio.

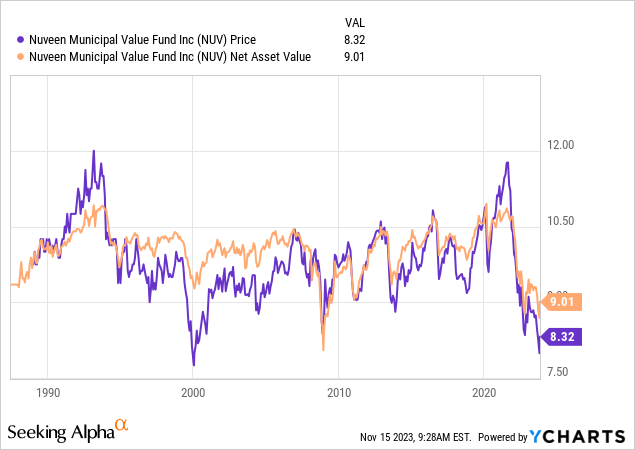

Price and NAV review

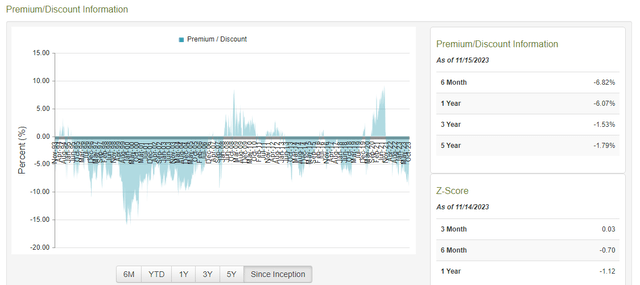

As might be expected, NUV has done extremely poorly since interest rates started climbing. Hope is increasing that “higher for longer” might not be much more than now, which should allow prices and the NAV to start climbing. The next chart shows NUV having traded at both premiums and discounts, with it currently at a 7.66% discount.

CEFConnect.com

While not the biggest spread, the current discount is hovering at the widest level since the GFC. Unlike some CEFs, it also recently traded at a high premium before the FOMC intervened in the market to fight inflation. Investors would benefit if the discount shrinks.

Portfolio strategy

Investors have multiple choices when deciding to own municipal bonds, some of which are:

- Direct ownership of individual bonds or diversify via holding a fund.

- Within funds, there are ones like NUV that use little/no leverage, and others like the Nuveen AMT-Free Quality Municipal Income Fund (NEA) that do. This gives a choice based on that factor that affects yield and risk.

- Which rating do you favor in the trade-off between yields received and risk taken? NUV focuses on the upper end of investment-grade ratings.

- If subject to high state/local income tax rates, it might be better to own a fund that only invests in bonds free of those taxes.

- If after-tax yields are not a major concern, there are taxable municipal bond funds to consider, like the Nuveen Taxable Municipal Income Fund (NBB).

- There are also funds that invest with the idea of having a low duration and thus less interest-rate risk.

Once you decide which to invest in, the hunt for choices is narrowed. Factors like managers, fees, size, and payment coverage then rise to the top in narrowing the choices down even more. Nuveen alone offers six CEFs they classify as National Investment-grade: two with no leverage, two with little leverage, and two with 40+% leverage.

PortfolioVisualizer.com

Conclusion

With the NUV CEF lagging behind Nuveen Select Tax-Free Income Portfolio (NXP) in return and risk factors, I would give NUV only a Hold rating as it is holding its own. For those sitting on a loss in their NUV holdings, taking that loss and reinvesting into NXP to remain unlevered or Nuveen Quality Municipal Income Fund (NAD) should be considered before 2024.

Read the full article here