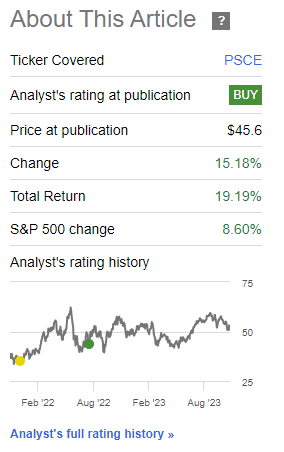

I last covered the Invesco S&P SmallCap Energy ETF (NASDAQ:PSCE) over one year ago. In that article, I argued that PSCE was a classic high-risk high-reward investment opportunity, due to its small, risky holdings, and outsized exposure to energy prices. I was bullish, on growth and valuations grounds. The fund has significantly outperformed since, in-line with expectations.

PSCE Previous Article

PSCE’s fundamentals have improved since, with the fund sporting a higher dividend, a cheaper valuation, and some momentum behind its back. I remain bullish, but the fund remains an incredibly risky investment too.

Although the fund’s 2.7% yield is respectable for an equity fund, it is probably too low for most income investors. For these, the Global X MLP & Energy Infrastructure ETF (MLPX), with a growing 5.5% yield, might be a better choice. I last covered MLPX here.

PSCE – Overview and Analysis

Index and Holdings

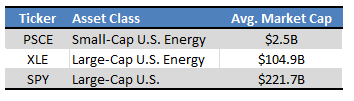

PSCE is a small-cap energy index ETF, tracking the S&P SmallCap 600 Capped Energy Index. The index first selects the 1500 largest U.S. companies, subject to a basic set of inclusion criteria. It then selects the 600 smallest companies in this group, and then selects the energy stocks within said group. It is a market-cap weighted index, with issuer caps to ensure diversification.

PSCE seems to effectively track the U.S. small-cap energy industry. The fund invests 28 different U.S. energy stocks, all relatively small corporations. Fund holdings have an average market cap of $2.5 billion, much lower than that of broader energy equity and equity indexes.

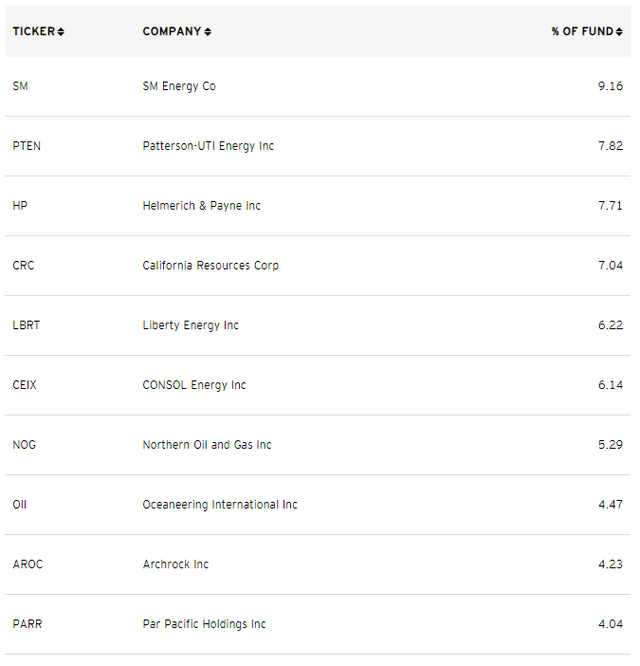

Fund Filings – Chart by Author

PSCE focuses on an incredibly narrow investment niche, which results in a incredibly concentrated portfolio. It only holds 28 stocks, with most broader equity indexes holding hundreds, some thousands. Top ten holdings account for over 60% of the value of the fund, much higher than average.

PSCE

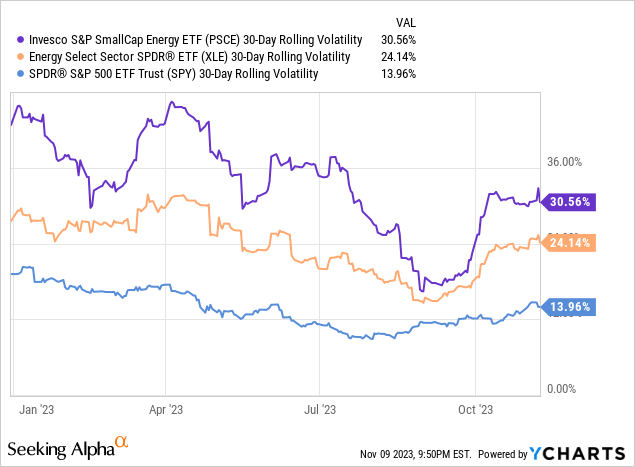

PSCE focuses on an incredibly narrow investment niche, with very few holdings, all in the same industry. Due to this, portfolio risk and volatility are both quite high, more than twice that of the S&P 500.

Data by YCharts

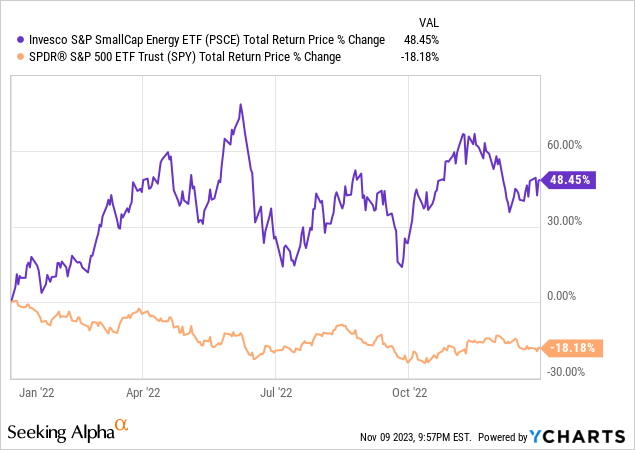

At the same time, performance does not necessarily track that of the broader equities market (too narrow for that). As an example, the fund saw significant gains during 2022, even as broader equity indexes were down.

Data by YCharts

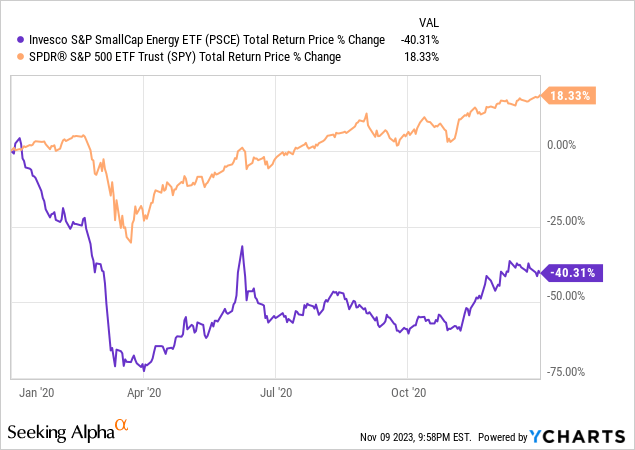

On the other hand, the fund saw significant losses during 2020, even as broader equity indexes soared.

Data by YCharts

PSCE focuses on an incredibly narrow investment niche, increasing portfolio risk and volatility, a significant negative for the fund and its shareholders.

Boosting risks further is the fact that the fund focuses on small-cap energy stocks, which tend to be significantly riskier than average.

Risk is partly operational and financial: small-cap energy companies tend to focus on more marginal oil wells, with greater operational expenses and higher break-even oil prices. Balance sheets and financials tend to be weaker too, and some smaller oil producers have reckless management teams.

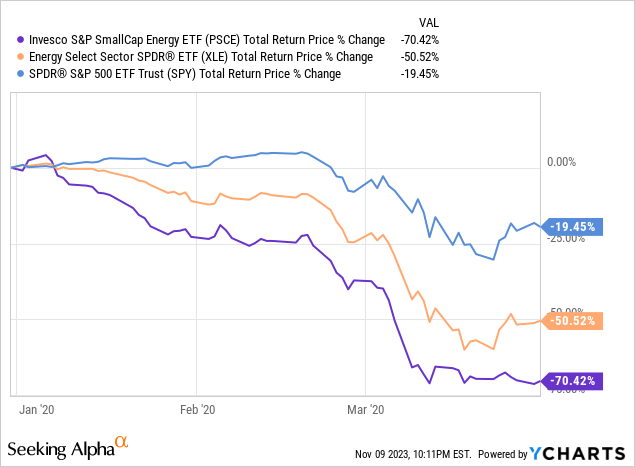

Risk is also linked to issues of market perception and risk. Investors perceive small-cap energy stocks as riskier, so these tend to face higher selling pressure when energy prices decrease or when economic conditions deteriorate. As an example, PSCE was down over 70% during 1Q2020, the onset of the coronavirus pandemic. These losses were at least partly due to market sentiment, as it was too early to tell what the long-term impact from the pandemic would be.

Data by YCharts

As should be clear from the above, PSCE is an incredibly risky fund, and riskier than most energy funds. Significant losses during downturns and commodity price crunches are to be expected. In my opinion, these issues mean that the fund is only an appropriate investment for more aggressive investors.

Stronger Energy Exposure

PSCE’s underlying holdings tend to have greater exposure to energy prices than large-cap energy stocks, for operational, financial, and market reasons.

Small-caps suffer above-average losses when energy prices are down, so see greater recoveries when these improve. Companies with higher operational expenses and break-even oil prices tend to see higher-than-average expansions in margins and EPS when oil prices increase, which feeds into higher share prices. Some of the smaller, more marginal producers can avoid bankruptcy or severe financial distress when oil prices are high, and so see high gains when this is the case. Market sentiment also plays a role, as investors are more willing to risk an investment in small-cap oil producers when oil prices are high.

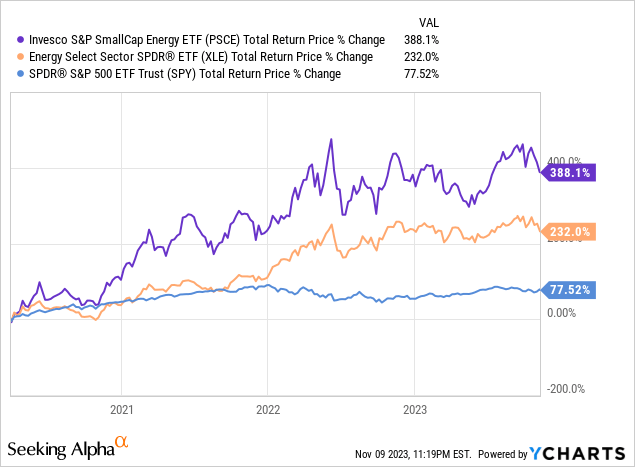

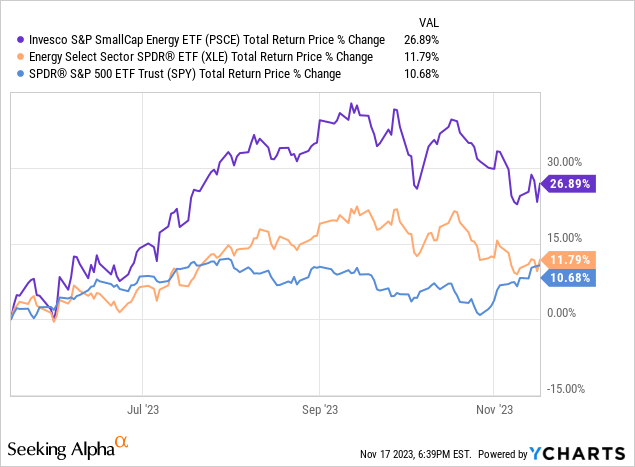

Due to the above, small-cap energy stocks tend to see above-average gains when oil prices increase, as has been the case since markets bottomed in 1Q2020.

Data by YCharts

As another example, PSCE saw higher gains the day I finished this article, on 11/17/2023.

Due to the above, PSCE seems like a natural investment for more aggressive energy bulls.

I say tend because the extreme volatility of PSCE and the energy industry makes it difficult to ascertain long-term trends. Trends sometimes get swamped by volatility, and are sometimes dependent on timing.

Cheap Valuation

Risky stocks tend to trade with discounted prices and valuations, and PSCE is no exception. Valuations are currently moderately lower than those of broader energy equity indexes, significantly lower than those of the S&P 500.

Morningstar – Chart by Author

PSCE’s cheap valuation and strong energy exposure could lead to outsized capital gains and returns for shareholders. Although these are highly uncertain, I’m optimistic for two reasons.

First, is the fact that the fund has some momentum behind its back. Returns have been very strong since the pandemic ended, and since the middle of the year. Volatility has been quite high, however, with the fund seeing several reversals too.

In any case, momentum could always continue, and is an indication that sentiment is improving.

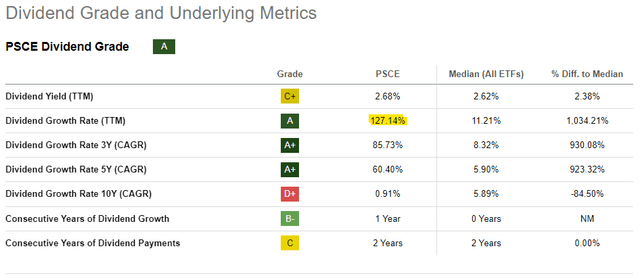

Second reason I’m somewhat hopeful of further gains, is the fact that energy stocks are returning significant cash to shareholders. Some of that cash is returned as dividends, with fund dividends more than doubling in size these past twelve months.

Seeking Alpha

Buybacks have also increased, with some companies buying back over 10% of their shares.

Dividends and buybacks are enticing to investors, which could lead to strong capital gains and returns. Even if they do not, dividends and buybacks allow companies to leverage their cheap valuations to benefit investors.

Companies with 7.7x PE ratios, average for PSCE, can deliver double-digit income to shareholders through dividends. The average S&P 500 company, with an 17.5x PE ratio, cannot. Companies with 7.7x PE ratios can also buy back double-digit percentages of their float every year, leading to double-digit EPS growth. The average S&P 500 company cannot do so.

PSCE’s underlying holdings are leveraging their cheap valuations to boost EPS, income, and shareholder returns. I believe this will lead to significant capital gains and market-beating returns moving forward, as has been the case in the past.

PSCE’s cheap valuation is a significant benefit for investors, and its core investment thesis.

Conclusion

PSCE is a small-cap energy index ETF. I’m bullish, due to the fund’s momentum and cheap valuation. The fund is much riskier than average, and might only be appropriate for more aggressive investors.

Read the full article here