")

Founded in 1969, Red Robin Gourmet Burgers (NASDAQ:RRGB) operates and franchises restaurants in North America, offering burgers, pizza, salads, and wings among other food and drink items. The majority of Red Robin’s restaurants are company-owned.

The company has struggled with maintaining profitability, and Red Robin’s debt makes the situation worse for investors. As a result, the company’s stock has plummeted within the past decade, and Red Robin isn’t currently able to distribute dividends due to weak profitability and high debt.

Ten Year Stock Chart (Seeking Alpha)

Profitability Needs to Improve with the North Star Plan

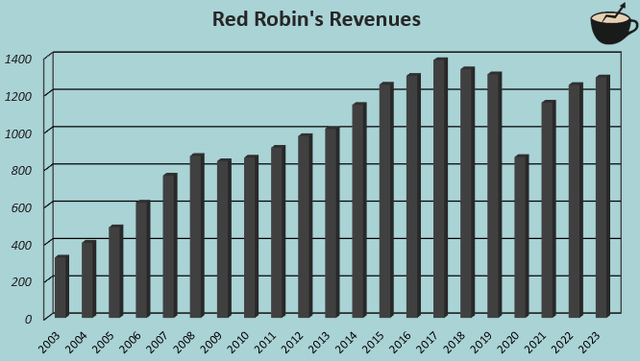

After pursuing constant restaurant growth, achieving a revenue CAGR of 10.0% from 2003 to 2018, Red Robin’s restaurant concept seems to have suffered. The company hasn’t been able to attract enough visitors in recent years, and as such, Red Robin has started to close down a significant number of stores, reducing the total count from 573 in 2018 into 511 at the end of 2022.

Author’s Calculation Using TIKR Data

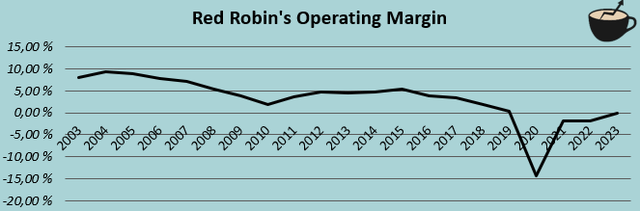

The poor performance can also be seen in profitability, being especially crucial for investors. Red Robin’s profitability has seen constant declines even from the early 2000s, and in 2023, the operating margin only stands at -0.0%; improvements in underlying operational performance are clearly needed.

Author’s Calculation Using TIKR Data

To improve profitability, Red Robin announced the North Star Plan in early 2023 including five main points. Red Robin plans to transform into an operations-focused company through an organizational structure that allows for restaurant operators’ more independent decision-making, elevates the guest experience through menu and other changes, removes costs through evaluating vendors and improving the supply chain, optimizes guest engagement through the loyalty program and other initiatives, and to ultimately drive restaurant revenues and higher unit level profitability. Red Robin expected that the improvements would be able to over double Red Robin’s adjusted EBITDA margin from 4.2% in 2022.

2024 Guidance Doesn’t Show Improvements

Red Robin’s given 2024 guidance doesn’t show continued improvements into 2024. The company expects revenues of $1250 million to $1275 million compared to $1303 million in 2023, still being down comparatively when excluding the 53rd week in Red Robin’s fiscal 2023. The middle point adjusted EBITDA margin for 2024 stands at 5.1%, showing a very modest improvement from 2022 but a year-over-year decline from 2023.

High Debt Makes Improvements Critical

Making near-term improvements more critical, Red Robin has an unhealthy amount of debt. Currently, the company’s balance sheet holds $182.6 million in long-term debt and had an extremely high $26.6 million in interest expenses. Compared to the market capitalization of $109 million at the time of writing, the amount of debt is very high, and currently breakeven operating income doesn’t provide cash flows from operations to pay off the debt.

The company has still been proactive in trying to reduce debt through selling assets; Red Robin has completed a good number of sale-and-leasebacks on the company’s properties to get liquidity for the company’s debts. For example, in March, Red Robin announced $24 million from further sale-and-leasebacks with Essential Properties Realty Trust, with the sale-and-leasebacks’ sum now adding up to $84 million in the past year. The sale-and-leasebacks are also accretive to net income as the real estate’s rent yield is lower than Red Robin’s interest rate. While these transactions have improved the debt position, a large amount of debt still remains. At the end of 2023, only $68.9 million in buildings and land combined exist on Red Robin’s balance sheet; the sale-and-leasebacks will have to come to an end quite quickly.

Valuation

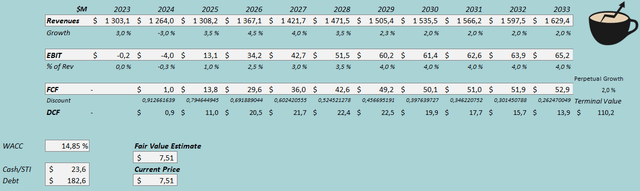

Evaluating Red Robin’s valuation is challenging, as operating income is currently near breakeven, and the company’s high debt makes net income negative. To demonstrate the valuation, I constructed a reverse DCF model where I model a scenario that the current stock price seems to price in.

It seems that the current valuation still prices in quite optimistic earnings in the future. In the reverse DCF, some growth is estimated for years after 2024 with 3.5% in 2025, 4.5% in 2026, and 4.0% in 2027 as the restaurant footprint can be expanded with improved operations. Afterwards, the growth slows down into 2.0% within a couple of years. For the EBIT margin, the DCF model estimates a ramp-up into an eventual level of 4.0% from the current breakeven level. Red Robin should have quite a low amount in capital expenditures, making the cash flow conversion very good.

I don’t believe that Red Robin’s financials are going to follow the DCF model’s $7.51 scenario in a base scenario – as can be seen from the 2024 guidance, improvements still seem to be far away from contributing into positive margins. As the priced-in scenario seems too optimistic, I don’t believe that the stock carries a good risk-to-reward.

DCF Model (Author’s Calculation)

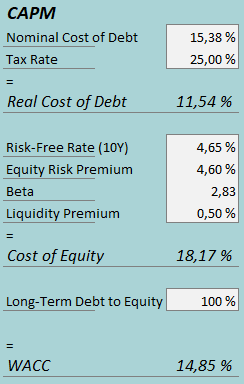

A weighted average cost of capital of 14.85% is used in the DCF model. The used WACC is derived from a capital asset pricing model:

CAPM (Author’s Calculation)

In Q4, Red Robin had $7.0 million in interest expenses. With the company’s current amount of interest-bearing debt, Red Robin’s annualized interest rate comes up to an understandably high rate of 15.38%. The company’s balance sheet is extremely leveraged compared to the current equity valuation, and I estimate a long-term debt-to-equity ratio of 100% with sale-and-leasebacks improving the debt position slightly in Q1. For the risk-free rate on the cost of equity side, I use the United States’ 10-year bond yield of 4.65%. The equity risk premium of 4.60% is Professor Aswath Damodaran’s latest estimate for the United States, updated on the 5th of January. Yahoo Finance estimates Red Robin’s beta at a figure of 2.83. Finally, I add a small liquidity premium of 0.5%, creating a cost of equity of 18.17% and a WACC of 14.85%.

Significant, But Unlikely Upside Potential

With the current market capitalization, the stock price does still show potential in the case that Red Robin is able to improve profitability very well. As Red Robin is highly leveraged, any earnings above my DCF model’s estimates immediately show a great upside for shareholders. The company’s operating margin reached 9.3% in 2004, and such a level would likely show a very great return for shareholders. My cost of capital estimate could also be too high in the scenario where the company pays down debt and profitability improves. Still, I see such improvements as unlikely until clearer improvements start to show in results.

Takeaway

Red Robin is in dire need of an improvement in profitability as the company’s debt burden continues to be large. Although sale-and-leasebacks have provided a good amount of liquidity to pay down debt, the company’s real estate doesn’t seem to be sufficient to pay the debt down. Red Robin’s earnings continue to be low, with breakeven operating income not providing cash flows to pay down the debt. While the company has laid out a plan a year ago to improve operations, an improving bottom line still can’t be seen with the 2024 guidance. Despite the stock falling into a fraction of its previous high, the valuation still seems to expect too much in my opinion. For the time being, I have a sell rating for the stock.

Read the full article here