")

A Quick Take On Reddit’s IPO Filing

Reddit, Inc. (RDDT) has filed for an $100 million in an IPO of its Class A common stock, according to an SEC S-1 registration statement, although the final figure may be materially higher.

Reddit operates a large social media website at Reddit.com.

RDDT is growing revenue and operating losses are dropping but remain substantial.

In a higher cost of capital environment, Reddit, Inc. stock performance post-IPO may be challenged until management can reach profitability, which appears a long way off.

What Does Reddit Do?

San Francisco, California-based Reddit, Inc. was founded to provide the ability for users to start and operate online communities for the sharing of opinions and information about the topics of interest to them.

Management is headed by co-founder, president and CEO Steven Huffman, who has been with the firm since 2015 and was previously co-founder and Chief Technology Officer at Hipmunk, an online commercial travel firm.

The company’s primary offerings include the following:

-

Reddit.com website

-

Community tools

-

Data services.

As of December 31, 2023, Reddit has booked fair market value investment of $2.2 billion from investors, including Advance Magazine Publishers, FMR (Fidelity Investments), Quiet Capital, Tacit Capital, Sam Altman, Tencent and Vy Capital.

The site has enabled the creation of more than 100,000 active communities, with 73 million average daily active unique visitors.

The company is also creating a directed share purchase program for qualifying users to purchase shares of the IPO at the IPO price.

Sales and Marketing expenses as a percentage of total revenue have dropped as revenues have increased, as the figures below indicate:

|

Sales and Marketing |

Expenses vs. Revenue |

|

Period |

Percentage |

|

Year Ended Dec. 31, 2023 |

28.6% |

|

Year Ended Dec. 31, 2022 |

33.8% |

(Source – SEC.)

The Sales and Marketing efficiency multiple, defined as how many dollars of additional new revenue are generated by each dollar of Sales and Marketing expense, was 0.6x in the most recent reporting period. (Source – SEC.)

Although the company is not an enterprise software firm, the Rule of 40 is a software industry rule of thumb that says that as long as the combined revenue growth rate and EBITDA percentage rate equal or exceed 40%, the firm is on an acceptable growth/EBITDA trajectory.

RDDT’s most recent calculation was only 3% as of December 31, 2023, so the firm is in need of improvement in this regard, per the table below:

|

Rule of 40 |

Calculation |

|

Recent Rev. Growth % |

21% |

|

Operating Margin |

-17% |

|

Total |

3% |

(Source – SEC.)

What Is Reddit’s Market?

According to a 2024 market research report by Mordor Intelligence, the global market for online social networking is an estimated $81.4 billion in early 2024 and is forecast to exceed $179 billion by 2029.

This represents a forecast CAGR (Compound Annual Growth Rate) of 17.1% from 2024 to 2029.

The main drivers for this expected growth are due to a strong increase in demand for online interaction among people of all ages, with especially strong growth in adoption during the recent pandemic period.

Also, organizations are increasingly tapping into social media data and related analytics to understand and interact with their customers and prospects wherever they want to connect.

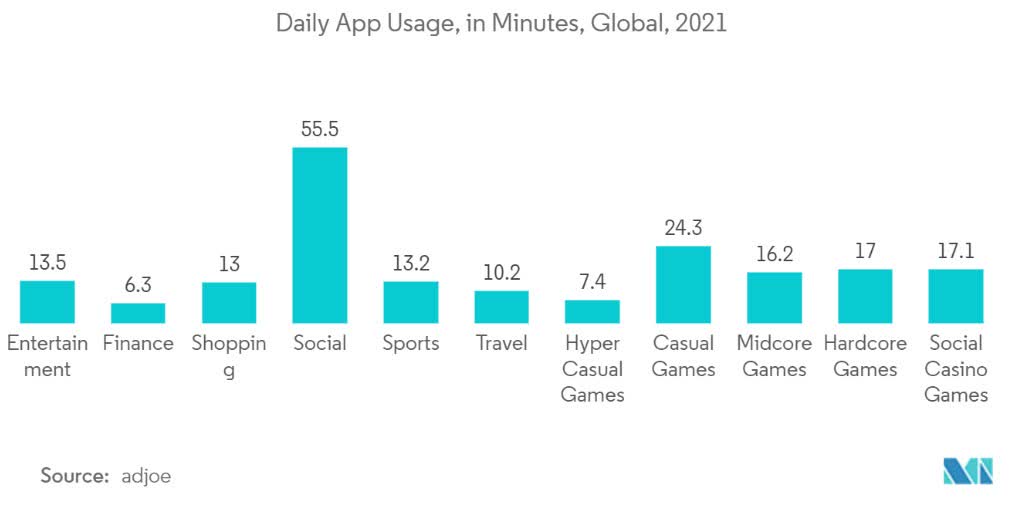

The chart below shows the minutes of daily application usage by online website/mobile app category in 2021:

Mordor Intelligence

The Asia-Pacific region accounts for the highest social media users and is expected to continue to produce strong growth in the coming years.

Major competitive or other industry participants include the following:

-

Quora

-

Facebook

-

X

-

Discord

-

Others.

Reddit’s Recent Financial Results

The company’s financial performance for the last two years is as follows:

-

Growing top-line revenue

-

Increasing gross profit and high and growing gross margin

-

Reduced operating losses and cash used in operations.

Below are relevant financial results derived from the firm’s registration statement:

|

Total Revenue |

||

|

Period |

Total Revenue |

% Variance vs. Prior |

|

Year Ended Dec. 31, 2023 |

$ 804,029,000 |

20.6% |

|

Year Ended Dec. 31, 2022 |

$ 666,701,000 |

|

|

Gross Profit (Loss) |

||

|

Period |

Gross Profit (Loss) |

% Variance vs. Prior |

|

Year Ended Dec. 31, 2023 |

$ 693,018,000 |

23.3% |

|

Year Ended Dec. 31, 2022 |

$ 561,902,000 |

|

|

Gross Margin |

||

|

Period |

Gross Margin |

% Variance vs. Prior |

|

Year Ended Dec. 31, 2023 |

86.19% |

2.3% |

|

Year Ended Dec. 31, 2022 |

84.28% |

|

|

Operating Profit (Loss) |

||

|

Period |

Operating Profit (Loss) |

Operating Margin |

|

Year Ended Dec. 31, 2023 |

$ (140,161,000) |

-17.4% |

|

Year Ended Dec. 31, 2022 |

$ (172,162,000) |

-25.8% |

|

Net Income (Loss) |

||

|

Period |

Net Income (Loss) |

Net Margin |

|

Year Ended Dec. 31, 2023 |

$ (90,824,000) |

-11.3% |

|

Year Ended Dec. 31, 2022 |

$ (158,550,000) |

-23.8% |

|

Cash Flow From Operations |

||

|

Period |

Cash Flow From Operations |

|

|

Year Ended Dec. 31, 2023 |

$ (75,114,000) |

|

|

Year Ended Dec. 31, 2022 |

$ (94,021,000) |

|

|

(Glossary Of Terms.) |

(Source – SEC.)

As of December 31, 2023, Reddit had $1.2 billion in cash, equivalents and marketable securities and $156 million in total liabilities.

Free cash flow during the twelve months ending December 31, 2023, was negative $84.8 million.

Reddit’s IPO Details

Reddit intends to raise $100 million in gross proceeds from an IPO of its Class A common stock, although the final figure will likely be significantly higher.

No existing shareholders have indicated an interest in purchasing shares at the IPO price, and it appears some shareholders may seek to sell into the IPO.

Class A shareholders will be entitled to one vote per share and Class B shareholders will have ten votes per share.

The S&P 500 Index does not allow companies with multiple share classes into its index.

Management is providing for a direct share purchase program for qualifying Reddit users, but this is optional and requires those participants to purchase shares at the IPO price.

The company is an “emerging growth company,” which means management may choose to disclose less information to shareholders.

Many such “emerging growth company” stocks have performed poorly post-IPO.

Reddit says it plans to use the net proceeds of the IPO as follows:

We intend to use the net proceeds we receive from this offering for general corporate purposes, including working capital, operating expenses, and capital expenditures. We may also use a portion of the net proceeds to in-license, acquire, or invest in complementary technologies, assets, or intellectual property. We periodically evaluate strategic opportunities; however, we have no current commitments for any material acquisitions or investments at this time.

We intend to use some of the net proceeds to satisfy tax withholding and remittance obligations related to the RSU Net Settlement.

(Source – SEC.)

Management’s presentation of the company roadshow is not available.

Regarding outstanding legal proceedings, management said the firm’s legal matters would not have a material adverse effect on its financial condition or operations.

The listed bookrunners of the IPO are Morgan Stanley, Goldman Sachs, J.P. Morgan, BofA Securities and numerous other investment banks.

Reddit Is Growing Revenue But Operating Losses Remain High

RDDT is seeking U.S. public market investment capital for its general growth and operating requirements.

The firm’s financials have produced increasing top-line revenue, growing gross profit and high and growing gross margin, and lowered operating losses and cash used in operations.

Free cash flow for the twelve months ending December 31, 2023, was negative $84.8 million.

Sales and Marketing expenses as a percentage of total revenue have fallen as revenue has increased, a positive signal; its Sales and Marketing efficiency multiple was 0.6x in the most recent reporting period of calendar year 2023.

The firm currently does not plan to pay any dividends and to keep future earnings (if any) for reinvesting into the firm’s growth and working capital requirements.

RDDT’s recent capital spending history indicates it has continued to spend on capital expenditures even as its operating cash flow has been negative.

The company’s Rule of 40 results have been disappointing, with reasonable revenue growth dragged down by operating losses.

The market opportunity for providing a social media networking platform is large and expected to grow at a strong rate of growth in the coming years.

The company faces risks including major competitors with deep pockets and the ability to incorporate new technologies such as AI functionalities to increase user engagement and bundle new services within their existing networks.

Also, AI services themselves may reduce visitor traffic by utilizing upvoted answers within Reddit communities.

Reddit has recently announced a deal to sell its data to Google for AI training purposes for $60 million.

It may strike similar deals with other AI service providers such as Microsoft, OpenAI, Xai and others, so its licensing revenue may have the potential to increase but may be a double-edge sword in the process.

The CEO and COO were provided with potentially large stock and option grants in 2023, but valuing those grants and options is difficult as they are tied to future stock performance as a public company, which is an unknown.

Unless the firm makes a substantial move toward operating breakeven, its post-IPO stock performance may be lackluster in a higher cost of capital environment.

Expected IPO Pricing Date: To be announced.

Read the full article here