")

Thesis

I wrote my last article on RH (NYSE:RH) when Berkshire Hathaway (BRK.A) exited its position and two other super investors remained invested in RH. Unfortunately, Lone Pine also exited their position in Q3, selling their 1.7 million shares. This was despite RH holding a 5% position in Lone Pine’s portfolio. So they once had a lot of confidence in the company. Other investors such as Polen Capital and First Eagle Investment also reduced their holdings significantly.

The challenging environment for the luxury furniture retailer and home furnishings company has left its mark. But just because these investors are out does not mean everyone should sell. As we have seen with Netflix (NFLX) and Meta (META), many big-name investors can be wrong. However, the situation for RH has changed for the worse, and I will explain why in the next few chapters.

Balance Sheet

RH Investor Presentation

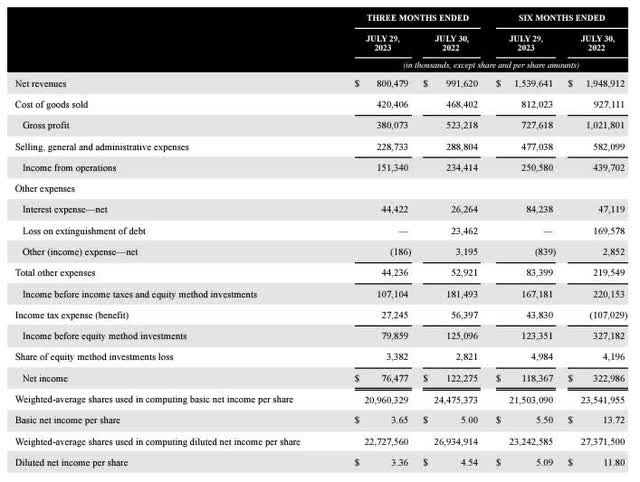

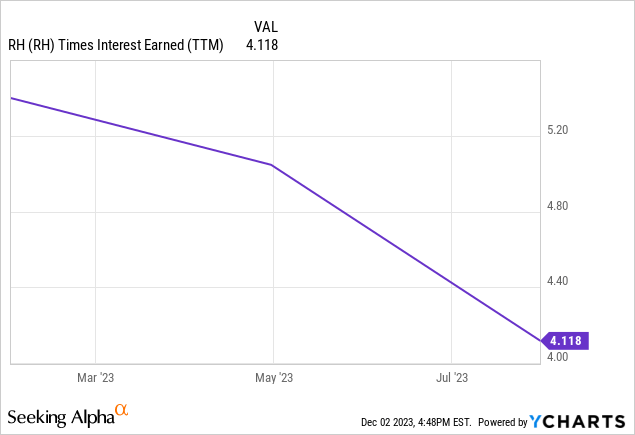

I think RH’s balance sheet used to be better. Cash decreased from $1.5 billion to $417 million, while net debt increased from $1 billion to $2 billion. As a result, interest expense increased from $47 million to $84 million due to higher interest expense on the term loan. Net sales for the last 6 months also fell sharply, from $1.9 billion last year to $1.5 billion this year. As a result, net income fell from $322 million to $118 million, representing a margin decline from 16.6% to 7.7%.

This results in a ~4x interest coverage ratio, well below the ~10x interest coverage ratio of the S&P 500. So the risk of the debt situation has increased compared to a few quarters ago, and perhaps the money spent on share buybacks could have been better used.

RH’s Capital Allocation

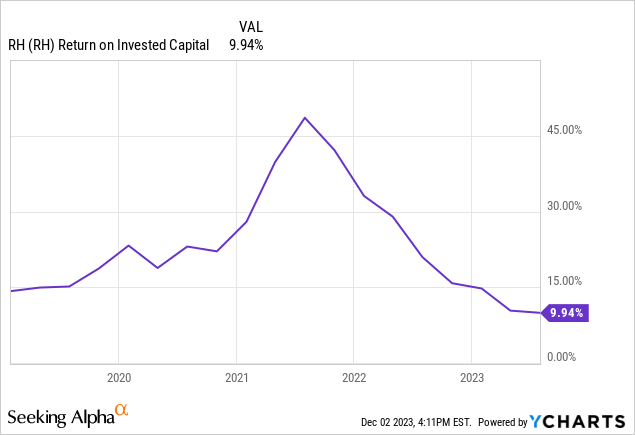

As the risk-free rate increased this year, the cost of equity also increased, resulting in a higher WACC. This combined with declining ROIC is not a good situation as the ROIC-WACC spread is narrowing. If we add in the rising debt, it is possible that RH is destroying value right now, as they could even have a negative spread. In the ideal case, the spread will still be positive, but it is likely to be only 2%. ROIC should come back as revenues and earnings normalize, but the question is how long it will take. The time until that happens could be difficult for shareholders. But since RH has shown that they can earn a higher return on their capital, now may be a good time to invest, as companies that increase ROIC tend to be some of the best performing stocks.

Reverse DCF

Author

My favorite tool to see what is priced into a stock is a reverse DCF. In this case, the base is a TTM diluted EPS of $13.22 and my discount factor is 15% because I think this hurdle rate gives us a good margin of safety. In this case, EPS would have to grow by 17% over the next 10 years to justify the current share price. A very ambitious target, but the 5Y CAGR is 26.25%, so RH has been able to beat that over the last 5 years. For a company that likes to buy back shares and sees itself as a growth company, this is within the realm of possibility. It will not be an easy task, but it is not a completely unrealistic goal, and if RH achieves it, shareholders could be handsomely rewarded.

However, should revenue and margins continue to decline, the buybacks alone will not be enough to secure the EPS growth rate going forward. Nevertheless, when RH repurchased a large portion of its outstanding shares in 2017, they picked the right time. So far, their timing on share repurchases has been impeccable. Let’s see how it goes this time.

Is There Enough Room For RH To Grow?

International expansion with Dusseldorf and Munich in 2023 and Paris, Brussels and Madrid in 2024 will likely drive revenue, but the EU is a different market than the U.S., with different tastes and a different sense of aesthetics. In addition, the differences between countries in the EU are also serious. The Germans, for example, are not known for their affinity for fashion / design, while the Italians put a lot of emphasis on it.

In addition, RH Guest Houses, RH Residences, RH Bath House & Spa offer further growth opportunities. However, as they are similar to the core business in terms of luxury and yet new, this could lead to ‘diworsification’.

Are There Significant Risks?

The $1.2 billion they used for buybacks, believing the stock to be undervalued, could pose a risk if RH’s economic situation does not improve in the next few years. Because many would argue, as some are now, that they could have used the money for something more useful, like deleveraging or investing in more future growth opportunities. Because the balance sheet is now worse than before, and as net debt has increased, the risk profile has become less favorable.

What To Watch For On The Next Earnings Call?

As Gary Friedman’s earnings calls are always entertaining, and he says what he thinks, it will be interesting to see what he thinks about when it is the right time to buy RH stock and if his opinion about a tough FY2024 has changed. In the last earnings call, his outlook for the rest of 2023 and 2024 was rather pessimistic. But companies like Pulte (PHM), which is a homebuilder, have grown their revenues this year, but with a lot of that coming from backlog. So it looks like the housing market has not been hit as hard as many feared.

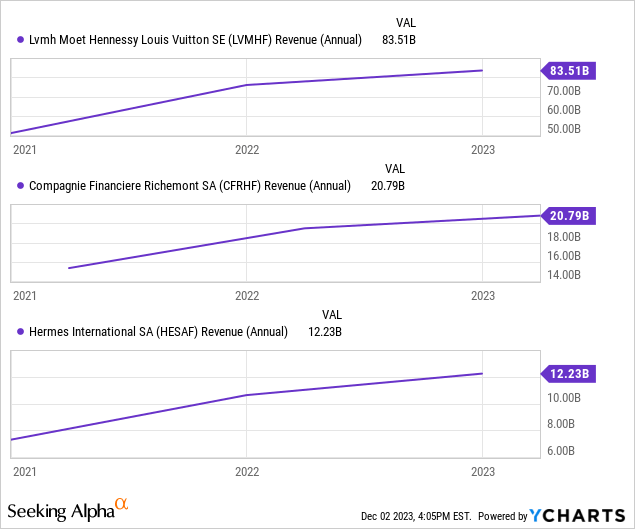

LVMH (OTCPK:LVMHF), Richemont (OTCPK:CFRHF), Hermes (OTCPK:HESAY) have also not felt the impact on their revenues as much as RH. So other luxury and real estate companies have weathered the crisis better.

Building the RH ecosystem is something interesting, so I would like to hear some comments from management about it and what the plans are for the future and if the development is going as planned.

Conclusion

RH rode a wave of easy money that really benefited luxury and real estate companies, but they have been hit hard lately. Therefore, their EPS CAGR of the last 5 years is likely to be elevated, and the next 5 years will look different. RH is definitely a good company with a polarizing CEO and an interesting idea that could work. However, I would not invest in them right now because I think there is a lot of uncertainty around the company and many different scenarios could occur. However, if margins, ROIC and revenues rebound, RH could be a very interesting long-term investment from that point forward.

Read the full article here