(NASDAQ:RCKT)")

Shares of gene therapy concern Rocket Pharmaceuticals, Inc. (NASDAQ:RCKT) have risen by 20% since we last looked at it in May of last year, as the company is poised for two potential FDA approvals. Furthermore, its one potential blockbuster rare disease gene therapy, RP-A501 for the treatment of Danon Disease, began enrolling patients in 1H23 after very encouraging Phase 1 results.

With its programs reversing disease and enough cash to get into 2026 – not counting revenue from any approved therapies – Rocket merited another look. An analysis follows below.

Seeking Alpha

Company Overview:

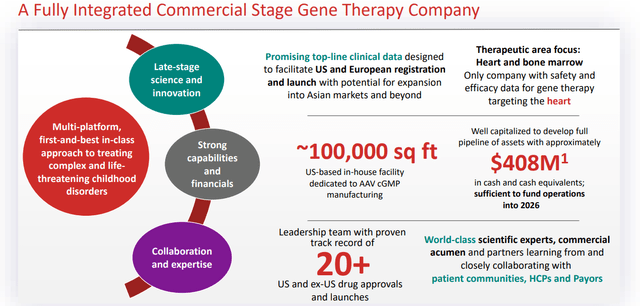

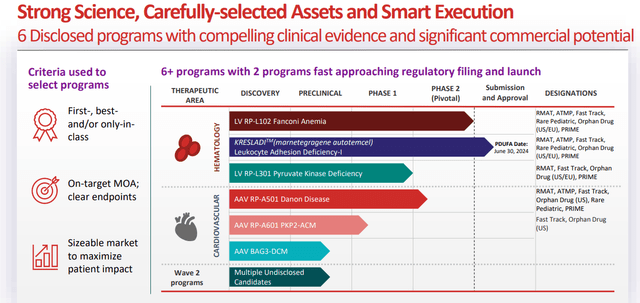

Rocket Pharmaceuticals, Inc. is a Cranbury, New Jersey-based late clinical-stage biopharmaceutical concern focused on the development of gene therapies to treat rare diseases. The company is advancing five clinical programs spawned from its two viral vector platforms, including Kresladi (marnetegragene autotemcel) for the treatment of severe leukocyte adhesion deficiency-I (LAD-I) with a recently extended PDUFA date of June 30, 2024. Rocket was incorporated in 2015 and went public via a reverse merger into failed ocular concern Inotek Pharmaceuticals in 2018, with its first trade executed at $10.86 a share. Shortly thereafter, the company conducted a public offering, raising net proceeds of $78.8 million at $13.25 a share. Rocket’s stock trades around $25.50 a share, translating into an approximate market cap of $2.3 billion.

January 2024 Company Presentation

Market

There are over 7,000 rare diseases – defined by the FDA as afflicting less than 200,000 people – impacting more than 30 million Americans and ~400,000 million worldwide. Of that number, approximately 5% have an FDA-approved therapy. When taking into consideration that ~30% of children who contract a rare disease die before their fifth birthday, the unmet need is significant. Approximately 80% of these diseases have a monogenic origin, providing a massive opportunity for Rocket and its gene therapies. This market was $161.4 billion in 2020 and is expected to more than triple by the end of the decade.

Platforms

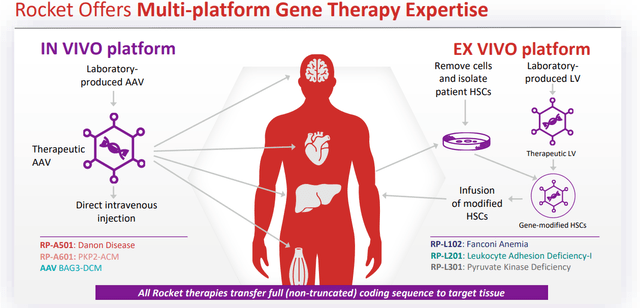

To exploit this prospect and improve the lives of many, the company employs two modified non-pathogenic viruses to penetrate cells and deliver missing and properly functioning genetic material into targeted tissues or organs: ex-vivo lentiviral vectors (LVVs), where the patient’s cells are extracted and the vector is delivered to them in a lab, with the modified cells then being reinserted into the patient; and in vivo adeno-associated viral vectors (AAVs), where the vector is injected directly into the patient. Rocket’s LVV platform is ideal for modifying hematopoietic stem cells [HSCS] to address hematologic and immune disorders, whereas its AAV platform is best suited for disorders of the heart, liver, eye, and central nervous system. Non-pathogenic viruses are well suited as delivery vehicles owing to their adeptness at invading cells.

January 2024 Company Presentation

Mostly all of Rocket’s technology originated from academia. The LLV therapies were in-licensed from Centro de Investigaciones Energéticas, Medioambientales y Tecnológicas (CIEMAT) based in Madrid, while the technology for Rocket’s AAV platform was in-licensed from UC San Diego.

Pipeline

The company’s LLV delivery platform is responsible for three clinical programs, while its AAV platform accounts for two.

January 2024 Company Presentation

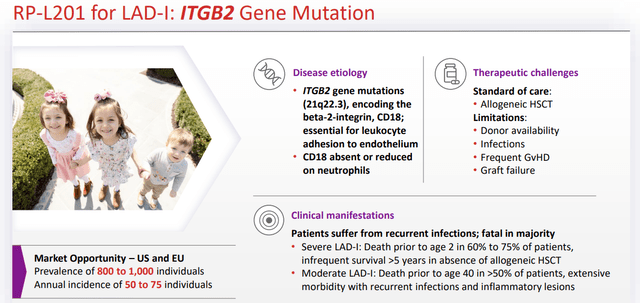

RP-L201. Its lead asset is RP-L201, which is being investigated in the treatment of LAD-1, an ultra-rare genetic disorder of the ITGB2 gene that retards CD18 expression, which in turn impairs the ability of white blood cells known as neutrophils to enter tissues where they are needed to fight infection. Without donor HSC transplantation (OTCPK:HSCT), mortality in 60%-75% of severe cases occurs by age two. The moderate form of the disease results in death prior to the age of 40 in more than half those afflicted with poor quality of life characterized by recurrent infections and inflammatory lesions. The total annual incidence of LAD-1 in the U.S. and EU combined is estimated at 50 to 75 individuals, with approximately 800 to 1,000 currently alive with the disease.

January 2024 Company Presentation

The returns for RP-L201, which is a single infusion of autologous HSCs transduced with LVV-carrying ITGB2 transgene, have been very encouraging. In a nine-patient Phase 1/2 trial, Rocket’s therapy demonstrated 100% overall survival with all nine patients exhibiting signs of disease reversal (at three to 24 months of follow-up). CD18 expression was sustained at over 10% (median 56%) versus an average of 1%< pre-treatment. Furthermore, visits to the hospital for infections and inflammation were significantly reduced (p<0.0001) and there were no serious adverse events reported.

After receiving priority review from the FDA and assigned a PDUFA date of March 31, 2024, Rocket announced that the FDA had extended the review period by three months (to June 30, 2024) to allow additional time to review clarifying information related to chemistry, manufacturing, and controls submitted by the company in response to FDA requests. RP-L201 has received fast track, rare pediatric, and regenerative medicine advanced therapy (RMAT) designations from the FDA, advanced therapy medical product (ATMP) and priority medicines (PRIME) classifications from the European authorities, and orphan drug designations from both sides of the pond. Although RP-L201 is still likely to be Rocket’s first asset across the FDA approval line, given the indication’s extremely small population, it will not significantly impact the top line, although it is likely to earn a priority review voucher, worth more than $100 million. The approval would also validate Rocket’s concepts.

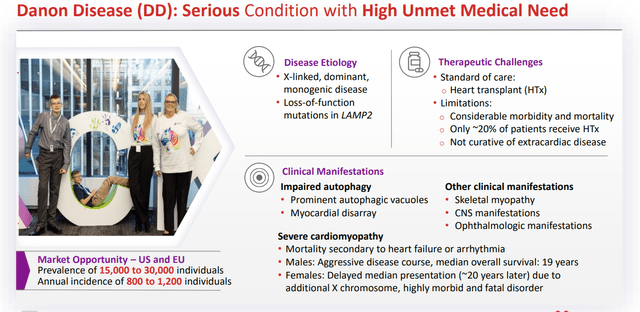

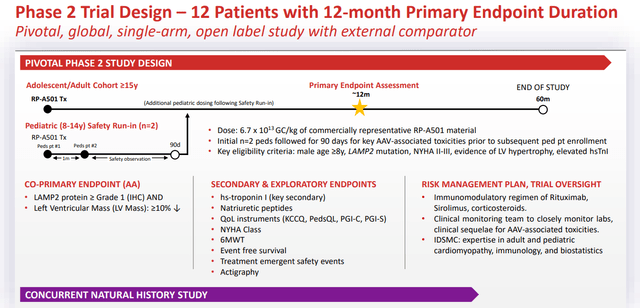

RP-A501. The distinction of Rocket’s potentially most needle-moving program belongs to its AAV therapy RP-A501, which is being evaluated in the treatment of Danon Disease, a mutation of the LAMPB2 gene responsible for the accumulation of autophagic vacuoles, predominantly in cardiac and skeletal muscle, leading to severe myocardiopathy, liver disease, and intellectual development. Male patients typically require heart transplants and die in their teens or 20s. Danon is believed to afflict 15,000 to 30,000 in the U.S. and EU, with 800 to 1,200 new cases annually. Although certainly not huge, these numbers represent a large patient population for Rocket’s rare disease approach, meaning an approval would catapult RP-A501 into blockbuster status.

January 2024 Company Presentation

After demonstrating meaningful benefit across multiple parameters, including LAMP2B gene expression and left ventricle mass reduction, in all six patients of a drawn out Phase 1 study, RP-A501 is undergoing assessment in a pivotal 12-patient Phase 2 trial that began enrollment in 2H23. RP-A501 has received orphan drug, rare pediatric, and fast track designations in the U.S.

January 2024 Company Presentation

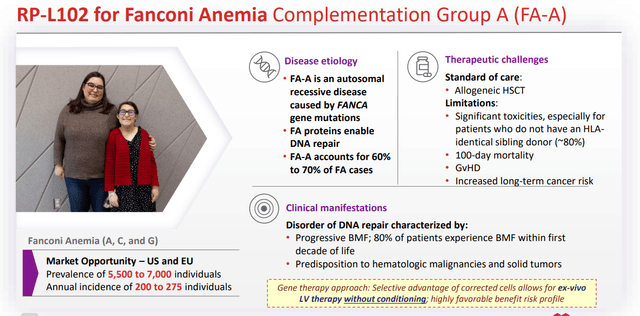

RP-L102. Not featuring as large a patient population, but ahead of RP-A501 in the clinic is PR-L102, which is undergoing evaluation in the treatment of Fanconi Anemia [FA], a very rare – 200 to 275 cases annually in the U.S. and EU – DNA-repair disorder that causes bone marrow failure, short stature, and acute myeloid leukemia, amongst other maladies. Patients with FA have a genetic defect that prevents the normal repair of genes and chromosomes within blood cells in the bone marrow. FA generally occurs in the first two decades of life and usually manifests itself in bleeding and infections as the bone marrow can no longer produce or inadequately produces platelets and blood cells.

Approximately 80% of FA patients experience bone marrow failure in their first ten years, with life expectancy of only 30 to 40 years. That translates into a ~5,500 to ~7,000 current FA population in the U.S. and EU. Approximately 60-70% of cases arise from mutations in the FANC-A gene – the others being FANC-C and FANC-G – which is Rocket’s first target.

January 2024 Company Presentation

The current standard of care for FA is HSCT, which has provided many patients with healthy platelets and blood cells. However, a lack of perfect donor matches can result in graft versus host disease (GvHD) with a 10%-15% 100-day mortality rate. Rocket’s gene therapy utilizes patients’ own stem cells, reducing the risk of severely toxic hematologic outcomes.

Results of a 12-patient Phase 1/2 trial were encouraging with seven of twelve patients at >12 months of follow-up post-infusion demonstrating sustained peripheral blood and bone marrow genetic correction, as well as mitomycin-C (a DNA damaging agent in bone marrow stem cells) resistance of 20% or more. Only one patient progressed to bone marrow failure and underwent successful allogenic HSCT. Rejection of the null hypothesis was hurdled when a fifth patient achieved increased mitomycin-C resistance greater than 10% at two timepoints between 12 and 36 months. Only one grade 2 adverse event was observed. Additionally, none of these patients underwent cytotoxic conditioning (chemotherapy) prior to the infusion.

On the back of these results and carrying RMAT, PRIME, orphan drug, rare pediatric, fast track, and ATMP designations, Rocket anticipates filing simultaneous BLA/MAA submissions for RP-L102 in 1H24. The marketing application for Europe was accepted for review earlier this week.

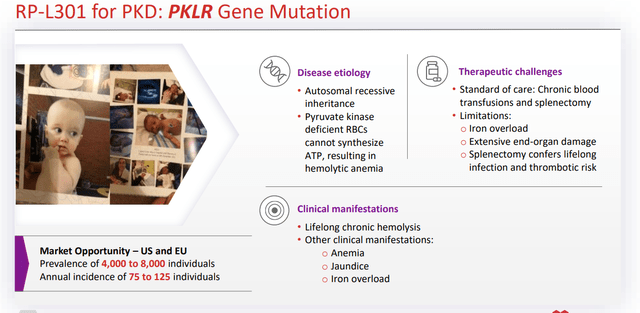

RP-L301. The company’s other LLV clinical asset is RP-L301, which is autologous HSCs transduced with LLV containing human PKLR transgene targeting pyruvate kinase deficiency (PKD). Red blood cells deficient in PKs are oddly (non-spherically) shaped, rendering them unable to synthesize ATP, resulting in anemia. The incidence of PKD is ultra-rare, with 75 to 125 new cases across the U.S. and EU. After its candidate demonstrating sustained hemoglobin improvements from severe baselines in two adult and two pediatric patients, Rocket anticipates entering RP-L301 into a pivotal Phase 2 trial, although no specific timeline has been forwarded. RP-L301 has received orphan designations from both the FDA and EMA, as well as fast track, RMAT, and rare pediatric disease tags from the FDA.

January 2024 Company Presentation

RP-A601. The company’s other clinical AAV therapy is RP-A601, which is being evaluated in a recently initiated six-patient Phase 1 study for the treatment of Plakophilin-2 arrhythmogenic cardiomyopathy (PKP2-ACM), an inherited heart disorder characterized by arrhythmias and sudden death with initial average presentation around age 35. It afflicts at least 50,000 in the U.S. and EU. RP-A601 has received orphan drug and fast track designations.

Balance Sheet & Analyst Commentary:

To pay for the advancement of its programs, Rocket has been a serial issuer of its shares, most recently raising net proceeds of over $188.9 million in a secondary offering of stock and pre-funded warrants at $16 per share in September 2023. It held cash and investments of $407.5 million at YE23, providing it an operating runway into 2026.

Street analysts remain unanimously bullish on Rocket, featuring 11 buy, one hold and three outperform ratings and a mean price objective of around $50 a share. On average, they project Rocket to generate FY25 revenue of just over $160 million.

Verdict:

When we last visited Rocket in May 2023, its stock was trading around $21 and we were optimistic on the company’s prospects then. The same holds true now, even up ~20% since we last paid it a visit. Obviously, any pre-clinical concern is risky given the challenges of development and approval process as there are many failures along the way to developing effective therapies that garner the FDA “thumbs up.”

Very small patient populations (i.e., less revenue) for most of its targeted indications notwithstanding, the company is producing disease reversal in the clinic, and with two platform-validating FDA approvals possible over the next 12 months, as well as excellent initial returns from potential blockbuster candidate RP-A501, Rocket is still appears undervalued and worthy of the analyst firms price targets on it. The bet is that Big Pharma will eventually agree and acquire Rocket. In summary, Rocket remains a “go” in front of potential catalysts.

Read the full article here