")

Summary

- Talen Energy has emerged from bankruptcy with less debt and an incredible asset base, which may be worth more than the entire company.

- Talen has massive tailwinds with the Inflation Reduction Act and its subsidies for nuclear.

- Talen has a clear catalyst for upside in the short term.

Talen Energy (OTC:TLNE) produces and sells electricity as its primary business. It has assets to do so in the Mid-Atlantic, Texas, and Montana. Additionally, the asset base to create electricity is diverse, spanning nuclear, natural gas, and coal. The company is also developing a zero-carbon data center campus focusing on crypto mining.

Emergence From Bankruptcy

Talen was taken private by a PE firm called Riverstone Holdings in 2016. It seems like Riverstone did what most PE firms did and leveraged up the balance sheet. As a result, they were forced to file Chapter 11. Now, they have emerged from bankruptcy with significantly less debt, and now in a different energy regime this energy is much needed. Much of it (Nuclear) is even looked at favorably in an ESG light.

Talen Assets

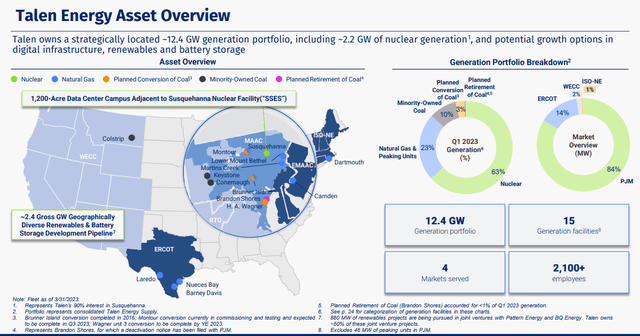

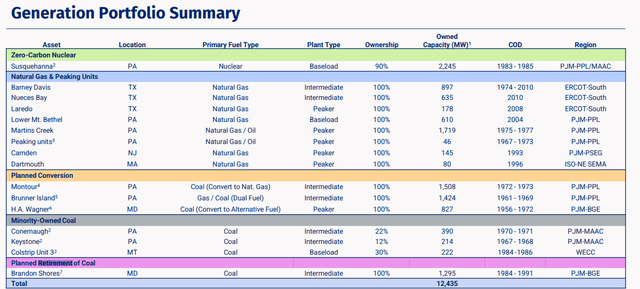

Talen Geographic Asset Base (Talen) Talen Portfolio (Talen)

Source: Talen June 2023 Update

Above are two pictures. (1) Shows the company’s asset overview, and (2) goes a step further into breaking down what each generation facility does, Talen’s percentage ownership, the market they serve, and the fuel type or how the asset generates power.

One important thing to note is that coal prices have hampered them due to its high price, but the company is forecasting that they will be retiring coal from their generation by the end of 2025. The best part about this is that they are forecasting that the majority of costs are already paid, with $257mm spent and only 22mm left to spend. This represents an additional upside of ~2.4 W!

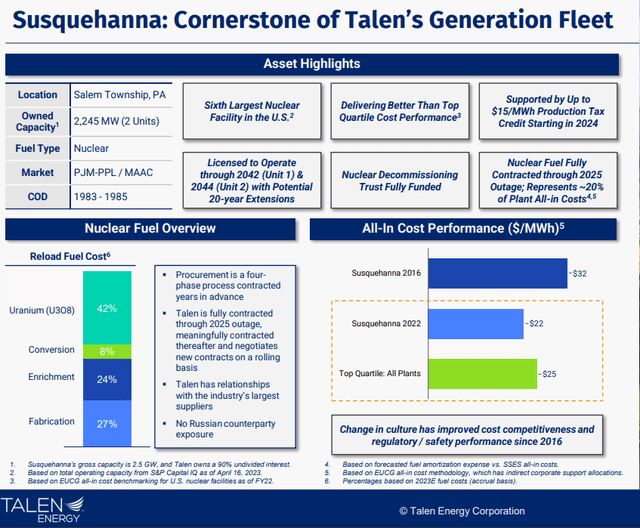

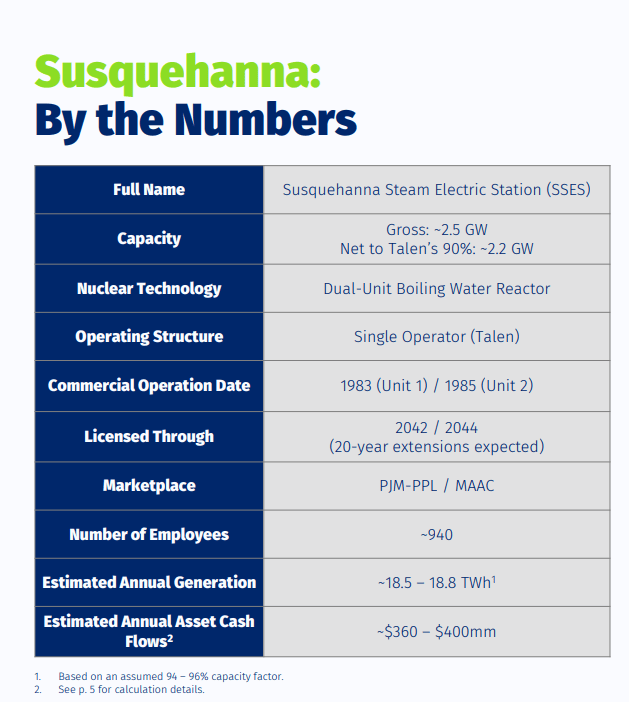

Susquenhanna:

Susquehanna Details (Talen) Susquehanna Details II (Talen)

These assets are obviously of significant value, but the Susquehanna plant is the true crown jewel and is even helping to further other projects. For context, Susquehanna is the 6th largest power plant in the US, and delivers better than top quartile cost performance. This is an incredible combination!

To make it even sweeter, producing nuclear energy is now supported by the production tax credit that Biden pushed through in the

Inflation Reduction Act (IRA). Legislation is now giving a credit of $15 per megawatt hour until prices rise above $25 thus creating a $40 floor price. This is extra appealing in the case of TLNE because it takes out a need for hedging, which was one of the reasons that caused them to go into bankruptcy. Additionally, the IRA enabled tax credit transferability, providing even more liquidity/optionality. The company is forecasting a potential benefit of $280 mm per year!

Assets With Upside

Next to the plant, the customer is building a zero-carbon data center. It is widely known from industry reports that the data center market is expanding and corresponding energy consumption. If you’re interested, you can read more about this in this McKinsey report. Well, Talen has already built a data center and is already working on partnering with hyperscalers with to get them in here. In their June update, they say “Customers are demonstrating interest, including substantial dialogue with key hyperscalers”.

Catalysts

So now I want to talk about the 3 biggest immediate upside to the company which are.

(1) Up listing to Nasdaq or NYSE.

(2) Cumulus Digital

(3) PPL litigation

So first the company has already gone from trading on the OTC pink sheets to the OTC QX. They’ve said they’re looking to up list in the near future. Their goal is to “Establish a liquid equity instrument with increased public transparency and focus on returning excess cash to shareholders”.

Second, if we go back to their data centers let’s talk about how they monetize these. Talen has a 75% ownership stake in Cumulus Data, a 1200 acre data center shell seeking a large customer like a hyper scaler. In the mean time the company (Cumulus) has created Nautilis, a cryptomine which is a bitcoin mining facility adjacent to the Susquehanna nuclear plant. However, the real upside is if they get a big name into this data center and create a long-term customer with power purchase agreements.

Lastly, we get to this PPL Litigation. So this history goes back to even before bankruptcy, but basically, Talen was spun out of PPL, the company alleges that the cash proceeds from an approximately $900 million sale of its hydroelectric assets to NorthWestern Corp. were improperly distributed to PPL. You can find more about that here. Anyway, if the Courts rule in favor of us this is a material amount of money coming back to Talen.

Valuation:

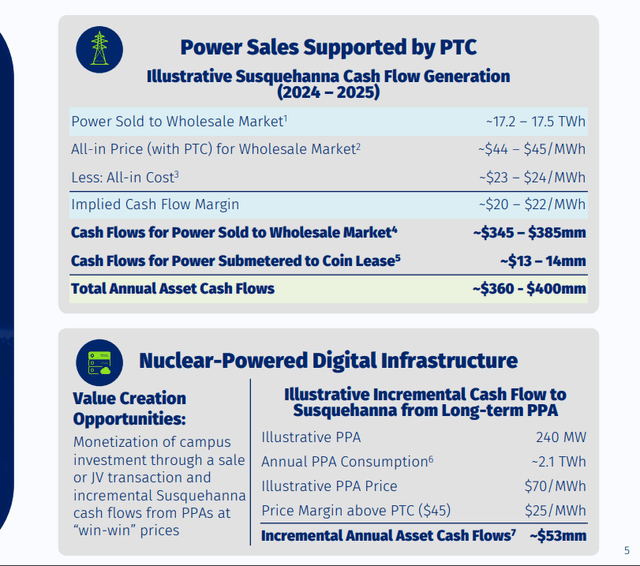

If you look at Talen’s asset base, we can see that it’s cheap. If we ignore everything besides Susquehanna we can see from the image below that it’s realistic that this can easily hit close to $500 mm in cash flow, especially if energy prices continue to climb into winter.

Nuclear Monetization (Talen) Talen Guidance (Talen )

From there, if we assign even no value to any of the other catalysts, we can get a best-in-class asset trading at ~10x adjusted free cash flow or a company trading at 10x EBITDA. What makes it even cheaper is that many of the projects that are not generating real cash yet have most of their capex completed! I believe this is one reason why the stock is so cheap and will appreciate once these assets start generating cash.

So we get to own a nuclear power plant, which seems like the only thing the market seems to value in this company, with all the other optionality for free. Additionally, the company just began a 300 million dollar buyback program, which is a clear signal to the market that management also thinks the stock is too cheap. Overall, this seems like a massive asymmetric bet to me as the company has all the right tailwinds, a lot of optionality, support from the government (IRA), and ample liquidity after emerging from bankruptcy.

Risks

I believe the biggest risks to the thesis are:

1. Regulatory – if there is any additional regulation around nuclear or something that makes them add more money to their nuclear decommissioning trust, it could materially hurt the business.

2. Liquidity – Given that shares trade OTC (for now) we could experience some volatility until they up list

Overall, I think the optionality the company has significantly outweighs the risk, and believe this company will outperform.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here