(TX)")

Since I gave Ternium S.A. (NYSE:TX) a buy rating in May, the stock is down about 2% largely due to falling steel prices and missing its Q3 EPS target. However, steel prices are bottoming, the company is growing market share in both Mexico and Brazil, and EPS is projected to rise by almost 40% in fiscal year 2024. Not to mention, upward revisions to consensus top-line estimates are encouraging. Despite posting total returns of over 35% in the past year, Ternium is trading at under 3x cash flow with an EV/EBITDA ratio of 2.54, and looks about 25% undervalued from an intrinsic perspective. Hence, I reiterate my buy rating.

Brazil Volumes Offset Headwinds

Ternium, Latin America’s leading flat steel producer, has 18 production facilities in Mexico, Brazil, Argentina, Colombia., the southern U.S. and Central America and posted $16.2bln in revenue in the past twelve months.

The company, which is actually headquartered in Luxembourg, sells hot and cold-rolled steel products to customers in a wide-range of businesses tops amongst which include those in the automotive, home appliances, construction, capital goods, and energy industries.

Ternium has a dominant position in Mexico’s steel market. In 2022, the 6.8 million tons of steel Ternium shipped to Mexico accounted for about 25% of the country’s consumption. And Ternium is on track to expand market share in 2023, although capacity constraints are limiting it from grabbing even more, the company said in its Q323 conference call. Ternium is also expanding market share in Brazil by boosting its stake in Usiminas in July from about 20% to 51.5%.

Q3 Results

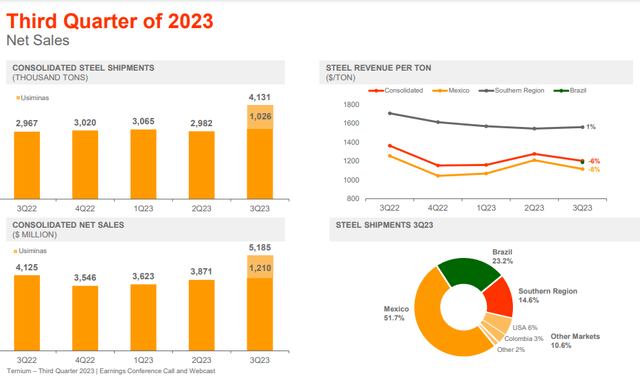

Sales grew $1.3 billion sequentially in Q3, with 90% of the growth coming from the consolidation of Usiminas volumes. About 23% of Ternium shipments were sold in Brazil with over half going to customers in Mexico. Revenue rose over 20% from the same quarter in 2022 while shipments are up 28%. However, as the slide below illustrates, steel prices continued to slide forcing revenue per ton lower, down about 6% from the previous quarter and 12% in the past year.

Ternium Q3 Sales/Shipments (Ternium Q323 Results Presentation)

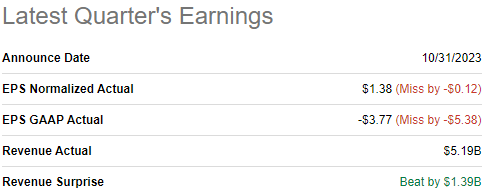

Ternium registered negative net income in Q3 due to a $1.5 billion non-cash loss resulting from increasing participation in Usiminas. However, even if we exclude this one-time cost, Ternium missed the non-GAAP EPS target for Q3, which led to a drop in the stock price, although it handily beat the sales target. Usiminas actually weighed on profit margins in Q3 as one of its blast furnaces was offline.

Ternium Q3 Earnings Results (Seeking Alpha)

Q4 & 2024 Outlook

As far as the fourth quarter prospects are concerned, the picture is mixed. Ternium projects Mexico volumes to increase in Q423 as a result of unraveling supply chain bottlenecks and despite typical seasonal weakening while Brazil shipments remain stable. Adjusted EBITDA is expected to decrease due to lower realized prices in Mexico and Brazil, although the company feels prices are beginning to recover.

The outlook appears brighter for 2024. Ternium says normalized margin performance will improve because they are seeing steel prices bottom out in the USMCA region and positive dynamics will impact the bottom line in Q124 as companies transition to restocking mode. Not to mention consensus estimates have TX EPS rising by almost 40% next year.

Ternium Consensus EPS Targets (Seeking Alpha)

Although the top line is only expected to grow 5%, I am encouraged by the upward revisions, which are likely to continue. The consensus sales estimate for fiscal year 2024 for example has gone up nearly 20% over the past 3 months. This is a key reason why the intrinsic valuation is higher than my previous analysis in May.

Ternium Consensus Revenue Revisions (Seeking Alpha)

TX Stock Valuation: Relative & Intrinsic

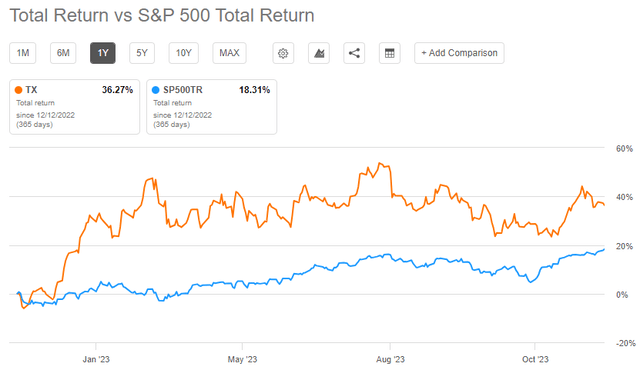

Ternium looks undervalued from both a relative and intrinsic perspective despite the stock rising by 25% in the past twelve months. Moreover, total returns are up over 35% in the same period. In addition, the company posts a strong dividend and has a solid balance sheet.

Ternium 1y Total Return (Seeking Alpha)

Key Multiples

Despite this solid performance, Ternium remains among the most undervalued steel stocks across the board, especially as measured by P/E, EV/EBITDA, Price/Book and Price/Cash Flow.

Price-to-Earnings

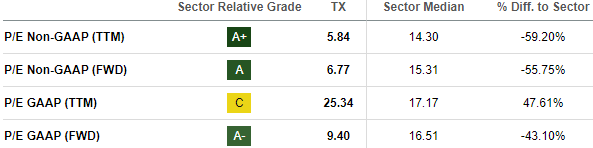

The non-GAAP P/E TTM of 5.84 is almost 60% below the sector median. The P/E GAAP ratio for the trailing twelve months is high due to the one-off cost from enhancing its position in Usiminas. It is also worth mentioning that the P/E for 2024 based on projected EPS and the current price is a mere 4.8.

Ternium P/E Grades (Seeking Alpha)

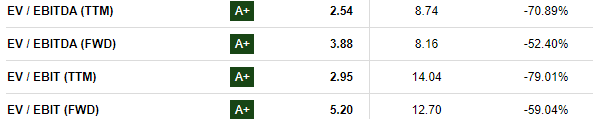

EV/EBITDA

Ternium’s EV/EBITDA ratio for the trailing twelve months is 70% lower than the sector median and EV/EBIT nearly 80 percent. The EV/EBITDA of 2.54 is lowest among 28 steel stocks ranked by Seeking Alpha (a list that in addition to pure play steelmakers includes coal, fab/machine shops, and distributors). The forward numbers are larger in light of expectations for EBITDA to fall in Q4 and yet still well below the market.

Ternium EV/EBITDA and EV/EBIT Grades (Seeking Alpha)

P/Book & P/Cash Flow

The company’s TTM and FWD price-to-book ratios are, respectively, 61% and 68% below the sector median. Ternium’s TTM AND FWD price/cash flow ratios are both more than 60% below the sector median.

Ternium P/Book and P/CF Grades (Seeking Alpha)

Dividend Strength

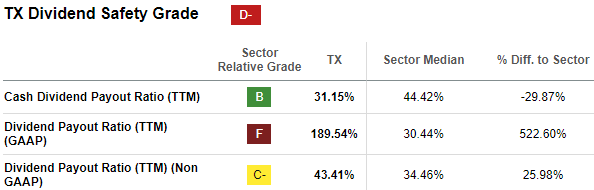

Ternium has received A’s in dividend strength and growth but D’s when it comes to safety and consistency

Ternium Dividend Grades (Seeking Alpha)

TX’s dividend yield of 7.44% is over 225% above the median of material sector competitors. The dividend has a 4-year average yield of 5% and 5-year CAGR of 20%. The consistency grade is driven by the fact the dividend has seen only one year in consecutive growth and only two years of consecutive payments.

Ternium Dividend Safety Grade (Seeking Alpha)

The dividend payout ratio based on GAAP principles is eye-popping at nearly 190% which is the reason it won an F grade, thereby dragging the overall safety mark to a D-. However, this is being driven by the aforementioned one-time Usiminas investment cost absorbed in Q3. Notice the normalized or non-GAAP dividend payout ratio is only 43%.

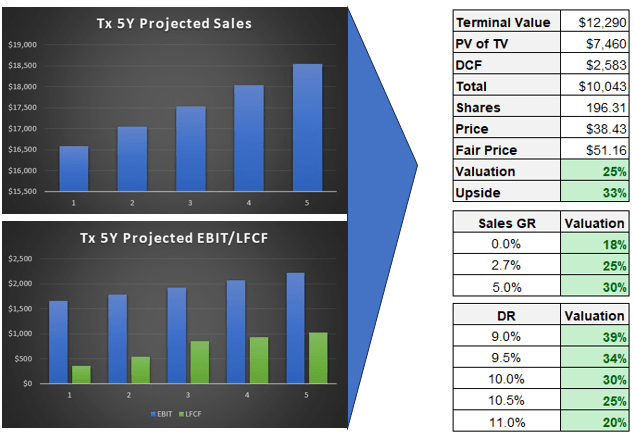

Intrinsic Valuation: Discounted Cash Flow

For the discounted cash flow analysis I utilized consensus estimates and historical averages for inputs like sales growth, EBIT, and capex/sales. Below is the five-year average of each key input:

- Sales Growth Rate: 3%

- EBIT Margin: 11%

- Capex/Sales: 10%

- Discount Rate: 10.5%

The stock looks undervalued by about 25% based on the five year DCF analysis, implying an upside of over 30%. The below slide also includes a sensitivity analysis based on sales growth from 0-5% and discount rate from 9-11%.

Ternium DCF Analysis (MH Analytics)

Rock Solid Balance Sheet

Ternium also showcases a solid balance sheet especially when compared to other major steelmakers. The company is $1.87bln net cash positive. Other critical metrics underscoring Ternium’s financial health include:

- Debt/Equity = 14% (this has gone down from about 30% five years ago)

- Book Value Per Share = 63.35

- Covered Ratio = 35

- Interest Expense / Sales = 0.61%

- Short-term assets exceed both short-term and long term liabilities

- Altman Z Score = 3.06

Risks

The investment in Ternium at this point is also a bet that Usiminas profit margins will rebound after having one of the blast furnaces offline. EBITDA & EBIT margins were squeezed in Q3 because of this, a failure to recover by Q124 and maintain EBIT margins at 10% or above would threaten the valuation.

It is also important to note that Brazil’s domestic steel market has been undermined by Chinese imports and to such an extent that steelmakers have petitioned the government to impose tariffs in a similar manner as Mexico. Although the company says it believes steel prices have bottomed, a continual deterioration of prices in Mexico will also undercut the boom in shipments.

The market is expecting earnings, sales and EBITDA to drop in Q4, and Ternium should be positioned to meet these lowered targets. However, a dive in steel prices or Usiminas’ failure to turn around could threaten prospects. A Q4 EPS miss will force the stock to drop in the near term.

Conclusion

Ternium’s stock price is up over 25% in the past year, shipments are on the rise, and the company is expanding market share in both Mexico and Brazil while steel prices are expected to rebound. EPS is expected to rise 40% in 2024 and revenue by about 5% and Ternium continues to maintain a rock solid balance sheet. Despite this the stock is trading at a mere 2.9x cash flow with an EV/EBITDA ratio lower than all steel stocks and 70% below the sector median. Hence, I rate it a buy.

Read the full article here