(NASDAQ:TSLA)")

Introduction

Tesla, Inc. (NASDAQ:TSLA) recently reported weaker-than-expected Q4 earnings, sending shares tumbling more than 12% the following day.

Lackluster growth, margin headwinds, and the lack of a clear outlook were the driving forces for the selloff.

Despite already being down 23% in 2024, it seems that the path of least resistance for the stock is down, given the company’s deteriorating fundamentals, weakening demand outlook, and rich valuation.

Buckle up, max pain ahead for Tesla.

Growth

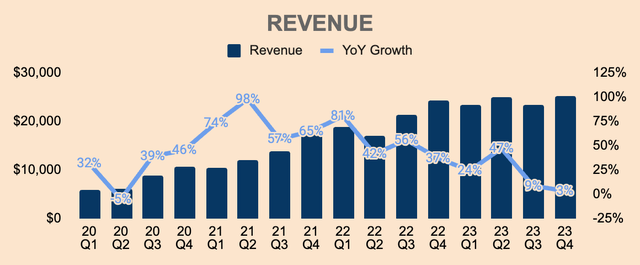

Tesla reported Q4 revenue of $25.2B, up only 3% YoY. This missed analyst estimates by $590M, or 2%, painting a weak demand picture for the leading electric vehicle (“EV”) manufacturer.

As you can see, growth has slowed down significantly over the last few quarters, down from 37% YoY and 9% QoQ. The trend certainly does not look good, with the company on track to have its first quarter of negative growth in over three years.

Author’s Analysis

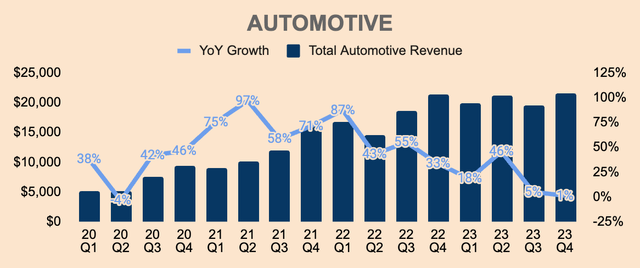

Breaking it down by segment, Tesla’s core Automotive segment, which accounted for 86% of Total Revenue, grew only 1% YoY to $21.6B. This was primarily due to lower average selling prices and lower full self-driving, or FSD, Revenue recognition.

Author’s Analysis

While Tesla achieved its 2023 production target of 1.8M vehicles, production and delivery numbers continued to slow down in Q4, even despite the price cuts:

- Q4 Total Production was 495K, up 13% YoY, down from Q3’s relatively low growth of 18%.

- Q4 Total Deliveries was 485K, up 20% YoY, again, down from Q3’s already-low growth of 27%.

Author’s Analysis

That said, Q4 was a record quarter for both production and deliveries, showing Tesla’s expansion plans in action.

We should see production numbers tick up higher in 2024 as the company has completed its factory upgrades in Q3, which increased its annual production rate to nearly 2M vehicles.

The question is: will deliveries have a record year as well? In other words, will the demand landscape support higher delivery numbers in 2024?

Only time will tell.

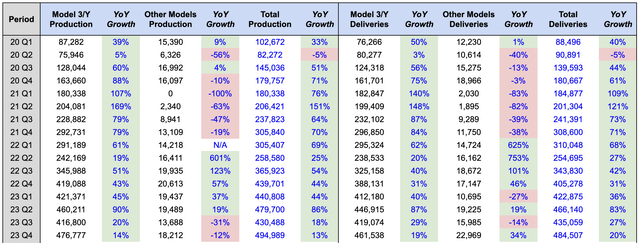

On the bright side, the Services and Other business produced a record Revenue of $2.2B, up 27% YoY, as Tesla’s fleet continues to expand. Despite robust YoY growth, notice how Services and Other Revenue has remained flat for two quarters in a row — perhaps, the segment is facing some challenges of its own.

Regardless, the segment should grow in 2024 as Tesla’s Supercharger partnerships with legacy automakers go live in 2024.

Author’s Analysis

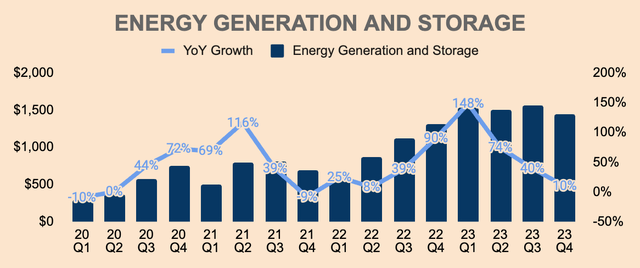

Moving on to Tesla Energy, the segment generated $1.4B of Revenue in Q4, which is up 10% YoY, driven by energy storage deployments. As you can see, growth for the Energy Generation and Storage business is fading as well.

Author’s Analysis

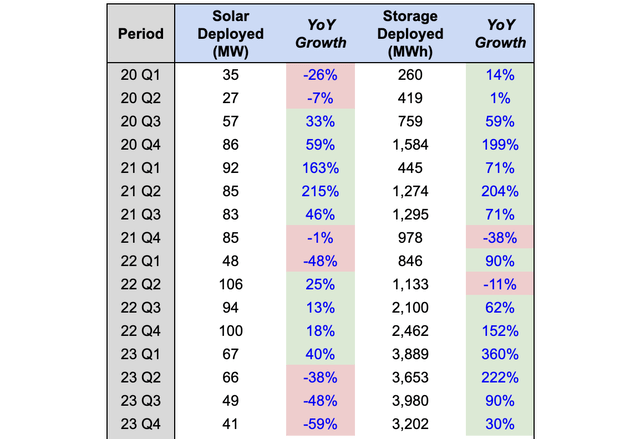

Its solar unit is the clear laggard, with only 41MW deployed in Q4, down 59% YoY. Ongoing high interest rates are putting immense pressure on the solar industry and Tesla is no exception.

Author’s Analysis

On the other hand, Tesla’s storage unit grew 30% YoY to 3.2GWh deployed. However, on a sequential basis, energy storage deployments dropped by nearly 0.8GWh.

That said, “deployments will continue to be volatile on a sequential basis” but management still expects “continued growth on a trailing twelve-month basis going forward.”

To sum up, all three businesses are facing major headwinds as growth turned stagnant. Each of Tesla’s businesses is interest rate sensitive and given the high interest rate environment the economy is facing right now, it’s no surprise that the company’s growth has come to a standstill.

Most concerning of all, its bread-and-butter Automotive segment seems to be heading for a decline in Q1, which may cause pandemonium among investors.

Fortunately, it seems that we’re at the peak of the interest rate cycle with multiple rate cuts on the horizon — when that happens, Tesla will enjoy strong demand tailwinds once again.

In the meantime, Tesla has to endure the short-term challenges. Growth is one. Profitability is another.

Profitability

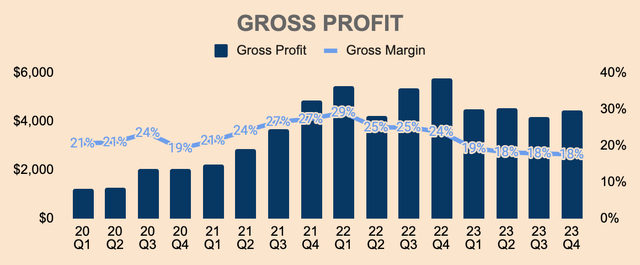

In Q4, Gross Profit declined 23% YoY to $4.4B, representing a Gross Margin of 18%, which declined 620bps YoY and 30bps QoQ. Gross Margin pressure was driven by the price cuts as well as the Cybertruck production ramp.

Whatever the reasons, Gross Margin decline never looks good as it may indicate fundamental weakness, perhaps a narrowing competitive moat or low pricing power — and that’s probably why investors are turning bearish on Tesla.

Author’s Analysis

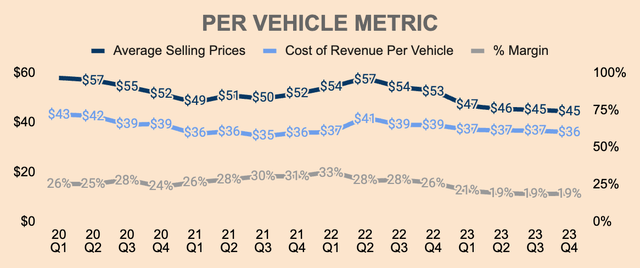

While Tesla was able to reduce Cost of Revenue per Vehicle, it wasn’t enough to offset the price cuts.

- As of Q4, Average Selling Prices declined about $8K YoY to $45K

- However, Cost of Revenue per Vehicle dropped only $3K YoY to $36K

- As a result, Automotive Gross Margin fell 700bps YoY to 19%.

Author’s Analysis

Yes, Tesla is sacrificing margins in the short term in an attempt to gain as much market as possible, so that the company can generate high-margin Revenue through ancillary services such as FSD.

But frustration is building up among investors. When will margins bottom? What’s the long-term margin profile of the business? What happens if Tesla raises prices again?

In addition, Tesla is currently working on the Next Generation Platform and a new EV model aimed at the mass market at a price tag of, get this… $25K.

What will happen to the company’s Gross Margin when the company launches this new vehicle in 2025?

My gut tells me that margins are going to head lower.

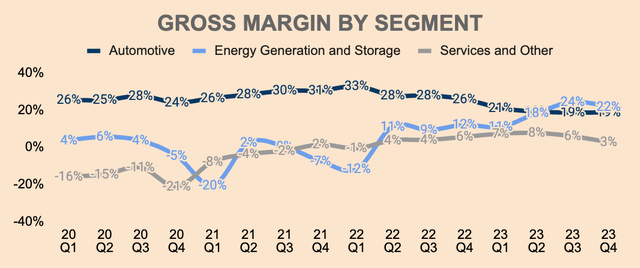

Some might argue that Tesla’s other two segments will compensate for the lower Automotive Gross Margins, but last time I checked, the other two businesses only produce a combined 14% of Total Revenue with not-so-impressive Gross Margins themselves.

- Energy Generation and Storage Gross Margin: 22%

- Services and Other Gross Margin: 3%.

Yes, they might improve in the future. But the crux of the matter is that their sizes are minuscule compared to the Automotive business, which means that margin expansion from these two segments may not be meaningful enough to cover the margin decline from the Automotive segment.

Author’s Analysis

That’s why Operating Margins continue to be under pressure, despite Gross Margin improvement for the two smaller segments.

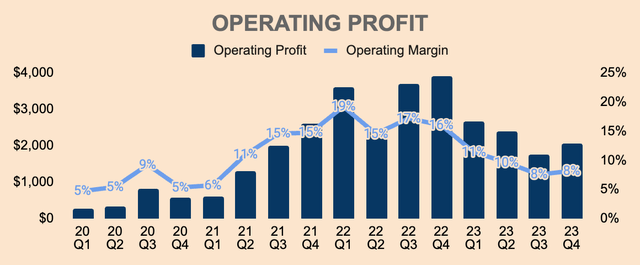

In Q4, Operating Profit was $2.1B, down 47% YoY. This represents an Operating Margin of 8% in Q4, which is now half from last year, mainly due to:

- Lower average selling prices

- Cost of Cybertruck production ramp

- Higher R&D expenses.

Author’s Analysis

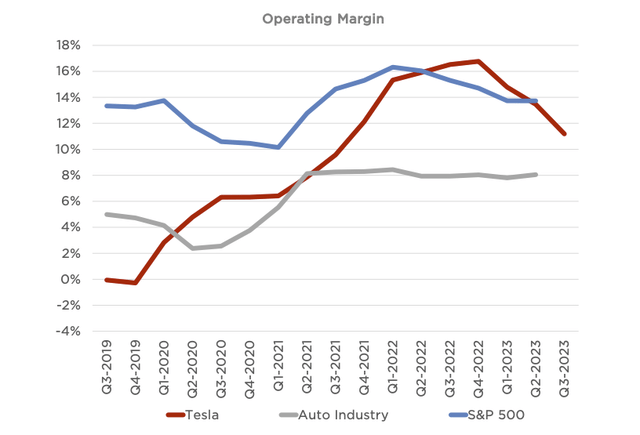

Oh… remember the chart below which compares Tesla’s superior Operating Margin to industry peers and the S&P500? Well… management decided to remove it.

In other words, Tesla’s profitability profile has turned so bad that comparing it with the auto industry and the S&P 500 (SP500) would weaken the investment case for Tesla — thus, it’s better to leave the chart out.

Tesla FY2023 Q3 Quarterly Update

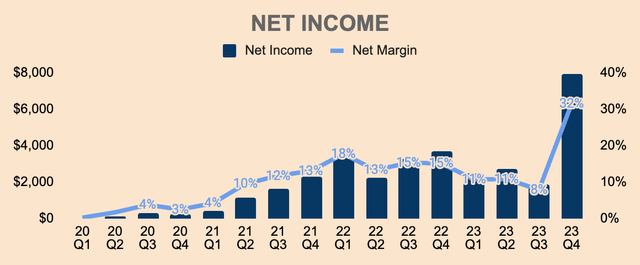

In terms of the bottom line, Q4 Net Income was $7.9B which included a one-time non-cash tax benefit of $5.9B, so without this benefit, Net Income would have been much lower.

Author’s Analysis

All in all, it’s difficult to interpret Tesla’s declining margin.

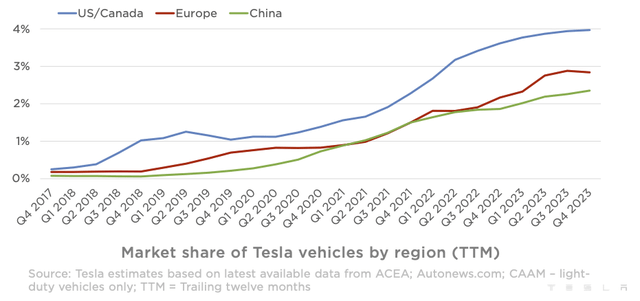

On one hand, optimists believe that Tesla is taking advantage of its cost advantages moats and intentionally lowering prices to maximize market share growth, which is reflected in the chart below.

Tesla FY2023 Q4 Quarterly Update

On the other hand, pessimists believe that Tesla’s falling margins are a reflection of weak demand, as a result of the macro situation and/or fierce competition.

So which side are you on?

As for me, I’m leaning more toward the pessimistic side — the data says it all:

- Growth slowed down significantly despite the price cuts

- Gross Margin declined meaningfully despite lower Cost of Revenue per Vehicle. In addition, there’s a “natural limit” to how much the company can cut costs.

That said, I need to see growth rates and Gross Margin bottoming before I turn more optimistic.

Health

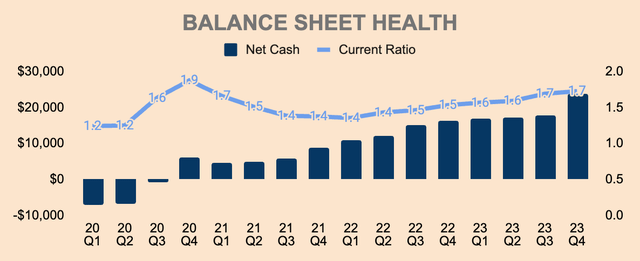

The good part about investing in Tesla over peers is that Tesla holds little leverage while peers have hundreds of billions of debt. Through whatever economic storm, Tesla is undoubtedly in the best financial position in the auto industry.

As of Q4, Tesla has $29.1B of Cash and Short-term Investments with only $5.2B of Total Debt, placing its Net Cash position at $23.9B. As you can see, Tesla’s balance sheet continues to strengthen with each passing quarter as Net Cash continues to grow.

Author’s Analysis

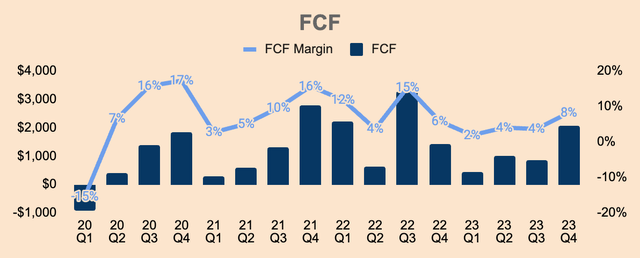

Net Cash grew $3.0B QoQ, driven by $2.1B of Free Cash Flow (“FCF”), representing an 8% FCF Margin. FCF remained strong despite high CapEx and R&D Expenses to fund future growth projects.

Author’s Analysis

Given its high Net Cash position, positive FCF profile, and plummeting share price, management might initiate a buyback program soon, especially if the share price keeps falling further, which could be a positive catalyst for the stock.

Outlook

Things already looked bad but it got even worse as management talked about the outlook, most notably:

In 2024, our vehicle volume growth rate may be notably lower than the growth rate achieved in 2023

(Tesla FY2023 Q4 Quarterly Update).

To recall, Tesla produced slightly over 1.8M vehicles in 2023, which is about a 35% increase from 2022.

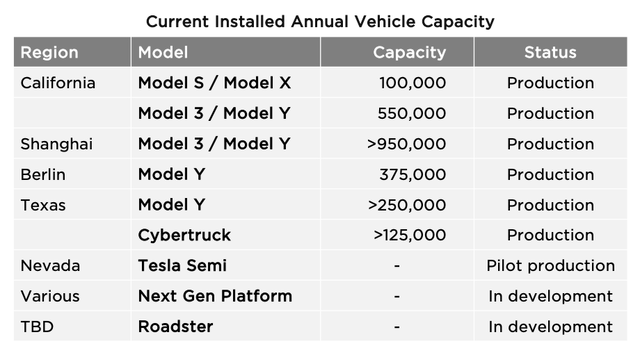

As it stands, Tesla has a total annual capacity of at least 2.35M vehicles. Assuming Tesla runs at full capacity and produces 2.35M vehicles in 2024, that is a 27% growth over 2023.

Tesla FY2023 Q4 Quarterly Update

I think this is unlikely.

I think 2.0M to 2.1M vehicles produced in 2024 is more accurate, which is about a 14% YoY growth — also “notably lower” than 2023’s growth of 35%

Assuming average selling prices remained stable at $45K, 2024 Automotive Revenue would be:

- 2.1M x $45K = $94.5B, which is up 15% YoY.

Mind you, Automotive Revenue grew only 1% in Q4 so a 15% growth in 2024 seems too generous.

With rate cuts expected in June, Automotive Revenue growth would likely remain depressed in the next two quarters. In fact, growth could turn negative in the first half of 2024.

It’s simple: high interest rates lead to low affordability, which results in lower Revenue.

In addition, Tesla is facing a couple more problems:

- Cybertruck ramp is going to take longer than anticipated “given its manufacturing complexities.” I have addressed the Cybertruck issue in detail in my previous article.

- With the expected launch of a new $25K model in 2025, many potential customers may cancel or defer their orders and wait for the release of the cheaper model, which may mean lower unit sales in 2024.

That said, while Tesla’s long-term growth story remains intact, the near-term outlook — at least, for the next two quarters — looks bleak, given high interest rates, slowing growth, and margin compression.

As such, I believe things are going to get worse before they get better.

Valuation

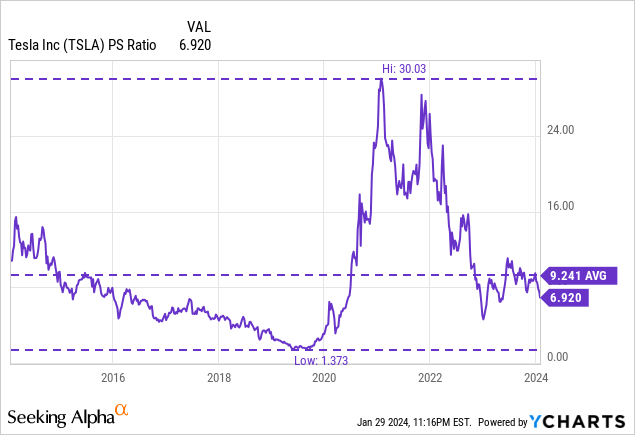

As it stands, Tesla trades at a Price to Sales ratio of 6.9x, which is a nice discount to its highs of 30x and its 10-year average of 9.2x, so on a historical basis, Tesla stock may look cheap.

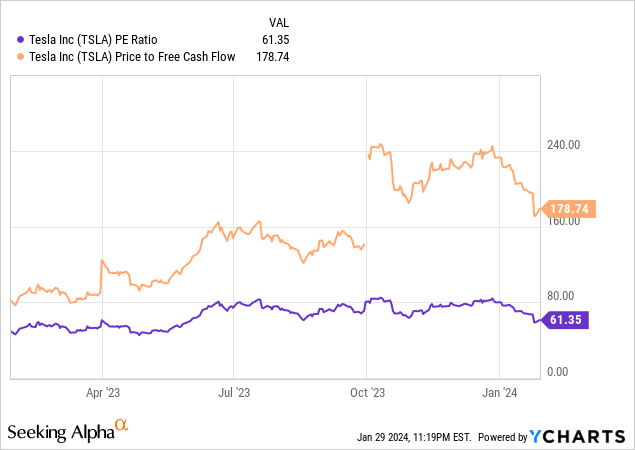

However, Tesla trades at a P/E and Price to FCF ratio of 61x and 179x, respectively.

I don’t know about you, but to me Tesla’s valuation looks very expensive considering weak growth, weak profitability, and weak outlook.

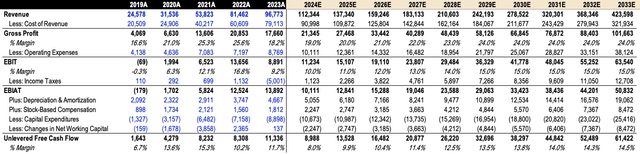

In light of management’s gloomy remarks, I’m lowering my price target as well. Here are my key assumptions:

- Revenue growth follows analyst estimates for the first three years and gradually falls to just 15% in 2027 and beyond.

- Gross Margin to expand to 24% by 2033. This one is a bit controversial given the margin trends as of recently, but I expect high-margin Revenue (like FSD) to eventually contribute to margin expansion.

Author’s Analysis

By 2033, Revenue is estimated to be about $424B, which is more than 4x from 2023. At the same time, I project a long-term FCF Margin of 14.5% for Tesla.

Author’s Analysis

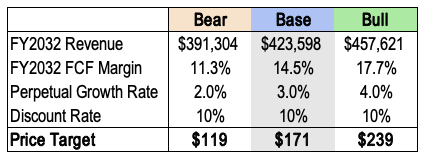

Based on a discount rate of 10% and a perpetual growth rate of 3%, I arrived at a fair value estimate of $171 for Tesla, which is lower than the average analyst price target of $219.

I have also included my bear and bull cases below. In all honesty, I’m leaning more towards the bearish side.

Author’s Analysis

I don’t care if you value Tesla as a car company or a software company or an AI robotics company — valuation matters, and right now, Tesla is still richly valued, despite being down 23% year to date.

And considering the company’s deteriorating fundamentals and weak outlook, I require a wider margin of safety to upgrade the stock to a buy.

Risks

- Higher for Longer: prolonged high interest rates will continue to put pressure on EV, solar, and energy storage demand. Rates need to go lower for Tesla to return to strong growth. That’s just the way it is.

- Competition: Competition is catching up, even Elon Musk admits it. We need to keep track of Automotive Gross Margin to evaluate Tesla’s cost advantages and pricing moat.

Well, our observation is generally that the Chinese car companies are the most competitive car companies in the world. So I think they will have significant success outside of China depending on what kind of tariffs or trade barriers are established. Frankly, I think if there are not trade barriers established, they will pretty much demolish most other car companies in the world. So they’re extremely good.

(CEO Elon Musk — Tesla FY2023 Q4 Earnings Call, emphasis added.)

Thesis

While I subscribe to Tesla, Inc.’s long-term growth story, there are a few things that are stopping me from buying the stock

For one, growth is slowing down significantly, so much so that we may see negative growth in Q1 and Q2.

Second, “in 2024, our vehicle volume growth rate may be notably lower than the growth rate achieved in 2023.”

Third, profitability is under pressure, which may indicate weak demand and pricing power.

And finally, valuation is still rich — I need a larger margin of safety.

For these reasons, I believe Q1 and/or Q2 might be a particularly turbulent quarter for Tesla. I believe things are probably going to get worse before they get better.

That said, max pain ahead for Tesla.

Read the full article here