Yesterday’s GDP report for the fourth quarter should have ended the debate about whether there is a recession on the horizon for the US economy, but there are still several pundits on Wall Street holding out. When one didn’t materialize in late 2022, they pushed out their forecasts to 2023, and when that didn’t look likely they indicated that 2024 would be the year of reckoning, using the same set of arguments that fell flat in 2022 and 2023. Granted, the yield curve remains inverted, the Leading Economic Index (LEI) has steadily deteriorated, and the M2 money supply is shrinking as consumers deplete excess savings. Yet this post-pandemic expansion is like no other, and failing to account for the anomalies that made it different is why those who relied on traditional leading indicators of economic strength were led astray. Ultimately, we will have another recession, as it is a part of the business cycle. Therefore, anyone who keeps forecasting one will eventually be right, but in the world of investing, timing is everything.

Finviz

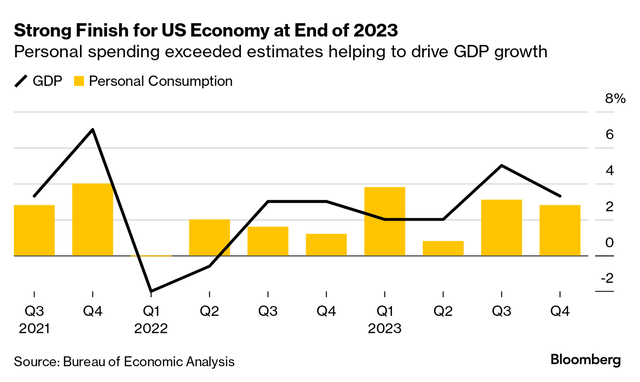

The economy grew at a 3.3% annualized pace in the fourth quarter, crushing the consensus estimate of 2%. While every major component was stronger than expected, consumer spending was the most important, contributing 1.9% to the total. The most relevant aspect of this report is that stronger-than-expected growth was accompanied by lower-than-expected inflation. The PCE price index fell from 2.8% in the third quarter to 1.7% in the fourth, while the core rate declined from 2.3% to 2%. The Fed has realized its mandate of stable prices, as well as a soft landing.

Bloomberg

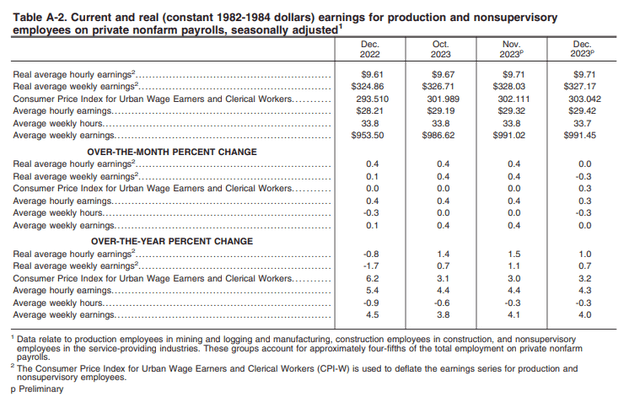

How has the economy avoided recession during one of the most aggressive rising interest-rate environments on record, combined with the highest inflation rates in 40 years? The soft landing narrative I proposed in the summer of 2022 was based on inflation falling as fast as it rose over the coming 18-month period. Meanwhile, excess savings would buffer consumers from the surge in prices for goods and services. Once excess savings were largely depleted, we would see a return to real wage growth, as the rate of inflation fell below that of the rate of increase in average hourly earnings. In other words, savings would hand the baton to wages at some point in 2023. As evidenced by the most recent Real Earnings report for December, that has happened. A year ago, the CPI was 6.2% and real (inflation-adjusted) average weekly earnings were shrinking by 1.7% year-over-year. Today, the CPI is 3.2% and real average weekly earnings are growing 0.7%.

BLS

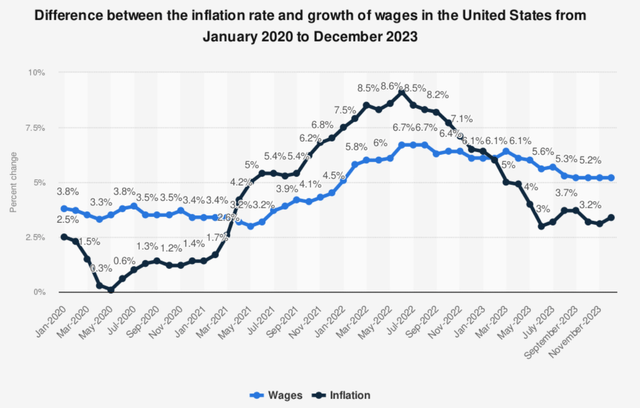

It looks like this handoff occurred during the first half of last year in the chart below. Regardless, this is why consumer spending continues to grow, staving off an economic contraction. Additionally, nominal wage growth rates are declining, but not at the same rate as inflation is falling. So there is more room for real wage growth to expand.

Statistica

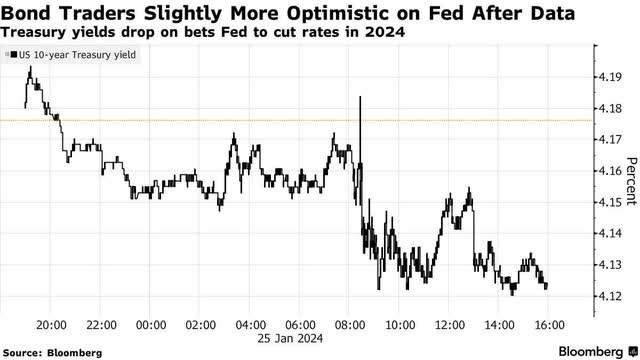

The Fed has achieved stable prices and pulled off the soft landing. If it isn’t self-evident now, it will be in retrospect by this summer. Since changes in monetary policy work with a lag of 6-12 months, Chairman Powell should start transitioning from today’s overly restrictive policy to one that is neutral in that it is neither stimulative nor restrictive. Fed officials have opined that this is likely somewhere between 3-3.5%. If this Fed wants to avoid the current policy rate slowing growth dangerously below trend later this year, it must start to lower it gradually at each meeting from March on. If not, then I think investors should be hyper-focused on the high-frequency economic data that best reflects the vital signs of the consumer. That will be my primary focus in 2024.

Bloomberg

Lots of services offer investment ideas, but few offer a comprehensive top-down investment strategy that helps you tactically shift your asset allocation between offense and defense. That is how The Portfolio Architect compliments other services that focus on the bottom-ups security analysis of REITs, CEFs, ETFs, dividend-paying stocks and other securities.

Read the full article here