")

For the past 12 months, the general investing public has been force fed an insane amount of excessive fear spread by newsletter writers, bloggers and the media alike, people with vested interests in seeing lower stock prices.

And unfortunately, a lot of people missed out on the rally off the late 2022 bottom, hoping that things return back to the doldrums of the 2021/22 bear market.

While I’m not naïve enough to think that the market won’t pull back, I think we need to take a look at the following things to see how we stand:

1.) Sentiment

2.) Technicals

3.) Valuation

1.) Sentiment

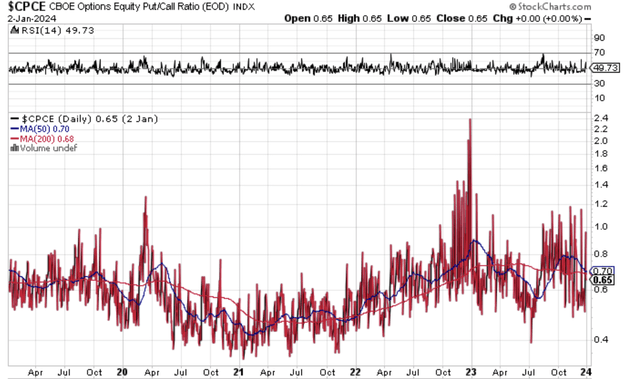

The CBOE Put/Call Ratio (CPCE) recently recorded a reading of 0.65. Typically, when the ratio is at 0.90 or greater it suggests that the average trader is bearish, which usually occurs around short term bottoms in the market.

When the CPCE is at 0.40 or lower it suggests that the average trader is bullish, which typically occurs near short term tops in the market. Here is a 5 year chart of the CBOE Put/Call Ratio:

CBOE Put/Call Ratio (CBOE Put/Call Ratio)

In looking at the chart above, the market is nowhere near the excessive optimism we saw in the late 2020 to late 2021 period, where the put / call ratio was consistently at 0.40.

We have been in an elevated CPCE of 0.60 to 1.0 for the better part of 6 months. I would say there is still more room for upside in the markets. When the reading consistently hits 0.40 I will begin exercising more caution, but until then I don’t think there’s any reason to think sentiment is too bullish.

Most traders/investors that I speak to are of this opinion: stocks look ok in the short term but not in the longer term. Most people are concerned about inflation, government debt, the coming election, and the Federal reserve. The proverbial wall of worry is sky high in my opinion.

2.) Technicals

Technicals are my guide post to determining when to buy and sell. I use these in combination with fundamentals to determine my entry and exit points in stocks and the market. I don’t think we need to concern ourselves with too many things, though. The motto of KISS (keep it simple stupid) applies here. The ones I look at the most are:

MACD

The MACD indicator a simple indicator of momentum. It takes trend-following indicators (i.e., moving averages) and translates them into an oscillator that is calculated by taking a shorter term moving average and subtracting a longer term moving average from it. It consists of 2 components:

This pivotal line on the MACD chart is computed by subtracting the 26-period Exponential Moving Average (EMA) from the 12-period EMA. Essentially, it represents the short-term momentum of the asset in question.

-

MACD Line: This pivotal line on the MACD chart is computed by subtracting the 26-period Exponential Moving Average (EMA)

-

from the 12-period EMA. Essentially, it represents the short-term momentum of the asset in question.

-

Signal Line: The signal line is a 9-period EMA of the MACD line. It is displayed on the same chart alongside the MACD line. The signal line’s role is to smoothen out the fluctuations of the MACD line and generate trading signals.

More than anything, it is an indication of momentum and trend following. I look for crossovers of the MACD relative to the signal line (often drawn in red on charts). If the MACD crosses below the signal line then it can be viewed as losing momentum and vice versa.

Full Stochastics

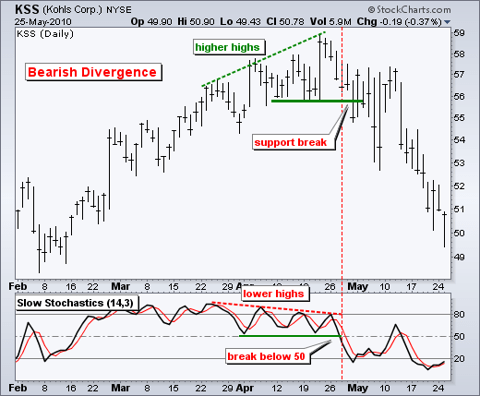

Developed by George C. Lane in the late 1950s, the Stochastic Oscillator is another momentum indicator. According to an interview with Lane, the Stochastic Oscillator “doesn’t follow price, it doesn’t follow volume or anything like that. It follows the speed or the momentum of price. As a rule, the momentum changes direction before price.” Stochastics are used to determine overbought/oversold conditions in addition to buy / sell triggers (i.e., when the %K line crosses over the %D line (often drawn in red on charts)). It can also be compared with price to determine bullish or bearish divergences with price. Here is an example of a bearish divergence where ultimately the price went lower:

Example of Full Stochastics (Example of Full Stochastics)

OBV

On Balance Volume (OBV) was developed by Joseph Granville in the 1960s and measures buying and selling pressure by adding up volume on up days and subtracting volume on down days from it. It focuses on the cumulative changes in trading volume over time.

I use it to help determine support for a stock / market. In shorter time frames, I find that there’s a lot of noise with this signal. You will see what I mean by this below.

With these 3 indicators in mind, let’s look at the overall market (NYSEARCA:SPY).

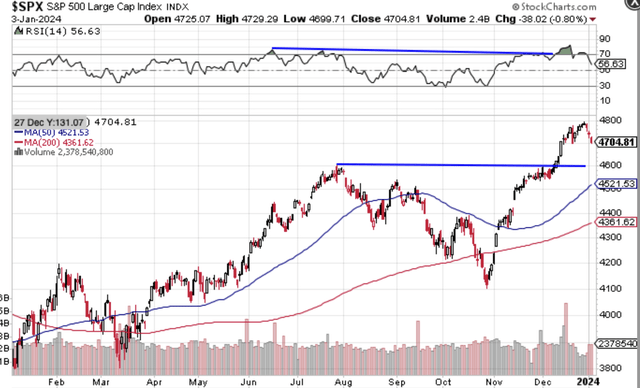

In late October, the market dropped 10% from August highs and FinTwit was in full on bear market mode, fearing the end of the US government and the talk was about runaway 10 year rates.

Then we rallied quickly to the August highs and we had what appeared to be a negative divergence in RSI. Traders called it just a short squeeze and they were sure the market was double topping.

Then the market exploded in early December past the August highs and the negative divergence was denied.

SPY Chart 2023 (SPY Chart 2023)

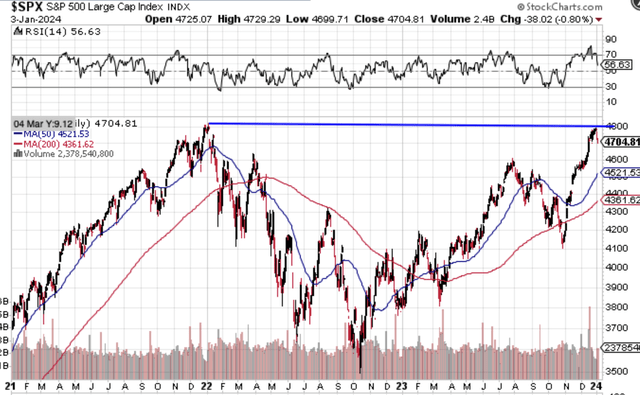

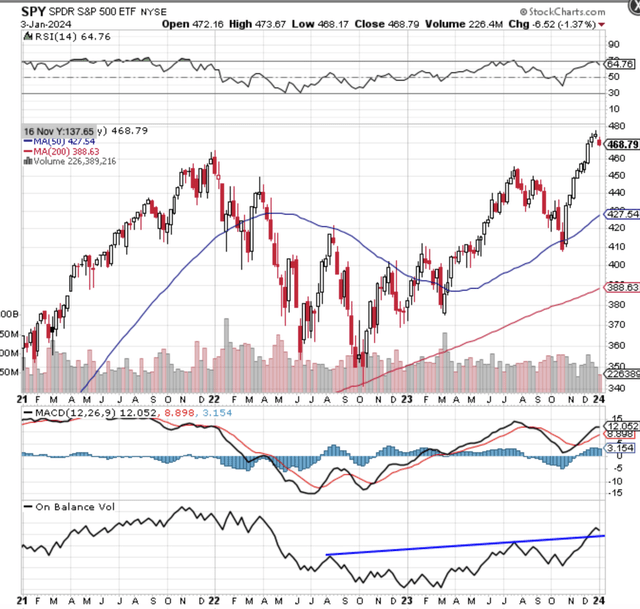

Now the concern, especially after this early January 2024 drop is that the market is double topping yet again, but this time the double top is with the 2021 highs. See the longer term chart below.

$SPX Chart 2021 to 2024 ($SPX Chart 2021 to 2024)

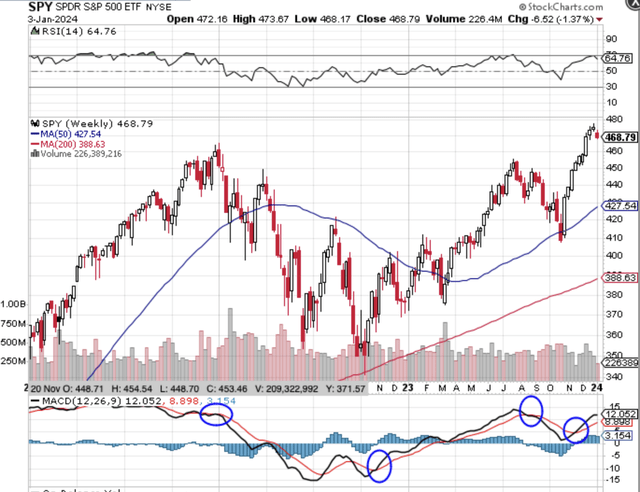

However, let’s take a look at things like MACD and OBV on a longer time frame (weekly time frame). Below is a weekly chart of the S&P 500 showing MACD crossovers. As you can see, the surge in November pushed the MACD for SPY into a buy. This mini-pullback here should likely be an opportunity to buy as the MACD is now in a bullish upswing.

MACD Crossovers – SPY (MACD Crossovers – SPY)

OBV, which again is an indicator of the volume coming into the market from the buy side, shows continued buying coming into the market. I prefer OBV on a longer time frame to avoid any false signals. See below the weekly chart:

SPY weekly Chart 2021 to 2024 (SPY weekly Chart 2021 to 2024)

3.) Valuation

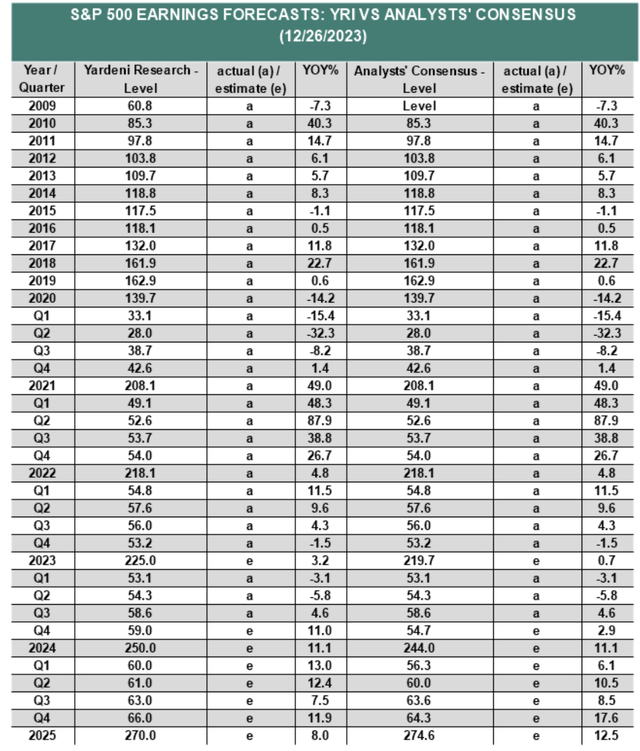

I follow research done by Ed Yardeni of Yardeni Research regarding the valuation of the overall market. According to Yardeni, earnings are expected to rise from $225 to $250 per share in 2024, leaving the market at around 18.8 times earnings.

That is around the same valuation that the market has averaged over the past 60 years during years in which rates are falling (the 10 year is now below where it was over the summer of 2023).

Here is Yardeni’s earnings chart.

Ed Yardeni S&P 500 Earnings (Ed Yardeni S&P 500 Earnings)

According to the above chart, stocks aren’t expensive but they aren’t cheap. Future returns likely will come from earnings growth and earnings growth looks strong for 2024.

What about the Transports?

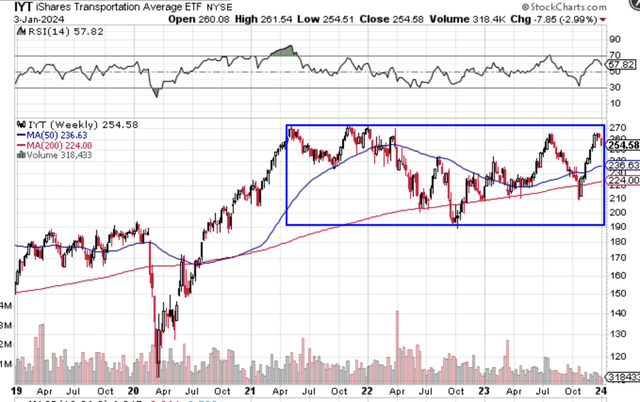

Much noise was made in 2022 about the breakdown in Transports and how they portend imminent danger for the overall economy. However, all they did was backtest the highs prior to Covid. Since then, they were first to retest the 2021 highs in early July 2023 and in the bigger picture, they have been in a 4 year consolidation pattern.

The move over the past 18 months in all likelihood has been one of consolidation and higher lows (i.e., recent lows in October higher than lows in October 2022). The weekly chart of IYT suggests that there could be an outsized move in transports coming soon as soon as it breaks above $270:

IYT Chart (IYT Chart)

If the markets are looking bullish, then what is the play?

If it is the case that the market should have more upside and technology has been the leader for a long time, perhaps it’s time to look to areas within laggards like consumer spending.

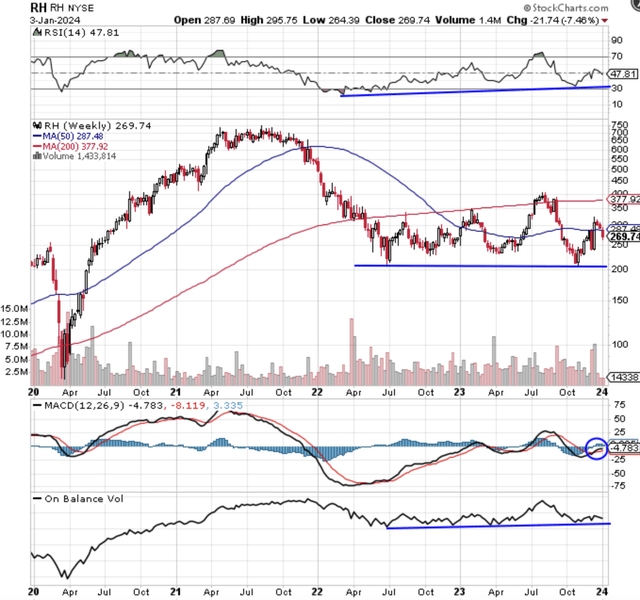

The best idea I have right now in this space is RH (RH), which I’m long. It is setting up a huge basing pattern, with a divergence in RSI while price made a double bottom in July 2022 and again in October 2023.

RH Chart (RH Chart)

MACD and OBV are giving a buy signal.

The best part: investors have completely written the company off. People on Twitter were openly mocking the CEO for doing a substantial stock buyback in 2023, at a time when sales in the luxury home market (their primary end market) were hitting the skids.

I wrote about RH here: “RH: Building a Luxury Empire”, which includes more about the fundamentals of the company and the CEO’s desire to climb the top of the luxury market.

With a strong stock market providing extra wealth for luxury home buyers and interest rates coming down, I expect a pretty strong rebound for this stock in 2024 and 2025. With a substantially reduced share count as a result of buybacks, there’s a scenario in which the company does $50-60/share in EPS in 2025, putting the stock at 4 to 5 times those earnings. It is my top buy.

Conclusion:

I recommend people to ignore the hype in the media around the Fed, inflation, government debt, and the upcoming US election. Inflation is coming down, interest rates have cooled, and sentiment is still pretty negative (as judged by CPCE).

Does it feel like everyone is all-in on stocks when every selloff results in elevated fear mongering? I think we can agree the vast majority of the public doesn’t believe this rally will continue, which is why it probably will.

I would look to things that haven’t rallied or that are still down a lot from their 2021 highs (like Shopify, which I’ve written about before).

Read the full article here