Anytime there is a major economic trend, there are multiple ways in which to capitalize. One of the most famous examples would be picks and shovels in the gold rush. Although not gold themselves, picks and shovels were a key piece of the supply chain in the pursuit of gold.

Similar logic has been applied to the artificial intelligence (“A.I.”) boom. In addition to companies that execute the A.I. directly, there has been a surge of investment in many of the products and services that fuel A.I. Many of these are already known to the market and have priced up thousands of percentage points. Others are less known, with one in particular not being priced in at all.

Allow me to begin with a bit of background, and then I will discuss the uncelebrated picks and shovels of A.I.

Known suppliers of A.I.

Much of the computing for A.I. is done in data centers and those data centers are fueled by GPUs, such as those produced by Nvidia (NVDA). Data centers and GPU makers are clearly known by the market to be the picks and shovels of A.I. as it can be seen in the tremendous market price movements.

SA

I am not a chips analyst, so I could not tell you if Nvidia stock is overpriced or underpriced. I only bring up the price action to show that the market is clearly aware of its association.

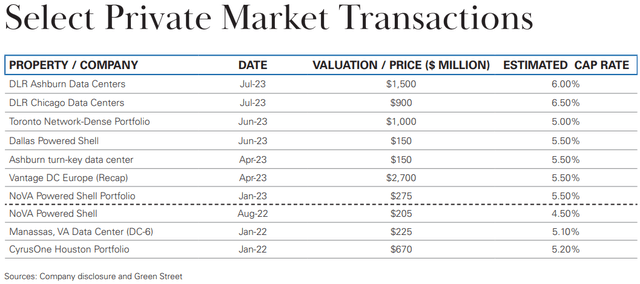

Data centers have not moved as explosively as Nvidia, but transactional data shows the market as well as private entities are valuing data centers as key components of A.I.

Newmark compiled a list of recent data center transactions, shown below.

Newmark

These are very low cap rates. In an environment where Treasuries are yielding almost 5%, sub 6% cap rates indicate buyers are pricing in a substantial amount of growth.

Unlike with chips, I am a data center real estate analyst, and in my opinion, data centers have become overvalued.

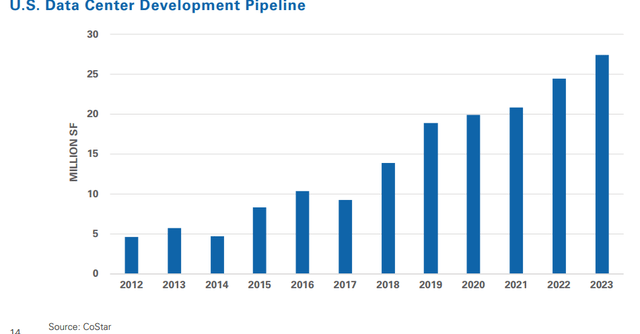

While demand is booming for data centers, there are almost no barriers to entry. Developers can simply build new data centers, which keeps rents at existing data centers from rising materially.

CoStar and Newmark

In other words, it is great to be a data center developer, but owning data centers, particularly those bought at low cap rates, is not a great place to be.

As these A.I. picks and shovels are known to the market and already priced in, I am not particularly interested in investing. There are, however, other key suppliers that have not priced up.

Energy producers: the unknown picks and shovels

The build out of data centers is having a massive impact on electricity demand. The increase in demand is multiplicative as it comes from 2 sources:

- More data centers being built

- Each data center consumes substantially more energy.

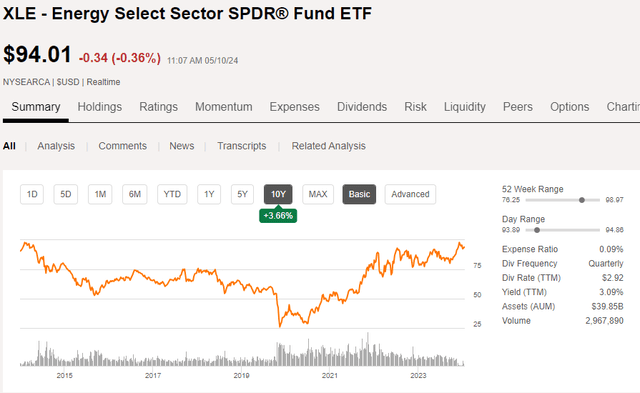

This energy demand should be a nice revenue driver for those positioned to produce it. The market has not priced this idea in at all. Energy production, whether green or gray, is priced about where it was 10 years ago.

Market pricing of conventional energy producers can be roughly estimated by the Energy sector ETF (XLE)

SA

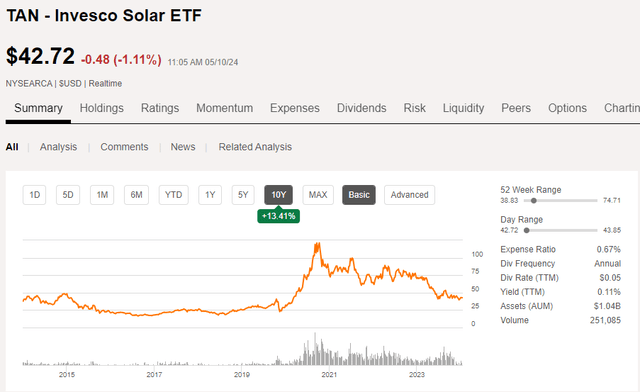

As a proxy for green energy, we can look at the Invesco Solar ETF (TAN)

SA

Both charts are within spitting distance of where they were 10 years ago, but you might notice they are mirror images.

During the pandemic, the concept of ESG investing took off. Investors sold grey energy to oblivion and bought solar into bubble territory. The bubble popped in 2021 and capital flowed back into conventional energy.

Based on valuation ratios that bubble has fully deflated with the earnings multiples of both grey and green energy looking quite reasonable and even a bit on the cheap side today.

The pricing would be appropriate for the now somewhat higher interest rate environment if demand drivers were normal. I posit that demand drivers, due to data center demand are substantially above normal for those positioned to deliver the right kind of energy in the right locations.

Why the market does not see it as a driver

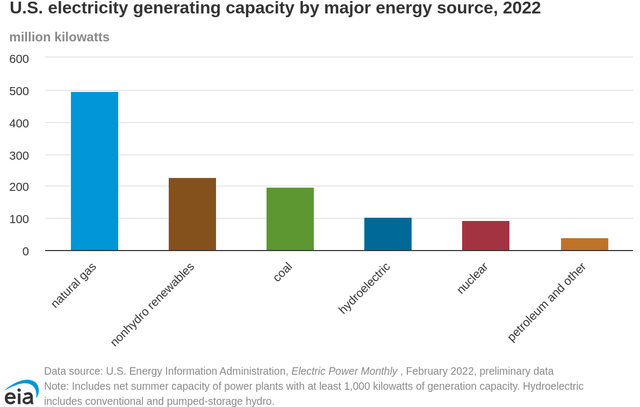

In 2022 data centers in the U.S. consumed about 17GW of power. The U.S. had electricity generating capacity of 1160 GW when aggregating the various types of energy.

EIA

So, data centers were about 1.5% of overall demand.

Electricity demand from other sources are roughly flat as efficiency gains such as LED bulbs are offsetting positive trends in electricity uses.

Recent data suggests data center power consumption will grow to 35 GW by 2030. That would take data centers to just over 3% of overall demand from the current 1.5%.

1.5 percentage points of incremental demand is a nice driver for energy producers overall, but that is nothing to write home about. Data centers being a reasonably small percentage of overall power demand is likely why energy producers are not seen by the market as picks and shovels of A.I.

However, data center development is very location-specific.

Location and power type matter

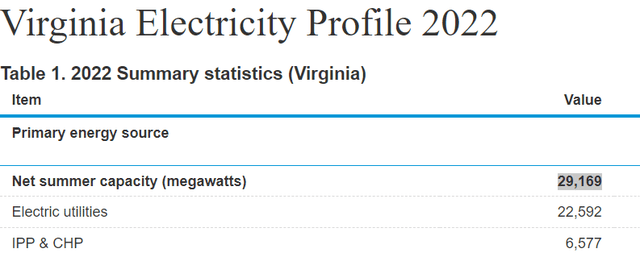

As of 4Q23, data centers in Northern Virginia consumed 3400MW of power. In contrast, the entire state of Virginia has capacity of 29,169MW.

EIA

So, while data centers are a small piece of the national pie, the data centers in NOVA alone account for 11.65% of the electricity capacity of the entire state.

That is just the starting point, Orders are coming in rapidly and in large chunks. According to Bob Blue (CEO of Dominion), some orders are for over a GW, as discussed in the 1Q24 conference call:

“historically, a single data center typically had a demand of 30 megawatts or greater. However, we’re now receiving individual requests for demand of 60 to 90 megawatts or greater and it hasn’t stopped there. We get regular requests to support larger data center campuses that include multiple buildings and require total capacity ranging from 300 megawatts to as many as several gigawatt”

A.I. data centers consume 2X to as much as 10X the power of former data centers.

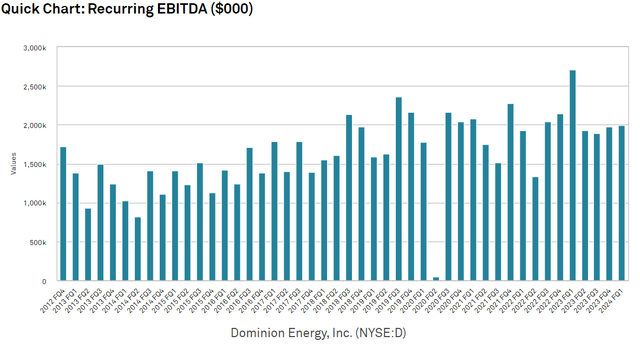

As Dominion is the primary provider of electricity in Virginia and NOVA specifically, they are capturing the lion’s share of substantial incremental demand. We wrote a more detailed thesis on Dominion here.

Other areas such as Dallas, Phoenix and Columbus are also experiencing rapid data center development. There could be opportunity in energy producers of those areas as well, although I have not yet vetted the specific stocks.

Beyond location, the type of energy can matter.

Data centers are often owned or leased by massive tech companies that almost universally have stated ESG goals. One of the most common objectives stated by these companies is a preset maximum level of emissions by a preset date. You have likely seen this as something similar to a pledge:

“carbon zero by 2033”

In the U.S., these pledges are largely voluntary, although enforced by the ESG committees set up at these companies. In Europe and other regions, such pledges are substantially less voluntary.

As such, the company not only needs to reduce its emissions, but has to do so in a way that can be proven.

When power is purchased from the grid, some percentage of it will be green and some percentage gray, but it cannot be tracked specifically which energy the data center bought.

To make it more easily provable, data centers have a tendency to engage in Power Purchase Agreements or PPAs in which they will buy power directly from a single source and in these agreements they can specify the type of power. For example, Equinix (EQIX) just announced a new PPA as discussed by their CEO, Charles Meyers, in the 1Q24 earnings call:

“In late April, we were pleased to announce our first renewable PPA in Singapore, an important part of our plan to continue to grow in this strategically critical market. This project will provide 75 megawatts of solar and is in line with Singapore’s Green Plan 2030, which seeks to have all business sectors supported by cleaner energy sources.”

Such transactions are fairly common. Thus, data center energy demand does not simply add a percentage point or two to grid energy demand. It comes in discrete packages which are won by specific power providers.

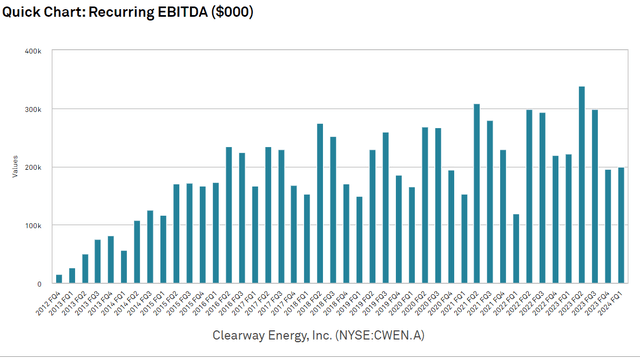

Certain energy producers are well versed in producing green energy and allocating it reliably and efficiently to specific PPAs. Clearway Energy (CWEN) does a substantial portion of their business through PPAs and is well positioned to capture incremental demand.

We discussed the opportunity in greater depth here.

There are likely many other stocks with similar opportunity. They would need to be researched on a case by case basis.

Big demand drivers not priced in

The magnitude of revenue upside for energy producers is not anywhere near as large as it is for the more well known A.I. stocks. As such, the reaction in stock price should not be as large.

I don’t think these stocks should rise 2000% like some of the A.I. darlings.

However, the investment opportunity is that they have not risen at all. CWEN.A is largely flat over 10 years.

SA

Dominion is actually down over 10 years.

SA

Weak pricing in these stocks has not been caused by weak fundamentals. EBITDA has been rising.

S&P Global Market Intelligence S&P Global Market Intelligence

The point is that these stocks have a substantial new demand driver but are priced at multiples lower than they were before that demand driver existed.

I think that is a great setup.

The broader opportunity

Incremental power demand is coming at a time when coal plants are being decommissioned. New power generation will need to accelerate to overcome the sum of incremental demand and lost former generation.

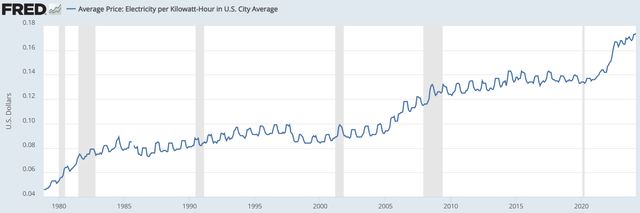

Electricity prices for consumers have been rising.

FRED

Ireland provides a nice example of where the U.S. could be headed. In Ireland, data centers are projected to consume 32% of power and consumers are rallying to try to block new data center development.

In the end, there is so much money behind data centers and A.I. that I don’t think efforts to block data centers will be successful. Instead, there will need to be more effort to fund electricity generation.

Economic incentives will naturally create this funding in the free market. I suspect it will come in many forms, ranging from reliable natural gas to green energy and even carefully deployed Small Modular Nuclear Reactors (SMRs).

In my opinion, investing in a broad range of power infrastructure will pay off eventually, especially given the reasonably cheap cashflow multiples at which many are trading.

Read the full article here