")

In October 2023, I issued an hold rating for Triumph Group over concerns that the company would dilute shareholders to service its debt maturing in 2025. The stock, however, has surged 86.5 percent compared to a 20.7% increase for the S&P 500. The surge was driven by a sale of a business unit that would allow Triumph Group to repay its maturing debt without diluting shareholders. In this report, I will be analyzing whether the reduced or eliminated risk of shareholder dilution and the current stock price provides a compelling entry point for investors.

Triumph Group Deals With Huge Debt Pile By Selling Business Unit

Triumph Group is an aerospace and defense company and the growth drivers there are quite clear. Despite some program challenges, commercial airplane program production rates will go up in the coming years while aftermarket sales remain strong as utilization continues to increase. In Defense, the geopolitical tension is driving demand for defense equipment and services as well and I expect this to be a multi-year trend as well.

Triumph Group

So, Triumph Group’s problem is not related to its end markets. The main issue was that its cash generation and cash pile would fall short significantly of its maturing debt. The company had $162.9 million in cash and cash equivalents and for 2024 a cash flow of $40 million to $55 million was projected by Triumph Group. At the midpoint that indicates $295.4 million when adding the cash pile and cash flow from inventory unwind expected in Q4 2024. For FY2025 (ending 31st of March 2025), $68 million in free cash was expected. With the Senior 2025 notes due by August 2025 and a backloaded cash profile. We would be looking at an approximated cash balance of $363.4 million which would not be sufficient to cover the debt.

My fear was that the company would dilute shareholders once again as it also did in June 2023 by exercising warrants to pay down debt. However, the company came up with a more constructive solution for shareholders by selling one of its business units. In December 2023, AAR announced that it would be acquiring Triumph Group’s Product Support business.

The divesture itself did not remove a big part of the debt as only $0.33 million out of a total of $1.63 billion in debt was removed. The proceeds from divesture, however, did significantly reduce debt. The entire balance of Senior notes due 2025 was paid off while 10% of the Senior secured first lien notes due 2028 was recalled. This brought the company’s debt down to $1,075 million implying a 34% reduction in debt while net debt improved from $1.46 billion to $0.78 billion driving a 46% improvement in net debt position.

What About Triumph Group’s Even Bigger $1.1 Billion Debt?

Selling off a business was probably the fastest way for Triumph Group to raise its liquidity. However, the $435 million of debt maturing by 2025 was only part of the debt. The bigger debt is due by March 2028 meaning by the end of FY2028. That amount is $1.08 billion.

The significant debt reduction is driving interest cost savings which Triumph Group can use to reduce its debt incrementally. I have modelled this using their previously assumed FCF/sales and applied this against the business correcting for the divested business.

|

2024 |

2025 |

2026 |

2027 |

2028 |

Total |

|

|

Estimated sales |

$ 1,120 |

$ 1,240 |

$ 1,360 |

$ 1,480 |

$ 1,600 |

$ 6,800 |

|

FCF/Sales |

-3% |

5% |

6% |

8% |

10% |

6% |

|

FCF |

$ -34.6 |

$ 55.8 |

$ 81.6 |

$ 118.4 |

$ 160.0 |

$ 381.2 |

|

Interest Savings |

$ – |

$ 60.8 |

$ 43.2 |

$ 59.4 |

$ 75.6 |

$ 239.0 |

|

Available from cash flow and interest savings to reduce debt |

$ 116.6 |

$ 124.8 |

$ 177.8 |

$ 235.6 |

$ 654.8 |

|

|

Debt reduction |

$ 180.0 |

$ 180.0 |

$ 180.0 |

$ 180.0 |

$ 720.0 |

|

|

Pro-forma cash |

$ 338.9 |

$ 275.5 |

$ 220.3 |

$ 218.1 |

$ 273.7 |

|

|

Senior Notes due 2028 outstanding |

$ 1,080.0 |

$ 900.0 |

$ 720.0 |

$ 540.0 |

$ 360.0 |

|

Our current projections show that the company can realize $239 million in interest savings and $415.8 in free cash flow from FY2025 giving the company $654.8 million to reduce its debt balance. Taking a $250 million cash balance on average, as a requirement, by 2028 the debt could be reduced to $360 million. This leads me to believe that Triumph Group can get quite far by using its free cash flow and interest savings to reduce debt but for at least a third of the remaining debt it would likely have to refinance. The good news is that with better financial performance expected and a more manageable debt level, refinancing can likely happen at much lower interest rates than the 9% that is currently being paid on the Senior notes due 2028.

Is Triumph Group Stock A Buy?

The Aerospace Forum

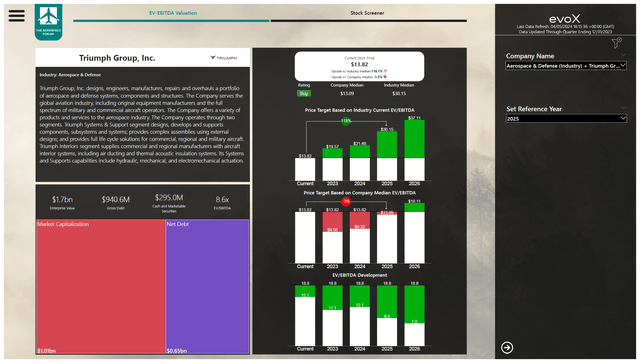

I believe that with the more manageable debt profile, Triumph Group stock is significantly more attractive. As a result, I am updating my price target to $21.60, which is right between the median EV/EBITDA for the company and that of the industry, as I believe that under the current circumstances a multiple expansion is justified. The rating is updated to buy, but we do note that we still have to see the company execute and build rates expectations for the Boeing 737 MAX are coming down. Triumph Group has around $0.3 million in components on each Boeing 737 MAX which would drive around $136.8 million in revenues.

Conclusion: Triumph Group Has To Execute Now

We saw Triumph Group making positives steps to reduce debt. What is left now for the company is show that it is can make the business generate cash again. There is some pressure driven by the Boeing 737 program production rate decreases, but I believe that Triumph Group is in much better shape now. Its net debt has reduced and with the combination of better free cash flow generation and interest savings it can address a significant part of the outstanding debt due by 2028. I still believe that the company will refinance some of the debt, but it will be able to do so at more attractive terms as its leverage has significantly improved.

Read the full article here