")

Today, we take a more in-depth look at equipment leasing concern United Rentals, Inc. (URI). The stock has risen some 70% since its late October as fears of recession have faded. However, it is difficult to see a scenario where the economy meaningfully accelerates in the quarters ahead. In addition, there was a noticeable uptick in insider selling in the first quarter, and some analyst firms are currently negative on the shares. Sign of a top? An analysis follows below.

Seeking Alpha

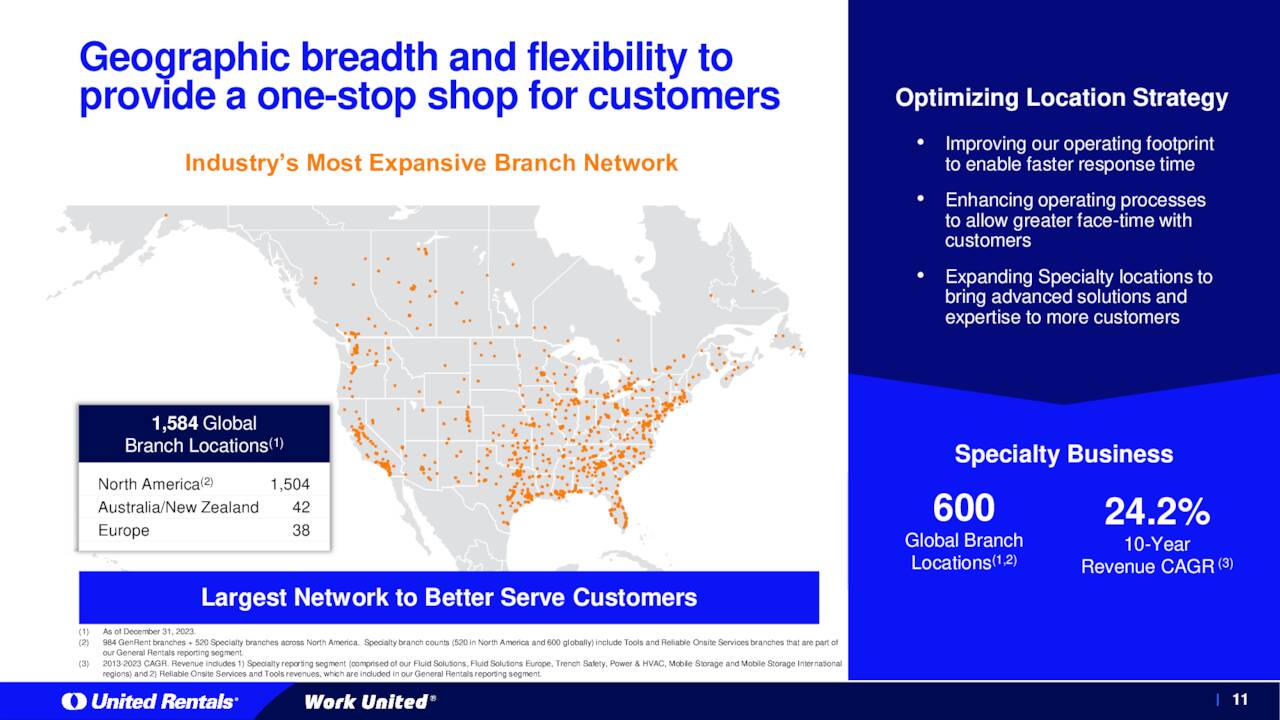

United Rentals’ business consists of renting industrial and construction equipment including items such as backhoes, skid-steer loaders, forklifts, and earth-moving equipment as well as specialty construction products which include trench safety equipment, aluminum hydraulic shoring systems, construction lasers, and line testing equipment. With the recent rally, the shares trade near $700 a share and sport an approximate market capitalization of $47 billion.

January 2024 Company Presentation

January Company Presentation

Factors Driving The Rally:

The rise in the stock has been curious given the high-interest rate environment that acts as a substantial headwind to new construction. However, in the fourth quarter, fears of recession receded and both third and fourth quarter GDP growth was impressive. The infrastructure spending contained within the massive Inflation Reduction Act or IRA legislation also has provided a tailwind. In addition, late last year investors were factoring in a continued decline in inflation that would allow the Federal Reserve to cut rates by a projected six times in 2024 according to futures. Something that has not materialized, even as we are now into spring.

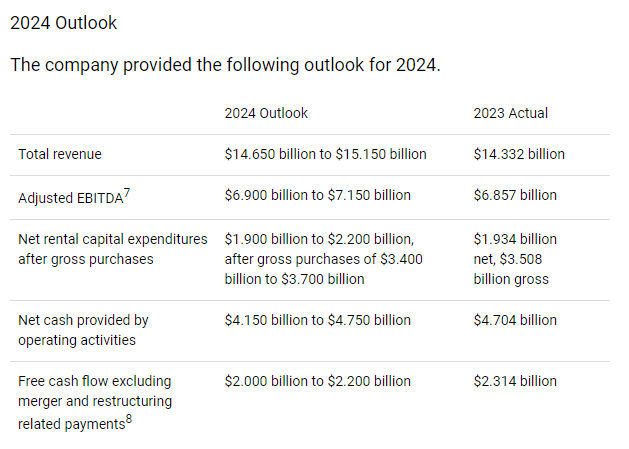

In addition, the company posted solid Q4 results on January 24th. The company delivered non-GAAP earnings of $11.26 a share, roughly a quarter per share above the analyst firm consensus. Revenues rose 13% on a year-over-year basis to $3.73 billion, $80 million above expectations. Management also provided initial FY2024 sales guidance that was above the consensus.

URI Press Release via Seeking Alpha

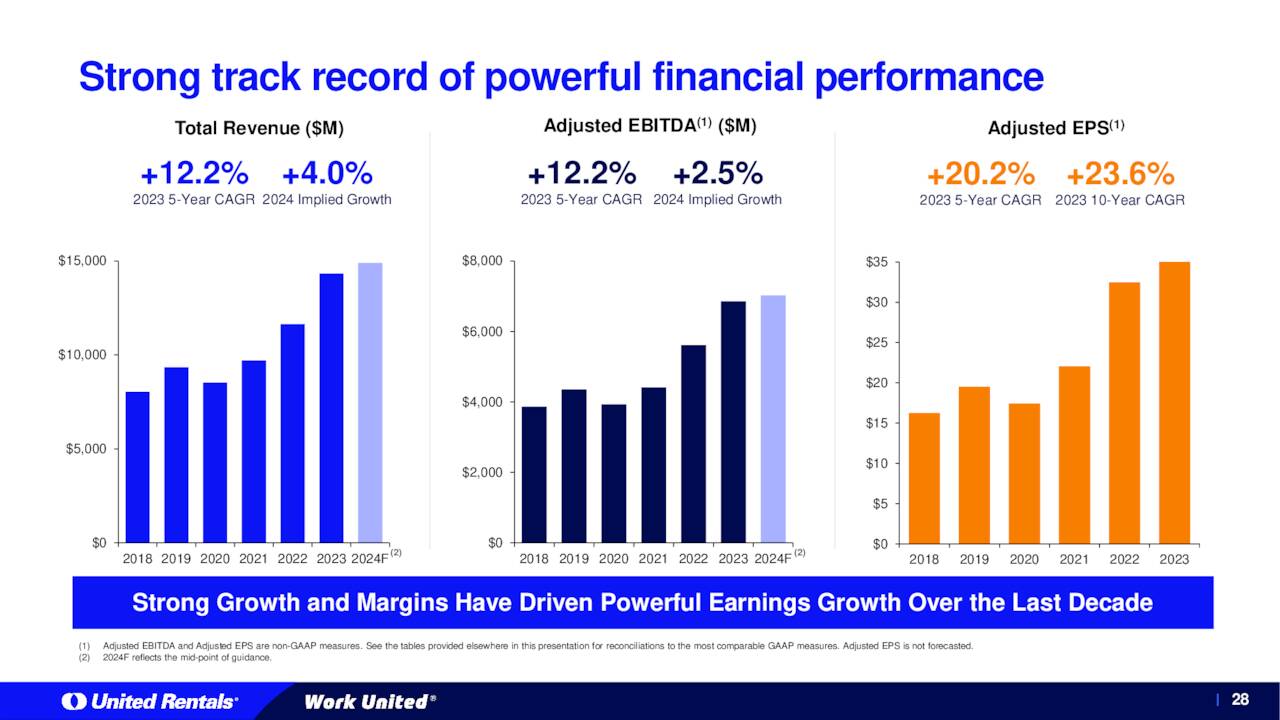

United Rentals has performed solidly over the past five years, as can be seen below. Early in March, the company announced a $1.1 billion acquisition. This is the latest in a series of ‘bolt-on’ strategic acquisitions the company has made in its history.

January 2024 Company Presentation

Potential Red Flags & Headwinds:

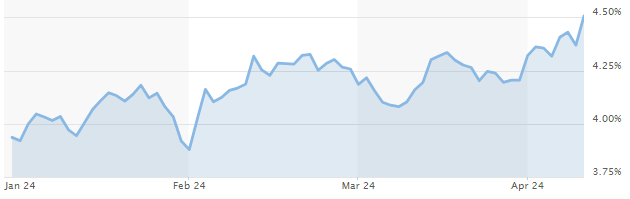

Wednesday morning’s CPI report was just another of myriad reminders that inflation is becoming much ‘stickier’ than hoped. The reading triggered another pop-up on the yield on the United States 10-Year Bond Yield (US10Y), which has not moved from just under 3.9% to 4.5% in a span of six weeks. Obviously, this is not a positive for new construction spending.

10-Year Treasury Yields (MarketWatch)

In addition, after a couple of big years, multifamily construction could have a significant downturn in 2024. In my recent article on the large building materials company Builders FirstSource, Inc. (BLDR), I noted that management projected that multifamily starts would be down 20% to 30% in the regions the company serves in 2024.

Several insiders sold just over $3 million worth of stock collectively from mid-February to mid-March. It was the first insider activity in the equity since a just over $300,000 disposal in mid-November. United Rentals made $40.74 a share (non-GAAP) on revenues of $14.33 billion in FY2023. The current analyst firm consensus has profits rising to $43.26 a share in FY2024 and $47.12 a share in FY2025. They project revenue growth of between four and five percent in each fiscal year.

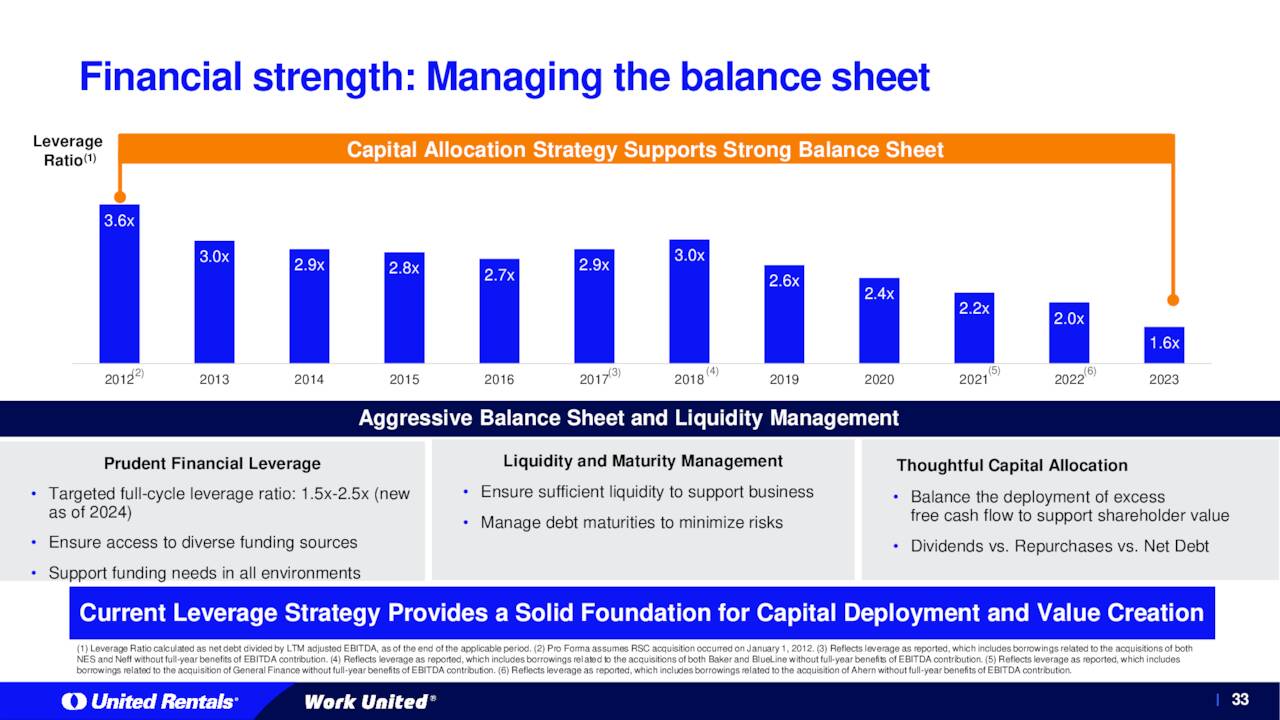

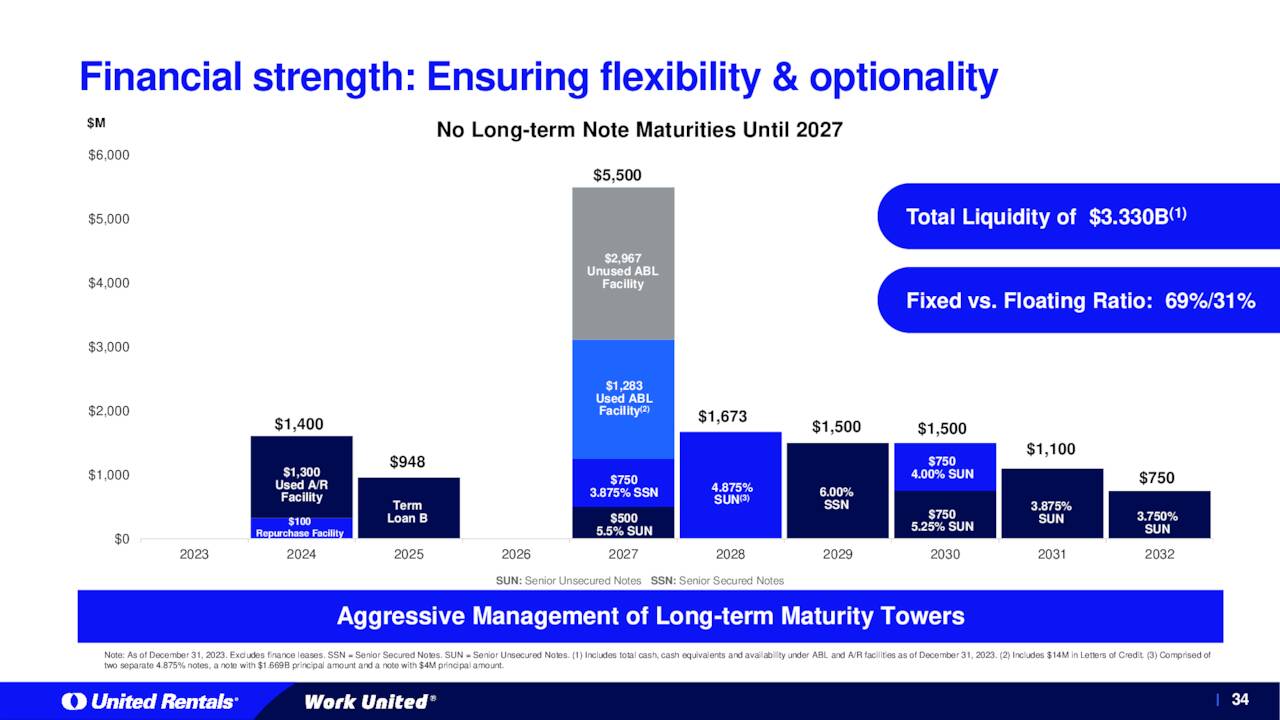

That leaves the shares trading at nearly 16 times forward FY2024E EPS and over three times forward sales. The stock pays a just under .9% annual dividend yield, and management bought back approximately $1 billion worth of stock in FY2023. In addition, management has done a good job of reducing leverage on its balance sheet recently, and its debt maturity schedule is in good shape as well.

January 2024 Company Presentation

January 2024 Company Presentation

Conclusion:

These seem dear valuations on a stock servicing a cyclical customer base. In addition, based on actual free cash flow in FY2023 and projected free cash flow in FY2024, the stock provides a free cash flow yield of just over 4.5% in an environment where short-term treasuries provide a “risk free” yield of 5.4%. Mainly because of valuation, so far in April Bernstein has reissued a Sell rating with $495 price target on URI while Robert W. Baird maintained an Underperform rating with $585 price target. Taking all of this into consideration, United Rentals, Inc. shareholders should act like insiders and take some chips off the table after the recent huge rally in the stock.

Read the full article here