")

A challenge only becomes an obstacle when you bow to it.”― Ray A. Davis.

Today, we take our first look at Ventyx Biosciences, Inc. (NASDAQ:VTYX), after this small developmental concern has suffered a recent setback in October and what looks like a complete debacle Tuesday morning. Both were in regard to the company’s pipeline development. With the steep decline in the stock Tuesday morning, the shares sell for less than the net cash on its balance sheet, and the company’ still has some “shots on goal within its pipeline. A “sum of the parts” value to take a chance on or a “falling knife” to avoid? An analysis follows below.

Company Overview:

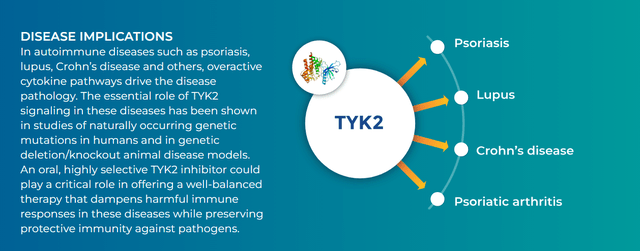

Ventyx Biosciences, Inc. is headquartered just outside of San Diego in Encinitas, CA. This clinical stage biopharma concern is focused on developing small molecule product candidates to address a range of inflammatory diseases. It’s lead drug candidate is called VTX958, a selective allosteric tyrosine kinase type 2 inhibitor that it is developing to treat several indications including psoriasis, psoriatic arthritis, and Crohn’s disease. The stock current trades around $3.50 and has an approximate market capitalization of $220 million based on pre-market trading Tuesday morning.

Company Website

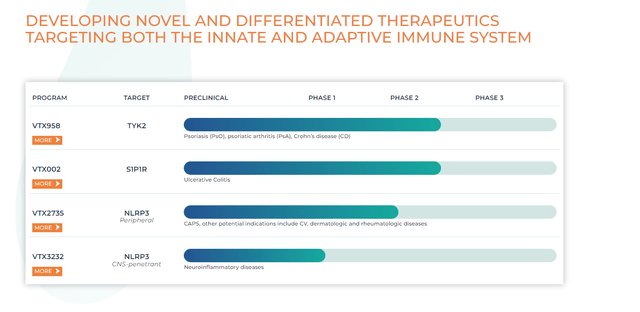

The company’s current pipeline includes four clinical-stage programs targeting TYK2, S1P1R and NLRP3. The company has two mid-stage developmental candidates. The first of these is dubbed VTX958. This candidate is an oral and selective allosteric inhibitor of tyrosine kinase 2 (TYK2). Management believed VTX958 had the potential to treat a broad range of immune-mediated diseases such as psoriasis, psoriatic arthritis, Crohn’s disease and lupus. It is now down to a single indication (more on that below) as of this morning.

Company Website

In the second quarter, the company completed the enrollment of patients in a Phase 2 “SERENITY” trial of VTX958 evaluating it as a potential treatment of plaque psoriasis. Results just came out Tuesday morning. To say the results were disappointing, is an understatement. While the data met both primary and secondary endpoints, the efficacy was not encouraging given the existing entrants in the plaque psoriasis market. The company has made the decision to discontinue development of VTX958 for both plaque psoriasis and active psoriatic arthritis.

The stock is off some 75% in early trading, and both Wells Fargo ($8 price target) and H.C. Wainwright have downgraded VTYX to Neutral. More analyst firms are likely to follow.

December Company Presentation

VTX958 now has one ongoing Phase 2 trial evaluating it for other indications. This is “HARMONY” for moderately to severely active Crohn’s disease. An interim efficacy analysis should be out from this study in the first quarter of next year. The Phase 2 “TRANQUILITY” study around VTX958 for active psoriatic arthritis will now be terminated.

Company Website

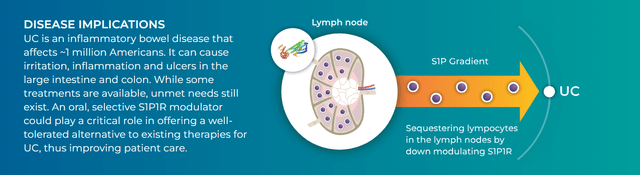

The company second mid-stage candidate is called VTX002. This is an oral, selective sphingosine 1 phosphate receptor 1 (S1P1R) modulator in development as a possible treatment for ulcerative colitis or UC. On October 9th, the company divulged top line results from a Phase 2 trial evaluating VTX002 to treat UC. While the data met their primary endpoint, results underwhelmed the investment community. The stock fell some 25% on the day of the announcement. The company will provide more updates from this study in 1Q2024.

A Phase 2 trial of VTX2735 in the treatment of familial cold autoinflammatory syndrome is currently ongoing. An update on this study should be out in the first quarter of 2024. This candidate is an oral, selective inhibitor of NLRP3 that is designed for the treatment of systemic inflammatory diseases. The company recently initiated a Phase 1 trial for VTX3232, but this asset is too early in its development to be germane to this analysis.

Analyst Commentary & Balance Sheet:

Since second quarter numbers were posted on August 9th, ten analyst firms including Oppenheimer, Goldman Sachs and Wells Fargo have reiterated Buy/Outperform ratings on the stock. Price targets proffered range from $43 to $77 a share. This obviously was before today’s negative pipeline news.

Approximately 18% of the outstanding float in the shares is currently held short. Several insiders have dumped approximately $3 million worth of shares collectively since the start of September. A beneficial owner has also disposed of nearly $3.6 million worth of equity over the past two months as well. The company ended the first half of 2023 with just over $330 million worth of cash and marketable securities on its balance sheet after posting a net loss of $53.3 million during the second quarter. Management stated that it is has funding in place for all planned activities into 2025 and that it had $300 million of cash as of the end of September with today’s trial news. The company has no long-term debt.

Verdict:

December Company Presentation

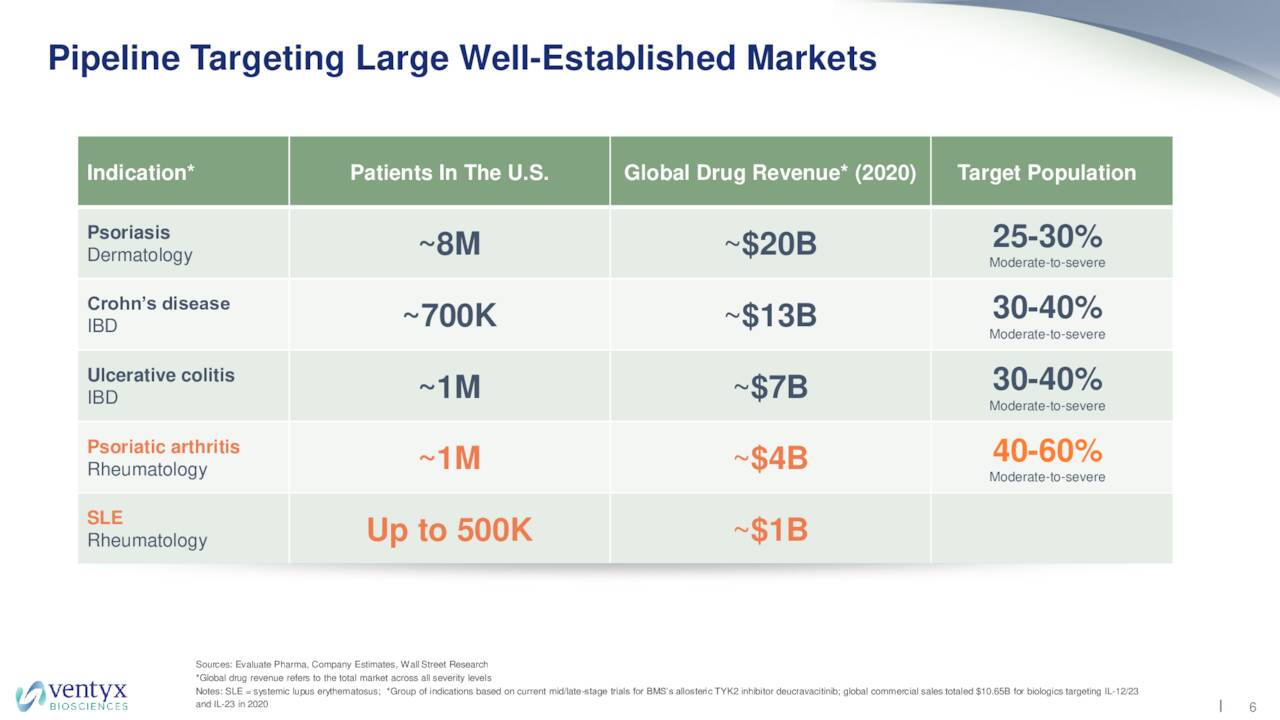

The company’s pipeline is targeting some large potential markets, but ones that already have established competitors. With today’s decline, the stock is valued for a bit less than the net cash on Ventyx’s balance sheet. However, the company will continue to have a significant quarterly cash burn rate, even as it should go down with the discontinuation of two key studies as of this morning.

The firm still has a few shots on goal and some key trial readouts out in 2024. However, with two strikes against the pipeline over the past month, I doubt many investors will stick around to see strike three. Therefore, I have no investment recommendation on Ventyx Biosciences, Inc., and I would leave the shares alone until the company is able to produce much more positive trial results.

Nothing is better for self-esteem than survival.”― Martha Gellhorn.

Read the full article here