Whenever most people hear the term commercial real estate they run.

Who wouldn’t be afraid of rising rates, debt maturities, loan defaults, and the office sector meltdown?

Blame it all on Covid-19 if you want, but there is no question that this market has created a perfect storm for REIT shorts sellers.

As most know, shorting stocks can be dangerous, especially for novice investors.

Heck, even experienced investors get burned.

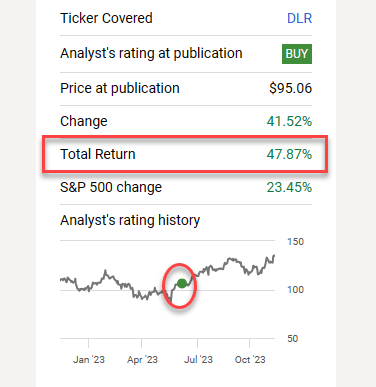

Just over a year ago (October 2022) I wrote an article explaining that “Jim Chanos, founder of Chanos & Company came out with his data center short and his premise was that hyperscalers are essentially the enemy.”

He said that “eventually hyperscalers will digest Digital Realty’s (DLR) core business and bring it into the cloud and the necessity of the kind of hybrid private, public cloud, public provider won’t be there anymore.”

I’ve debunked that thesis more than once here on Seeking Alpha and as shown below, Chans was wrong.

Seeking Alpha

(I’m overweight DLR)

It doesn’t surprise me to see Chanos shutting down his hedge fund as he explained, “The marketplace for what I do has changed”. Chanos & Co.’s funds are down 4% year to date, which validates the point I made that “shorting can be dangerous”.

Remember, the most you can earn on a short is 100% and that’s only if the stock goes to zero. But the potential losses are limitless if the stock goes up.

For REITs (and other dividend-paying stocks) a short seller is also on the hook for any dividends the company pays while the short position is open – which makes the risk even more pronounced with REITs since they tend to pay high dividends.

The same goes for interest charged for borrowing shares.

In addition, REITs’ real estate portfolios are almost never worthless, which once again makes it more expensive to maintain a short with limited rewards.

So, with that in mind, I thought it would be interesting and exciting to put together an update on several of the most shorted REITs.

SL Green Realty (SLG) – Short Interest: 28%

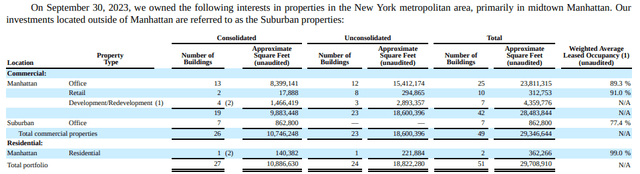

SL Green is a real estate investment trust (“REIT”) and Manhattan’s largest owner of office buildings with a portfolio of 59 properties covering 32.5 million square feet, including ownership interest in 28.8 million square feet of properties in Manhattan and 2.8 million square feet of property securing SLG’s debt and preferred equity investments.

SL Green specializes in the development, acquisition, repositioning, and management of Manhattan commercial properties, primarily office properties, but they also invest in other property types such as select residential and retail assets.

In addition to receiving rental income on the properties they own, SLG also generates investment income on debt and preferred equity investments.

The chart below shows SLG’s owned properties in the New York metro area and lists properties outside of Manhattan as their suburban properties. It also breaks down and categorizes property types including both commercial properties and residential.

Their commercial properties consist of 25 office properties located in Manhattan covering 23.8 million square feet with a weighted average leased occupancy of 89.3% and 7 office properties outside of Manhattan that cover 862,800 square feet and have a weighted average leased occupancy rate of 77.4%.

SLG has an ownership interest in 10 Manhattan retail assets covering 312,753 square feet with a weighted average leased occupancy of 91.0% and 7 Manhattan development projects totaling 4.4 million square feet.

For their residential category, they have 2 residential properties in Manhattan covering 362,266 square feet with a weighted average leased occupancy rate of 99.0%.

SLG – IR

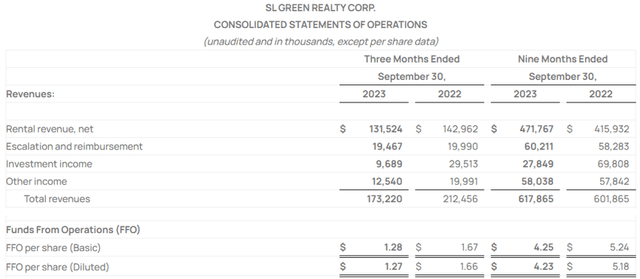

In October, SLG released its third-quarter operating results and reported total revenues during the quarter of $173.2 million, compared to total revenues of $212.5 million in the third quarter of 2022.

The company reported funds from operations (“FFO”) at $87.7 million, or $1.27 per share, compared to FFO of $114.2 million, or $1.66 per share for the same period in 2022. On a per-share basis, the year-over-year change in FFO represents a decrease of approximately 23%.

Additionally, SLG signed 50 office leases in Manhattan totaling 355,831 square feet during the third quarter and signed 134 office leases in Manhattan totaling 1.3 million square feet through the first 9 months of 2023.

When excluding leases for One Vanderbilt, the leases signed during the third quarter have an average lease term of 6.3 years and tenant concessions of almost 6 months of free rent.

SLG – IR

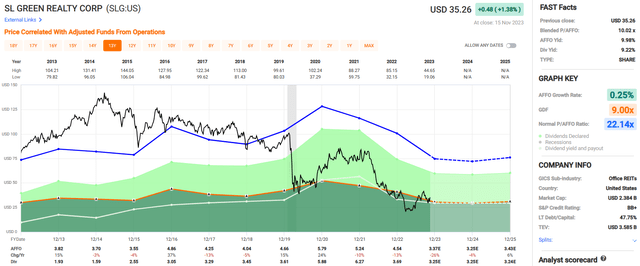

Since 2013 SL Green has had a blended average adjusted FFO (“AFFO”) growth rate of 0.25%. AFFO fell by -13% in 2022 and analysts expect AFFO to fall by -26% in 2023.

In 2024 analysts expect another decline of 4%, but the following year analysts expect SLG to return to growth with AFFO per share projected to increase by 6%.

SLG pays monthly dividends and offers a 9.22% dividend yield with a 2022 year-end AFFO payout ratio of 81.23%. As previously mentioned, analysts expect AFFO to fall by -26% in 2023, from $4.54 to $3.37 per share.

If analysts’ estimates are correct, it would put the 2023 expected AFFO payout ratio at approximately 96%, and the 2024 expected AFFO payout ratio at 100%.

Currently, SLG is trading at a massive discount with a current P/AFFO of 10.02x, compared to their 10-year average AFFO multiple of 22.14x.

We rate SL Green Realty a Spec Buy.

FAST Graphs

Medical Properties (MPW) – Short Interest: 23%

Medical Properties Trust is a healthcare REIT that was established in 2003 to develop and acquire net-leased hospital properties.

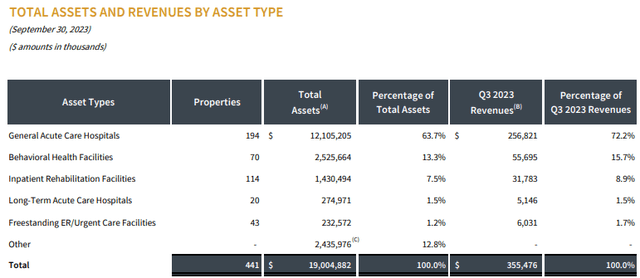

Since that time, MPW has grown to become one of the largest owners of hospital real estate with a portfolio that includes 337 properties containing approximately 43,000 licensed beds which are leased to or mortgaged by 54 operators across 9 countries including the United States, the United Kingdom, Switzerland, Germany, Italy, Spain, Portugal, Colombia, and Finland.

General Acute Care Hospitals are MPW’s largest property type and make up 63.7% of their total assets, and contributed 72.2% of their third-quarter revenue.

Their next largest property type is Behavioral Health Facilities which makes up 13.3% of their total assets and 15.7% of their 3Q revenue, followed by Inpatient Rehabilitation Facilities which makes up 7.5% of their total assets and 8.9% of their 3Q revenue.

MPW also invests in Long-Term Care Hospitals and Urgent Care Facilities which combined make up approximately 2.7% of their total assets and 3.2% of their 3Q revenue.

MPW – IR

In October MPW released its third-quarter earnings results and reported total revenue of $306.6 million during 3Q-23, compared with $352.3 million for the same period in 2022.

Normalized FFO (“NFFO”) came in at $225.5 million, or $0.38 per share, compared to $272.3 million, or $0.45 per share in the third quarter of 2022.

AFFO generated during the quarter was reported at $182.1 million, or $0.30 per share, compared to $215.4 million, or $0.36 per share for the comparable period in 2022.

While I never like to see year-over-year earnings numbers go down, in MPW’s case it is understandable as they have been strategically divesting assets to reduce debt which has impacted their rental revenues, NFFO and AFFO.

Some recent examples include MPW’s sale of 3 hospitals to Prime Healthcare for roughly $100 million and the hospital REIT’s sale of its 4 remaining properties in Australia for approximately AUD $470 million.

In order to improve their balance sheet and liquidity MPW also recently cut their quarterly dividend from $0.29 to $0.15 per share.

On the third quarter results MPW’s CEO Ed Aldag, Jr stated:

“Our business model remains strong and stable. Looking forward, we have launched a capital allocation strategy to increase liquidity, effectively address our debt maturities and solidify through a right-sized cash dividend our business for sustained long-term shareholder creation and growth when our cost of capital inevitably begins to normalize.”

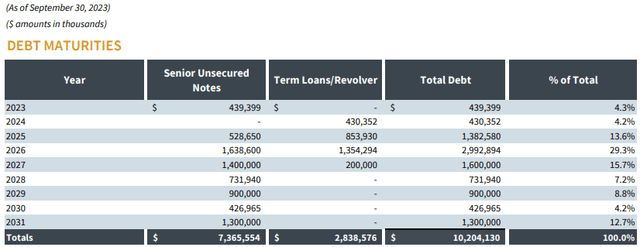

At the end of the third quarter, MPW reported an adjusted net debt to adjusted EBITDAre ratio of 6.7x, a total debt to total gross assets ratio of 50.2%, and an interest coverage ratio of 3.1x.

The majority of their debt is fixed rate at 85% and carries a weighted average interest rate of 4.041%. Additionally, only 4.3% of their debt matures in 2023 and only 4.2% of their debt matures in 2024.

During the earnings release, MPW disclosed that it was continuing to evaluate options to increase its liquidity, including joint ventures and further asset divestiture. In total MPW’s stated goal is to raise $2.0 billion in new liquidity over the next year.

MPW – IR

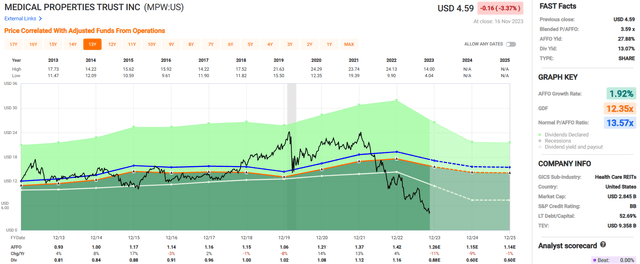

MPW shareholders have had a rough ride recently with the stock falling by 62% over the last year. The sell-off has pushed the stock’s price down to multi-year lows which may present an opportunity for an investor with a high risk tolerance.

While some macro issues have impacted all REITs (interest rate/inflation) some of the sell-off is due to issues specific to MPW such as their tenant concentration and tenant health.

If MPW can “right-the-ship” by strengthening its balance sheet and returns to growth it may be a very compelling investment opportunity at today’s price.

Currently, the stock is trading at a P/AFFO of just 3.59x, compared to their 10-year average AFFO multiple of 13.57x, and pays a 13.07% dividend yield that is well covered with a third-quarter AFFO payout ratio of approximately 50%.

We rate Medical Properties Trust a Spec Buy.

FAST Graphs

Seritage Growth (SRG) – Short Interest: 25%

Seritage Growth Properties was formed in 2015 as a REIT for the purpose of unlocking the real estate value of the retail portfolio it acquired from Sears in 2015.

SRG continued operating as a REIT through the end of 2021, but on March 31, 2022, the company revoked its REIT status to become a taxable C-Corp effective on January 1, 2022.

The change gives SRG more operational flexibility to sell its assets and pay down its debt, as it is no longer subject to operating under the regulations governing REITs.

Initially, Seritage Growth was primarily engaged in the development and ownership of a portfolio of diversified and mixed-use properties that were leased to retail tenants, but in October of 2022, SRG shareholders approved the proposed “Plan of Sale” which enables SRG’s Board to sell all of the company’s assets, distribute the profits to the shareholders, and dissolve the company.

Under the “Plan of Sale,” SRG will continue to manage each remaining property until it is sold.

As of the end of the third quarter, SRG’s portfolio consisted of interests in 42 properties totaling roughly 5.6 million square feet of gross leasable area (“GLA”), close to 126 acres held for development until the time of sale, and approximately 259 acres to be sold in its current condition.

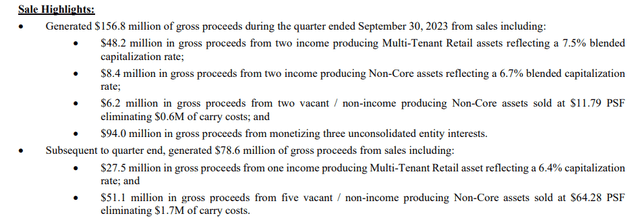

In November SRG released its third quarter operating results and reported $156.8 million of gross proceeds during the quarter, and $78.6 million of gross proceeds subsequent to quarter end from the sale of multiple retail properties.

SRG – IR

SRG has 8 assets under contract which are subject to closing conditions but are expected to generate gross proceeds of approximately $78.0 million upon sale.

Additionally, the company is currently negotiating purchase and sale agreements (“PSAs”) on 7 assets for expected gross proceeds of approximately $59.0 million.

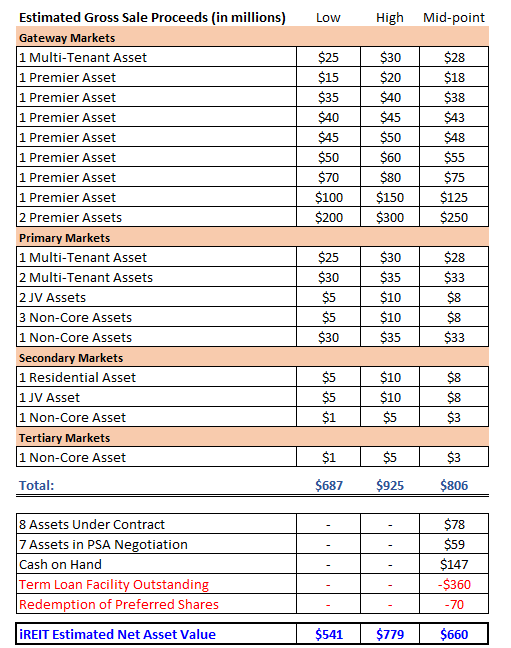

Below is a list of future sales projections listed in their earnings release which provides SRG’s current estimated gross sale proceeds per asset in their portfolio. The list of future sales projections does not include the 8 assets under contract or the 7 assets in PSA negotiations.

SRG – IR

Below, I combined the list of future sales projections with the expected gross proceeds for the assets under contract and in PSA negotiations, added cash on hand, and subtracted total debt and preferred equity to arrive at an estimated net asset value (“NAV”) of $541.0 million at the low end, $779.0 million at the high end, and $660.0 million at the mid-point.

SRG – IR (compiled by iREIT)

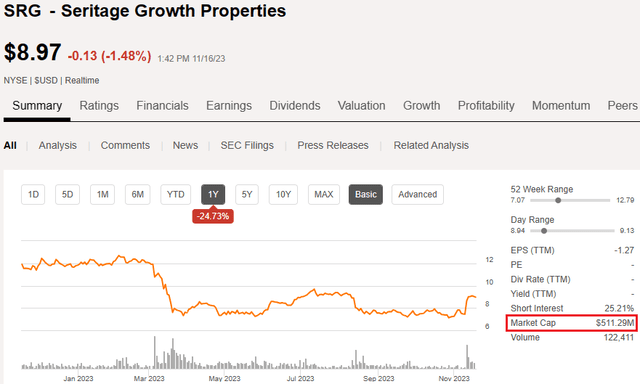

Currently, SRG is trading at $8.97 per share for a total market cap of $511.29 million. Using the low end of our NAV estimate SRG is trading at a P/NAV of 94.45%, using the high end of our NAV estimate it is trading at a P/NAV of 65.60%, and using the mid-point gives us a P/NAV of 77.42%.

Using these estimates, implies a potential upside ranging from approximately 5.50% at the low end of our NAV estimate to 34.40% potential upside at the high end of our NAV estimate.

Now, no investment is without risk and there is no guarantee that SRG will receive the gross sale proceeds it expects. Property values can fall or other economic conditions may negatively impact the value of their properties which would reduce the NAV and potential upside.

We have no rating on Seritage Growth Properties.

Seeking Alpha

Pebblebrook Hotel (PEB) – Short Interest: 17%

Pebblebrook Hotel Trust is a REIT that was formed in 2009 to invest in upscale, full-service hotel properties located in large U.S. cities and to invest in resort properties located in select destinations, with a primary focus on major gateway coastal markets.

PEB invests in both branded and independent hotels with a focus on the “upper-upscale” segment of the lodging sector. Some of the major brands their hotels operate under include Hilton, Westin, and Hyatt.

Pebblebrook looks for full-service hotels that normally have at least one or more restaurants, lounges, and meeting centers and targets markets with high barriers to entry, including select leisure destinations and major gateway markets.

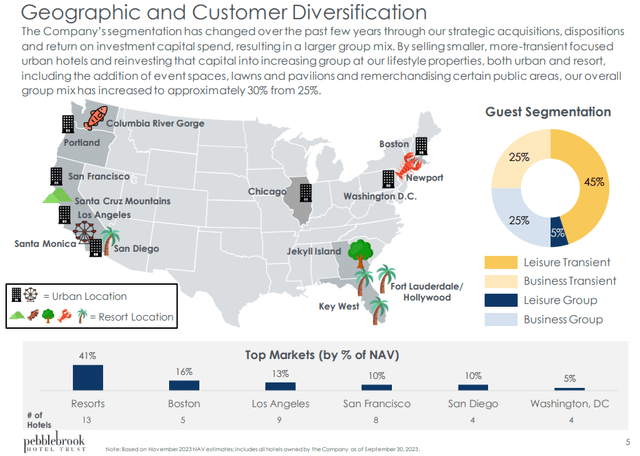

As of their most recent update, PEB owns 47 hotels and resorts across 13 urban and resort markets that contain approximately 12,200 guest rooms.

Their top 3 markets include resort markets which contain 13 properties and represent 41% of their portfolio NAV, Boston which contains 5 properties and represents 16% of their NAV, and Los Angeles which contains 9 properties and makes up 13% of their portfolio NAV.

45% of their guest segmentation is made up of leisure transient, followed by business transient and business group which each represents 25% of their guests.

Leisure group is their smallest category and only represents 5% of their guest segmentation.

PEB – IR

Pebblebrook Hotel released its third-quarter operating results in October and reported total revenues during the quarter of $395.8 million, compared to total revenues of $416.7 million for the same period in 2022.

FFO available to common shareholders during the quarter was reported at $66.0 million, or $0.54 per share, compared to FFO available to common shareholders of $80.8 million, or $0.61 per share in the third quarter of 2022.

AFFO during the quarter came in at $74.1 million, or $0.61 per share, compared to AFFO of $86.7 million, or $0.66 per share for the comparable period in 2022.

On the earnings results, Pebblebrook’s CEO Jon E. Bortz stated:

“Our third quarter bottom line results were at the top end of our expectations, even after the negative impact of severe weather events on both coasts and the labor strikes in the entertainment industry that primarily affected our Los Angeles properties.

We continued to see healthy occupancy improvements in our urban market hotels, driven by improving group and transient business travel, as well as solid gains in weekend leisure demand. Our third quarter resort portfolio occupancy was flat year-over-year, though it would have been higher if not for the severe weather events.”

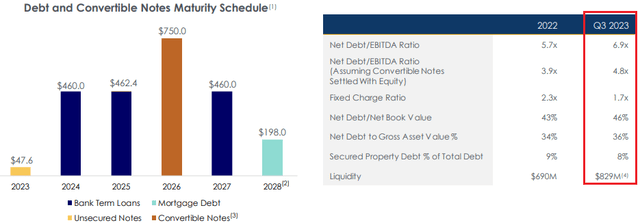

PEB also provided an update on their balance sheet and liquidity and reported total liquidity of approximately $829.0 million, which consisted of $191.6 million in cash, equivalents, and restricted cash, and $637.4 million available to them under their unsecured revolving credit facility.

PEB’s consolidated debt and convertible notes have a weighted average interest rate of 4.4% with a weighted average term to maturity of 2.8 years and 78% of their debt is set to a fixed rate.

For 3Q-23, PEB reported a net debt to EBITDA ratio of 6.9x, a net debt to gross asset value ratio of 36%, and a fixed charge coverage ratio of 1.7x. Additionally, the company has no significant maturities until the fourth quarter of 2024.

PEB – IR

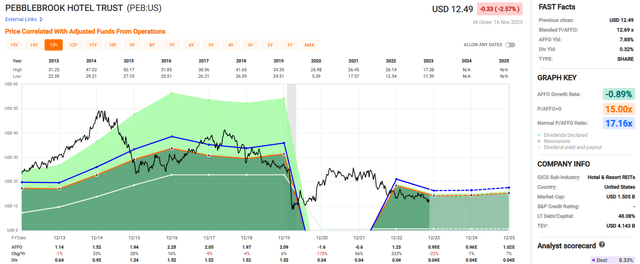

Over the past 10 years, Pebblebrook has had an AFFO growth rate of -0.89%. As clearly illustrated in the chart below, PEB’s AFFO was severely impacted by the pandemic in 2020 which has distorted their average AFFO growth rate.

When removing 2020 from the calculation PEB delivered an AFFO growth rate of 8.91% from 2013 to 2019. Similarly, due to the pandemic, PEB had to slash its dividend by 97.37% in 2020, going from a dividend of $1.52 per share in 2019 to just $0.04 per share in 2020.

Since the severe cut in 2020, PEB has maintained its quarterly dividend at $0.01 per share and currently has a dividend yield of 0.32%. PEB’s stock is trading at a P/AFFO of 12.69x, which is discounted when compared to their 10-year average AFFO multiple of 17.16x.

We rate Pebblebrook Hotel Trust a Spec Buy.

FAST Graphs

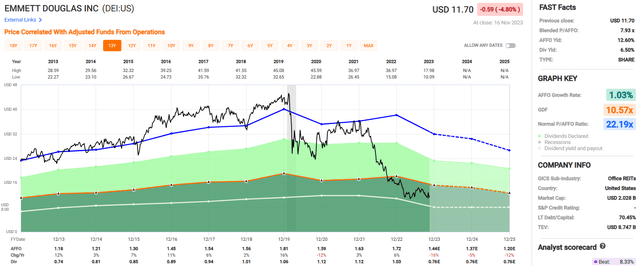

Douglas Emmett (DEI) – Short Interest: 16%

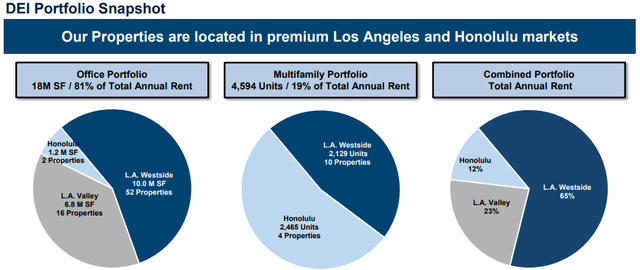

Douglas Emmett is a diversified REIT that invests in high-quality office properties and multifamily communities located in top coastal submarkets within Los Angeles and Honolulu.

DEI specializes in the development, acquisition, and management of Class A office properties and premier multifamily communities and targets markets with material supply constraints and high-end housing.

DEI has properties located in some of the most prestigious submarkets of Los Angeles and Hawaii including Beverly Hills, Brentwood, Santa Monica, and Honolulu.

Douglas Emmett’s portfolio consists of 70 office properties totaling 18.0 million square feet and 14 multifamily properties that contain 4,594 units.

The majority of their annual rent comes from office properties at 81.0%, while multifamily properties make up approximately 19.0% of their annual rent.

By location, L.A. Westside makes up 65.0% of its annual rent, L.A. Valley makes up 23.0%, and Honolulu makes up 12% of its annual rent. As of the end of the third quarter, DEI’s office properties had an occupancy rate of 81.8%, and its multifamily properties have a lease rate of 98.9%.

DEI – IR

In October Douglas Emmett released its third-quarter operating results and reported total revenues during the quarter of $255.4 million, compared to total revenues of $253.7 million for the same period in 2022.

FFO during the third quarter was reported at $89.4 million, or $0.45 per share, compared to FFO of $105.2 million, or $0.51 per share in the third quarter of 2022.

AFFO was reported at $68.7 million, or $0.34 per share, compared to $90.4 million, or $0.44 per share for the comparable period in 2022. The year-over-year decrease in FFO was primarily attributed to higher interest expense on their floating rate debt.

During the quarter Douglas Emmett signed 225 office leases totaling roughly 934,000 square feet which included 267,000 square feet of new leases. Rental rates on leases signed during the third quarter increased by 3.6% on a straight-line basis and decreased by 9.7% on a cash basis when compared to the expiring leases for the same space.

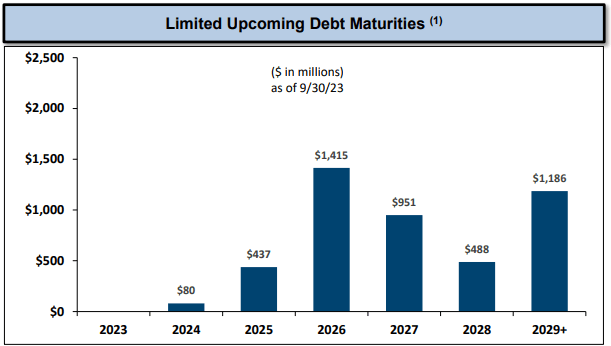

At the end of the third quarter, DEI had cash and equivalents totaling $526.2 million, no corporate-level debt, and nearly 50% of its office properties were unencumbered. Plus, DEI’s next term loan maturity is not until December 2024.

DEI – IR

Over the last decade, DEI has had a blended average AFFO growth rate of 1.03% and an average dividend growth rate of 5.22%. The company increased its dividend each year between 2013 to 2020 but did not raise its dividend in 2021.

In the fourth quarter of 2022, the quarterly dividend was cut from $0.28 to $0.19 per share, representing a 32% dividend cut. In its 4Q-22 press release DEI stated that the reduced dividend rate would provide the REIT with over $74.0 million per year in extra liquidity.

Analysts expect AFFO per share to fall by -16% in 2023, and then fall by -5% and -12% in the years 2024 and 2025, but analysts expect the dividend to be maintained at $0.76 per share annually.

Currently, the stock pays a 6.50% dividend yield that is well-covered with a 2022 year-end AFFO payout ratio of 59.88% and trades at a P/AFFO of 7.93x, which is a significant discount when compared to their 10-year average AFFO multiple of 22.19x.

We have no rating as Douglas Emmett is not currently in our coverage spectrum.

FAST Graphs

In Closing

As I explain in my new book,

“Advocates of short selling believe it’s beneficial to investors. They say it helps identify overvalued shares and then narrows the price inflation by selling them.

And since there are times when that turns out to be true, I wouldn’t ignore short-seller analysis altogether.

It can end up being an important part of research, bringing serious issues to light such as operating deficiencies and financial fraud.”

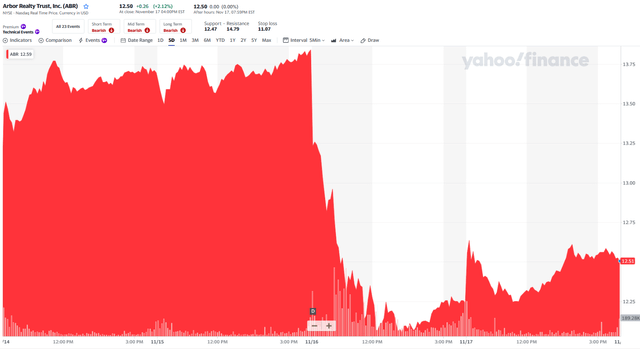

A few days ago, Arbor Realty (ABR) shares fell by over 12% after Viceroy research published a report titled Slumlord Millionaires that explained,

“Viceroy’s dive into Arbor’s CLOs suggests its entire loan book is distressed and underlying collateral is vastly overstated. These loans do not qualify for refinancing anywhere, and substantially all mature within the next 18 months.”

Yahoo Finance

Also, remember that Viceroy is also a DEFENDANT in a lawsuit with Medical Properties and according to Bloomberg, the hospital REIT.

“…won a second preliminary court ruling in its defamation lawsuit over an alleged “short and distort” scheme by Viceroy Research.”

Judge R. David Proctor is allowing the case to

“…move forward against two of Viceroy’s principals about two months after ordering the firm and another executive to face the allegations. The suit, filed in March, says they ran a smear campaign involving social media posts and more than a dozen reports.”

There’s no question that social media has made it more convenient for short sellers to disseminate so-called research, which is why it’s important to always do your own due diligence by paying close attention to fundamentals.

As always, thank you for reading and I look forward to your comments below.

Note: Brad Thomas is a Wall Street writer, which means he’s not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: Written and distributed only to assist in research while providing a forum for second-level thinking.

Read the full article here