")

Wynn Palace in Cotai shows iconic Y design of all WYnn properties.

Premise: Tracking the shares of Wynn Resorts (NASDAQ:WYNN) for over 44 years has covered my career, as a publisher of the first ever gaming business publication, to my c-suite career as a gaming executive, and subsequently as a consultant and financial analyst. It has also afforded me over time many one on one industry discussions with its eponymous founder Steve Wynn.

And during a six -month period around 2000 I was a holder of Wynn shares, averaged about $14 to $17. Needless to say, I exited my position with a return that paid in full the four-year tuitions for two of my three sons. Thank you Steve. I hold no shares in the company since nor any other gaming stock as I have frequently noted on my Seeking Alpha posts avoiding conflict of interest situations with my casino clients. My gaming portfolio is in a blind trust.

During my various career tenures, I have been a constant student of the stock for any number of reasons. Among them is my curiosity from the early 80s as to why, despite at times when peers generated superior earnings, or showed better sales growth, the Wynn shares always traded far above rivals.

google

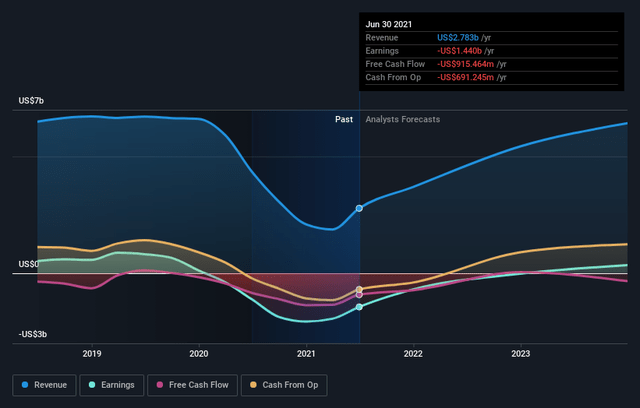

Above: Outlook remains strong.

Of course there was a certain, almost mythical, reverence rife among the analyst community in the presence of Steve Wynn personally as CEO.

Wynn’s unique reputation as the presiding genius of the industry was well deserved. It wasn’t only because of the big moves he made between Atlantic City and Las Vegas, but the dozens of normally under the radar business decisions that added to the allure of the stock competitors couldn’t touch.

He was first to solve the most difficult dilemma of the AC slot business, i.e., how to identify the hoards of slot players who descended upon the town by bus every day. The industry was giving away millions in rolled quarters on the come, but other than a primitive process where hosts stood behind players at the machines scribbling estimates of coin in. provable.

Wynn hit on an idea to adapt the old Maryland seaside boardwalk marketing ploy. They were called ticket spitters. They were devices attached to boardwalk arcade games that cranked out tickets from a roll synced with a player’s toss on each ball play. At the end of the play, the customer bellied up to the prize counter, got a total from the clerk.

What Wynn then did was set the devices so that a player was identified by a card insert in the slot machine then the ticket redemption began. Players came to the prize counter but there wasn’t only teddy bears or coffee pots to choose from. Players could redeem for e buffet ,restaurants, shows, t-shirts, rooms spa days.

More important Wynn now had a way to identify his slot customers. Then it was a sheep and goats process to refine the play by player value.

The rest was easy. Those players who generated the most tickets would receive the best valuable comp offers. So Wynn now had the day, the shift, the machine the denomination of the coin in, the losses and the wins.

In time, the Golden Nugget led the city in daily win per machine, by the percentage of dollar slot play vs. quarters and the opportunity for his host contingent to size into players as they poured in their coins. This and other marketing tools developed by Wynn and his staff build the data base of players with above average wins per trip.

This meant more affluent average customers, who in the basic casino business mantra that birds of a feather flock together, created an ambiance on the property that it was a high end, high status casino. It’s what attracted the super high end play from Philadelphia and New York that supported the top grossing table game wins as well.

That among other reasons is how Wynn both in Vegas and AC built the singular most valuable customer database in the business. And that data, at the end of the customer machine, translated to a powerful, sustained earnings leadership. He once told me the single most valuable marketing tool for a casino was the property itself. You don’t build to be competitive, you build properties to dazzle and wow customers – “it’s all about a departure from reality” he said. As he and his team began to design to be the top place in town.

All this set the Wynn shares on a decade long drive to valuations that ran from 25% to 39% higher. The proof was found in an amazing statistics: Wynn properties were out winning its most aggressive peers in average daily win in average customer value. They won more money with fewer machines and tables than everyone else in town.

Google

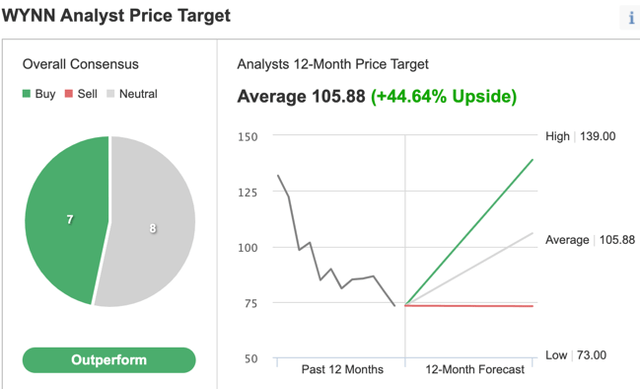

Above: Analyst PT shows 44% updated price.

It began to appear to be driving higher valuations

Wynn had but one sequence of bad performance. It was around 2000. For the first time Wall street battered Wynn shares when analysts got out the pitchforks over what the street saw as Wynn’s, excessive investment in masterpieces of French Impressionist art in the 100s of millions. Add to that an immediate sense that the master had lost his touch and an assault on the Mirage stock from Kirk Kerkorian and you had a major swoon. I came into the stock then precisely because of my feeling that there would always be a good bet on the stock because the core operational formula worked regardless of intermittent headwinds.

Recent comparative price history in sector: Wynn vs. peers

Nov. 2021: Our post that Wynn looked attractive at $86.

Peers in same date window: (We called a PT at$120)

MGM: $40.26

LVS: $48.28

CZR: $45.55

BYD: $38.47

PENN: $25.27

On January 17th of this year, we posted a buy call at $97.

Most peers continued dead pooled around Nov. prices.

Price at writing: $107.36. The stock is up ~20% since our November call. With similar headwinds and tailwinds impacting the sector, we note here that Wynn commanded a double valuation against peers.

Our data archives suggested this was par for the course in general over the last 40 years. Since 2018 of course, Steve Wynn was no longer a factor in valuation. So it is clear that what he built both in Vegas, Macau and Boston still reflected his imprimatur. It is a deep down formula as noted of dead aim on an upscale customer both high end and tourists over decades. Innovative marketing programs, strong customer contact culture sustained.

Our conclusion

While the entire gaming sector was buffeted by the same covid headwinds, as soon as the worst part of the crisis began to fade, Wynn resumed its price leadership in a market that continues to believe it owns a perennial premium vs. peers.

If this is a long term, reliable measure of Mr. Market’s judgment that no matter the circumstances, Wynn shares have a built in premium that departs from the overall tone of the sector market in rise or decline.

For that reason, we believe that a premium mentality has ruled the trading of Wynn shares over decades and that in a sense is an unappreciated alpha. Investors ever on the trail of unrecognized alphas in items like undervalued balance sheet assets like dormant reality, or data base growth out pacing competitors over time, superior sales growth against peers in same markets bypass this not so apparent value.

It means that no matter the macro trends in the sector, Wynn shares will always trade at a premium.

Pre-covid, on January 7th of 2020, Wynn shares traded at $141.80, again a substantial premium over peers.

The company trades at an EBITDA margin of 30% for this year, and the same forecast for 2025.

We estimate a forward P/E based not only on recent trends in the sector, but with a data set on its relative trading to peers since 2005.

Total revenue 2023: $6.5b vs. $3.7b for 2022 clearly the result of Macau recovery and strong Vegas outlook.

We are looking at a FWD EPS of $526 to $5.34 for 2024.

A FWD P/E in a range of 20 to 22 which given our estimates of FWD sales growth in Vegas, Macau and Boston males Wynn a strong buy going deep into this year. I also believe it’s too little too late entry into sports betting will end in a sale of the unit. It was clearly bad timing, but Wynn historically does know when to hold ’em and when to fold ’em.

We are raising our PT to $140 by the end of Q3’23. One of the underlying forward strengths will be the growth of Wynn Macau market share into the central teens this year.

Read the full article here